(Idea) Buy Valaris

By: Jon Costello

Valaris Ltd. (VAL) is a Bermuda-domiciled offshore contract drilling company. I’ve followed the name for the past few years but never invested due to the industry's vulnerability to fickle day rates and its brutal cyclical downturns.

However, my interest was recently piqued when VAL shares fell into the low $30s. I began buying after realizing that macro trends within the industry favor a continuation of its upcycle and that a cash flow inflection could generate multi-bagger returns from current prices.

Based on conservative assumptions over the next few years, I believe VAL shares remain extremely undervalued. They’re one of my favorite ways to play higher oil prices and navigate range-bound or potentially sideways oil price action over the next 18 to 24 months.

Valaris Emerges from Bankruptcy

VAL is the successor to Ensco Rowan, which was formed through Ensco’s acquisition of Atwood Oceanics in 2017 for $839 million and then its acquisition of Rowan in 2018 for $2.4 billion. Ensco Rowan entered bankruptcy in August 2020.

At the time of the bankruptcy, the company listed $12.9 billion of assets and $7.3 billion of long-term debt. In bankruptcy, it reduced long-term debt by $6.5 billion. Its existing credit facility and unsecured notes were converted to equity.

The company also secured a $520 million capital injection and $550 million of new 8.25% Senior Secured Notes that mature on April 30, 2028. Interest on the Notes can be paid in kind at 12% for the life of the note. Old shareholders received warrants issued on 5.6 million new VAL shares. The warrants expire in April 2028 and have a $131.25 strike price.

Reorganization and fresh-start accounting adjustments made in the bankruptcy process—which occurred amid depressed asset values during the Covid downturn—reduced the company’s reported asset value by $9.1 billion. VAL emerged with an asset value of $2.6 billion. It exited bankruptcy in May 2021 through an IPO of 75 million shares that began trading at around $22 per share, giving it a $1.65 billion market cap.

Since the IPO, share repurchases have reduced VAL’s diluted share count to 72.9 million. With shares trading around $38, the company has a market cap of $2.8 billion. Its $700 million in net long-term debt results in an enterprise value of $3.5 billion.

The Bull Case: It’s All About the Cash Flow Inflection

The bull case for all offshore drillers rests on the cash flow inflection that occurs during an industry upcycle.

Over the course of an entire cycle, offshore drilling is a lousy business. During downturns, lower oil prices reduce capex budgets among the oil majors and national oil companies that serve as the drillers’ primary customers. Lower capex, in turn, reduces the demand for offshore drilling rigs. As demand for rigs falls, the day rates by which rig prices are set decline. Since rig contracts run anywhere from a few months to multiple years, sustained low day rates reduce the earning power of a given rig fleet over time. Margins come under pressure, and offshore drillers operate at a loss for years at a stretch.

Adding to the industry’s woes during a downturn, uncontracted rigs must be maintained. These rigs are either “warm stacked,” or kept ready for redeployment, or “cold stacked,” in which they’re essentially mothballed at minimal expense. Warm stacking and cold stacking are costly. For instance, when VAL exited bankruptcy, its 18 cold-stacked rigs cost the company $60 million a year—just to maintain assets that generate no revenue. When market conditions improve, reactivation costs for cold-stacked drillships can run into the tens of millions of dollars.

These cyclical downturns have been a recurring feature of the modern offshore industry since it embraced capital-intensive deepwater drilling in the 1980s. The combination of declining day rates on a company’s existing fleet plus the increasing expenses associated with warm stacking and cold stacking idle rigs risks sends cash flow plunging. The deep cash flow losses bring about a large-scale industry purging that forces many operators into bankruptcy.

The most recent downturn was particularly brutal. Among the major global offshore drillers, only Transocean (RIG) avoided bankruptcy.

The opportunity in VAL’s stock stems from the cash flow inflection that occurs as negative operating leverage experienced in a downturn transitions to positive operating leverage in an upturn. This transition turbocharges cash flow growth. Prices rise, and what used to be a drag on corporate cash flow becomes a contributor.

This cash flow inflection is yet to come for both VAL and the offshore drilling industry. At the moment, the trend of improving day rates appears to have been delayed for a few quarters, not longer.

Equally important for investors, the offshore drilling industry’s economics have undergone a structural improvement. During the last downturn from 2014 to 2020, time was the offshore drilling investor’s enemy. Going forward, however, time will increasingly become the investor’s friend.

Why Does This Bargain Exist?

Along with the rest of the offshore services sector, VAL shares have been hammered over the past year, falling more than 50% from their high of around $80 last August. The stock’s one-year chart illustrates its dismal performance.

The selloff in the second half of 2024 was attributable to a deteriorating outlook for offshore rig contracting activity in 2025. Large project deferrals pushed startup dates from 2025 into 2026 and 2027, reducing demand for rigs in 2025. At the same time, contract suspensions by national oil companies increased the supply of available rigs.

Furthermore, a lull in tendering and contracting activity limited day rate visibility, raising concerns that the bull cycle had run its course. A mere whiff of another downturn is enough to send offshore drilling investors running—understandably so, given how much shareholder value is destroyed in the industry's downturns.

