(Idea) Occidental Petroleum - Recent Deleveraging Strengthens The Investment Case

Occidental 2024 write-up (public)

Occidental 2025 write-up (public)

By: Jon Costello

The market continues to value Occidental Petroleum (OXY) as a heavily indebted company. That description is becoming obsolete faster than investors appear to recognize.

When I last revisited OXY in June 2025, I expected balance-sheet repair to remain the dominant issue through 2027, with larger repurchases and dividend increases beginning in 2028. I was too conservative. OXY ended the first quarter of 2026 with $13.3 billion of long-term debt, down from a post-CrownRock peak of $28.9 billion and only $3.3 billion above management’s near-term target of $10 billion. At sustained oil prices above the mid-$70s per barrel, the company should reach that target within months.

That timing matters because the oil market is pricing an orderly reopening of the Strait of Hormuz and a quick disappearance of the recent risk premium. That assumption strikes us as too complacent. OXY is one of the cheapest large-cap ways to express the opposite view, but the investment thesis no longer depends only on higher oil prices. It also rests on a balance sheet that has already improved substantially.

The Balance Sheet Changed Faster Than I Expected

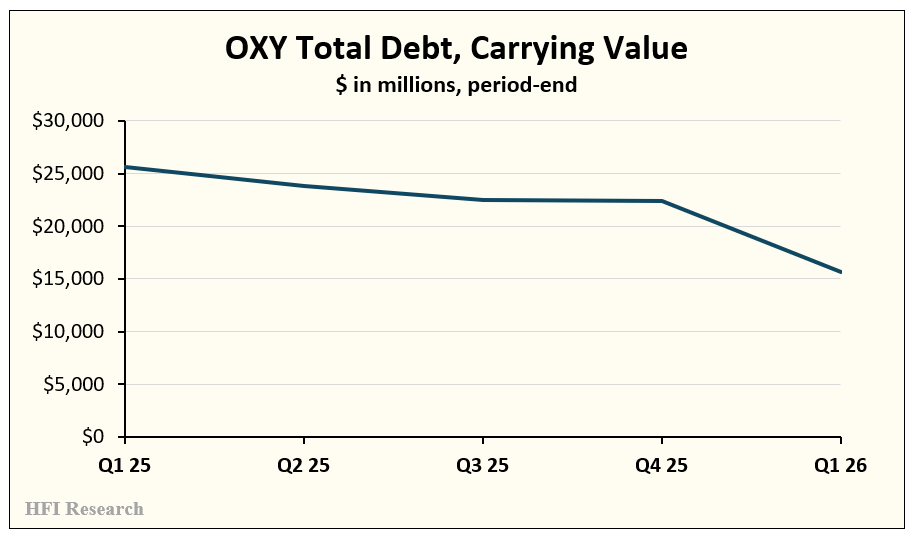

The OxyChem sale closed on January 2, and management applied the proceeds to debt. Since December alone, OXY has reduced long-term debt by $7.5 billion. Total debt has fallen to $15.7 billion at the end of the first quarter from $25.6 billion a year ago.

The improvement extends beyond the headline debt reduction. OXY’s annual interest run-rate is approximately $845 million, roughly $550 million below the 2025 level. Near-term maturities are also modest, with only $415 million due through the end of 2029. The company no longer needs favorable capital markets to complete the remaining deleveraging.

The following chart shows OXY’s total debt at carrying value over the past five quarters.

OXY’s long-term debt position now supports, rather than constrains, the investment case for owning OXY shares.

At the oil prices used in my valuation, OXY should reach $10 billion of long-term debt in approximately three to five months. The relevant question is therefore no longer whether the balance sheet will be repaired, but how management will allocate cash once that target is reached.