(Idea) Transocean

Big Upside As The Cycle Turns.

By: Jon Costello

I’ve expressed my interest in offshore drillers in several recent articles, including today’s macro update. These companies have made it through what was arguably their industry’s worst-ever downturn and are now poised to profit in the upcycle.

My top pick in the sector has been Valaris (VAL), but others like Noble Energy (NE) and Transocean (RIG) also deserve a look. This article discusses Transocean’s risks and upside potential.

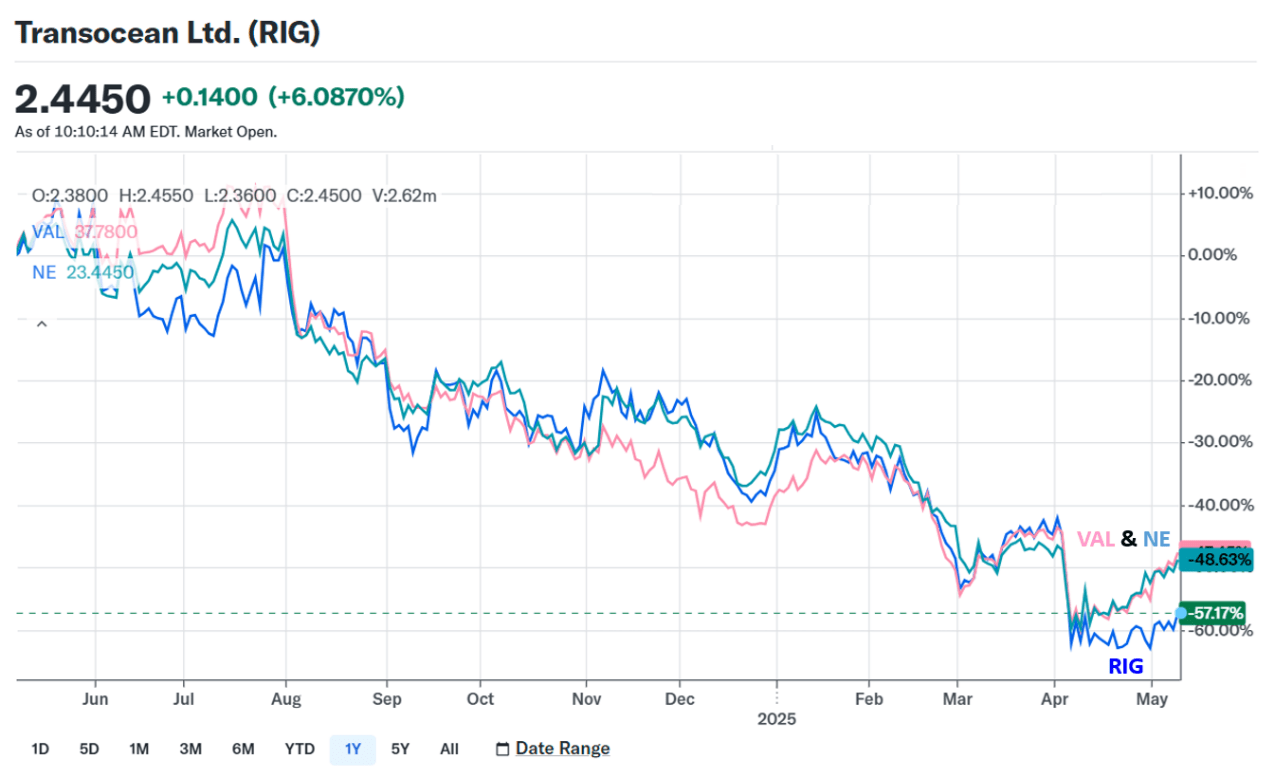

Recent Share Price Underperformance

Transocean is one of the few global offshore drilling service contractors that has avoided bankruptcy in the offshore drilling downturn that began in 2014. Its defining characteristic vis-à-vis its peers is its high-quality assets and large contract backlog. Its negative is its heavy debt load. Its peers discharged most of their long-term debt in bankruptcy. In the process, the pre-bankruptcy equity was all but wiped out, and most debt was converted to equity. They emerged with conservative financial profiles and slimmed-down balance sheets.

Transocean’s debt load and the risk that it enters bankruptcy if the offshore drilling cycle remains depressed have caused its shares to dramatically outperform its large peers since they exited bankruptcy in the 2021-2022 timeframe.

The company’s higher risk is responsible for its underperformance in the most recent downturn for offshore drilling stocks. Whereas its peers have bounced hard over recent weeks, Transocean’s shares have lagged, as shown below.

Source: Yahoo! Finance, May 8, 2025. Tickers added by author.

Risks remain for Transocean’s shareholders, which could cause its stock to continue to lag those of its peers. First and foremost among them is its large legacy debt load. Investors in Transocean’s stock must be confident that the company can meet its debt obligations and survive the current oil market downturn in a form that allows its shares to participate in the subsequent upturn.

Drillship and Semisubmersible Backdrop

The global rig fleet currently includes 109 drillships and 92 semisubmersibles, inclusive of “stacked” rigs, which are the rigs that have been temporarily idled. There are 14 drillships and 13 semisubmersibles that have been “cold stacked,” or maintained at minimal expense.

In 2023, investors began to anticipate an offshore cyclical recovery, as demand for floaters and semisubmersible rigs grew to a point at which contract rates began to increase and stacked rigs were reactivated. However, activity began to slow in late 2024 after major oil companies postponed projects.

While the upcycle has been paused since then, all signs indicate the longer-term recovery is still underway. Contract rates, which hovered in the range of $200,000 per day, increased into the high $400,000s and low $500,000s in 2024. They have since declined to the mid-to-low $400,000 range today. At the current level, the major offshore drillers are operating close to cash flow neutrality.

The next few years will likely see continued attrition of the existing floater and semisubmersible fleets, while new offshore project upstarts will add to the demand for existing offshore rigs. Amid this backdrop, the offshore drilling service companies will see their cash flow inflect higher, as rates increase and stacked rigs are reactivated.