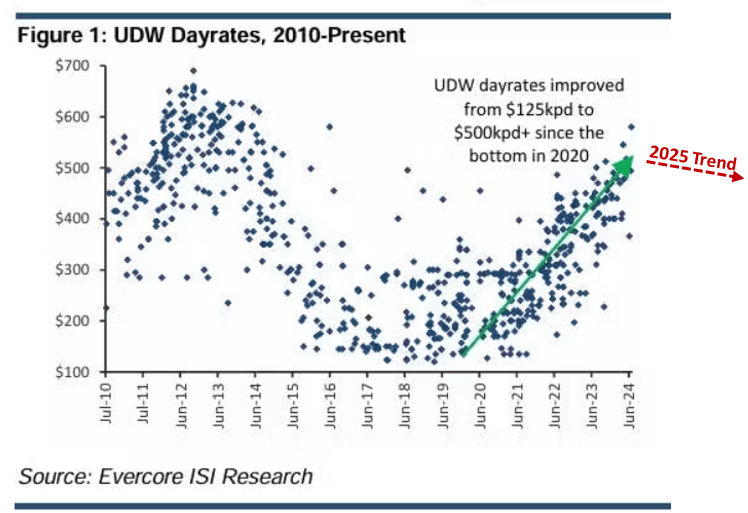

The slowdown spooked investors in offshore drilling stocks. Many had anticipated a continuation of the ongoing trend of increasing day rates. Dayrates for drillships had increased from roughly $200,000 when VAL exited bankruptcy in 2021 to a high of around $500,000 in mid-2024. The market dynamics during the second half of 2024 caused day rates for high-specification drillships to cool off to the mid-$400,000 level.

Source: Offshore, Evercore ISI, Aug. 7, 2024. Red text added by author.

Weakening day rates meant that the ongoing recontracting cycle, which the bulls were counting on to push an offshore fleet’s weighted-average dayrate higher over time, had effectively stalled.

Dayrates are now expected to remain flat in 2025. This outcome dealt a blow to the EBITDA and cash flow expectations among bullish offshore investors that prevailed in 2025 and drove share prices higher.

VAL’s Fundamentals Deteriorate

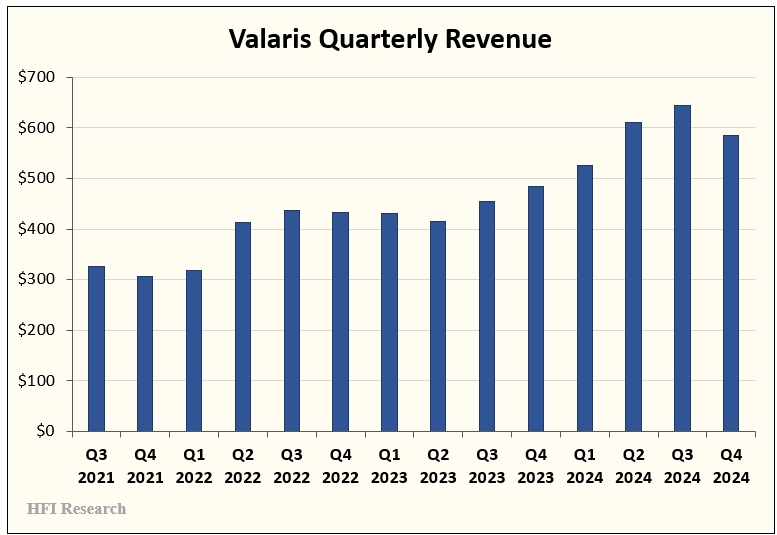

VAL’s financial results over the latter half of 2024 reflected the prevailing weakness in the industry. Fourth-quarter results, in particular, underwhelmed. Two drillships came off contract in the third quarter, increasing the number of uncontracted drillships to four out of VAL’s fleet of 15.

The increased count of uncontracted vessels reversed VAL’s multi-quarter trend of higher revenues, as shown below.

While Adjusted EBITDA was in line with analyst expectations and the company’s guidance, it declined to $142 million from $150 million in the third quarter. VAL’s contract backlog shrank to $3.6 billion on February 20, 2025, from $4.1 billion on October 30, 2024.

By early 2025, lower day rates and deteriorating company fundamentals ran headlong into President Trump’s “Drill Baby Drill” program, OPEC’s decision to add barrels to the oil market, and steadily falling oil prices. All these bearish factors sent VAL’s shares to multi-year lows.

Offshore Recovery is Set to Continue

Offshore drilling has been around since 1896, when it began in the Santa Barbara Channel in California. However, the modern industry took hold in the 1980s when oil majors sought new discoveries at greater water depths. Deepwater development efforts came as the major onshore fields matured. The largest of these fields were discovered in the 1960s and 1970s, and massive onshore discoveries like them were growing less frequent.

