(Idea) Occidental Petroleum

By: Jon Costello

Occidental Petroleum (OXY) shares have underperformed their large-cap peers over recent months. Despite the underperformance, OXY’s fundamental results have been strong, and its near-term and longer-term outlook for shareholders remains positive. Investors may want to consider buying the shares either as a catch-up trade based on a summertime oil price rally or as a long-term investment that will benefit from growth in shareholder value over the coming years.

OXY Has Lagged Its Peers

It wasn’t long ago when OXY shares exhibited relative strength as Berkshire Hathaway (BRK.B) amassed its 27% equity stake. Those days are long gone. OXY shares have sold off year to date and are now approximately 20% below Berkshire’s average cost for its stake in the mid-$50s per share.

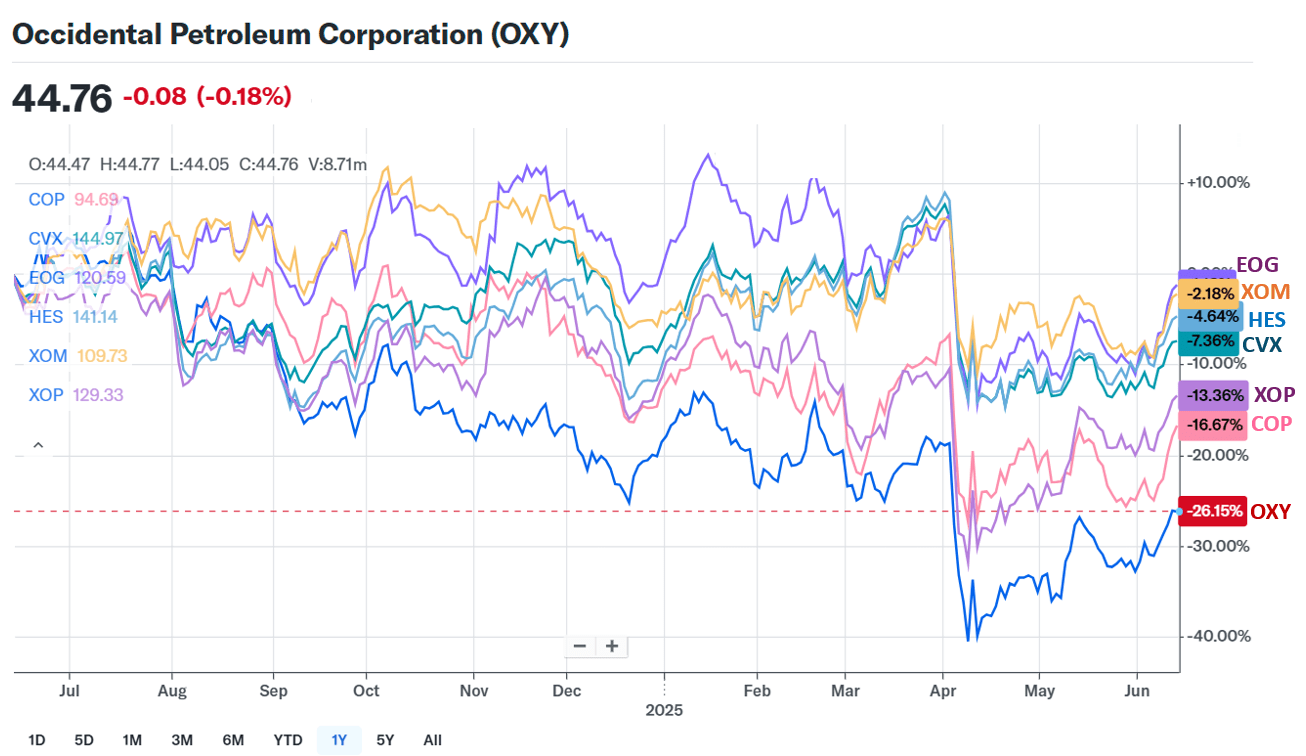

For multiple consecutive quarters, OXY shares have badly lagged behind their peers—both independent U.S. shale E&Ps and international oil & gas majors. The following chart plots the performance of OXY’s stock versus its large-cap U.S. peers over the past year.

Source: Yahoo! Finance, June 12, 2025.

While OXY shares may have received too much support from Berkshire’s backing, the recent underperformance is overdone. Even the company’s critics, who take issue with the caliber of its management, the purchase price of large shale acquisitions, or the ultimate value of its foray into carbon capture, have to acknowledge that nothing is fundamentally wrong with the company.

The most valid criticism of OXY is that its leverage is high—at approximately two-times operating cash flow at $70 per barrel WTI—but leverage must be considered relative to free cash flow generation, and OXY becomes a free cash flow machine as oil prices rise above $70 per barrel. OXY’s balance sheet shows no signs of strain. It will easily meet its debt maturities as they come due. As it pays down debt, grows its non-oil and natural gas-related operations, and benefits from higher commodity prices, value will accrue to shareholders from their increased claim on the company’s equity and higher free cash flow per share.

I expect management’s continued execution to drive future outperformance in OXY shares. The shares appear attractive as either a relatively short-term catch-up trade amid a summer oil price rally or over a multi-year holding period as OXY pays down debt and executes other accretive capital allocation measures for shareholders.