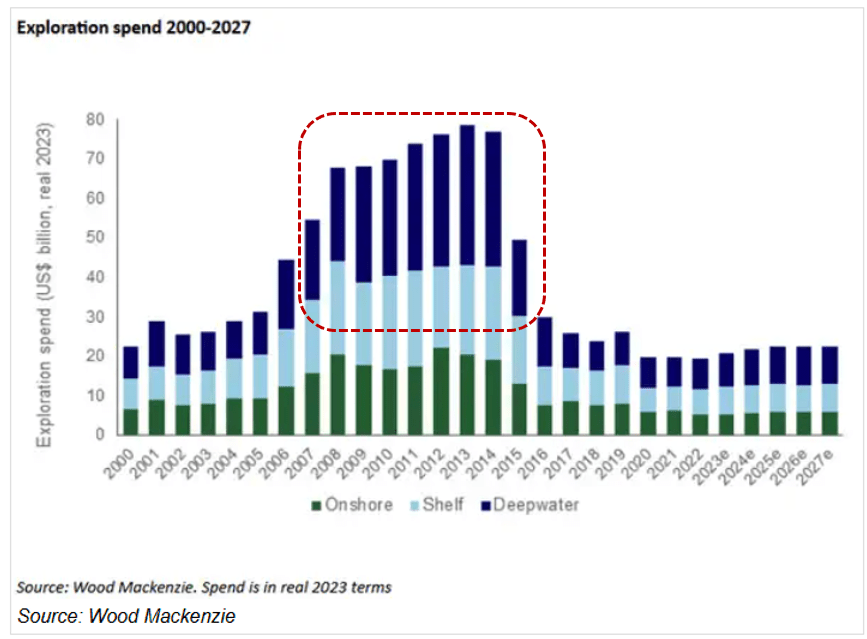

By the early 2000s, accelerating oil demand growth and constraints in onshore supply sent oil prices significantly higher. The cash flow windfall achieved by major oil companies drove a historic surge in offshore exploration capex, shown in the following chart.

Source: Wood Mackenzie, Offshore Engineering, Aug. 16, 2023. Red line added by author.

In 2009, the offshore spending boom dramatically boosted orders for newly built rigs. That year, the industry ordered 88 drillships and semisubmersible platforms, set to be delivered from 2009 through 2012. Only sixty-three of the newbuilds were contracted, with the remainder built with no guarantee of work.

Unfortunately for the industry, the increasing rig supply was heading toward a demand cliff. Just as the newbuilds arrived on the scene, marginal capex began to flock to the U.S. shale patch. When the wave of new rigs entered a market with lower-than-expected demand, the industry underwent a protracted downturn that lasted until 2021.

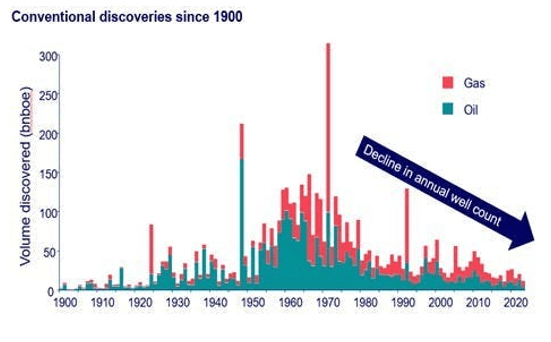

The torrent of capital investment flowing to U.S. shale resulted in capital being withdrawn from conventional exploration development. This accelerated the decline in conventional oil discoveries, which had already been underway for decades.

Source: Wood Mackenzie, Oil & Gas Journal, Nov. 21, 2024.

Today, the oil market is about to enter an entirely new phase. U.S. shale production growth is slowing markedly, a topic we’ve discussed ad nauseam.

Capex is a necessity in the oil and gas business, particularly among the oil majors and national oil companies. These large E&P operations form the customer base of the large offshore drillers. Their production portfolios run into the millions of barrels per day, and their production is constantly declining. They need new projects to maintain flat output and avoid angering their stakeholders. They will invest in new project development almost regardless of oil prices.

Consensus in the capital markets is warming to the reality that oil demand will continue to grow for at least the next decade. As a result, long-cycle conventional oil projects are gaining broad-based acceptance once again. As the renewables craze abates and oil exploration is viewed as necessary, companies are allocating capex away from renewables and toward oil and gas.

Large-scale E&P operations won't participate in U.S. shale. Current conditions offer scant opportunities for a non-U.S. major, such as BP (BP) or TotalEnergies (TTE). Most of the best acreage has either been consolidated or is depleting at a rapid clip.

Meanwhile, unconventional resources outside the U.S. lack the scale necessary to generate enough supply to meet increasing global demand.

Marginal capex will therefore have to fund conventional resource exploration development. This trend bodes well for offshore drilling activity and demand for offshore rigs over the coming years.

Offshore Upcycle to Continue in 2026

Among conventional supply alternatives competing for the marginal capex dollar, offshore will emerge as a prime contender. Offshore projects are planned over the course of an entire oil market cycle. As such, their development tends to be less dependent on near-term futures pricing, so they’re relatively immune to oil price volatility. This long-cycle feature of offshore resource development will support offshore drilling activity even if oil prices remain subdued.

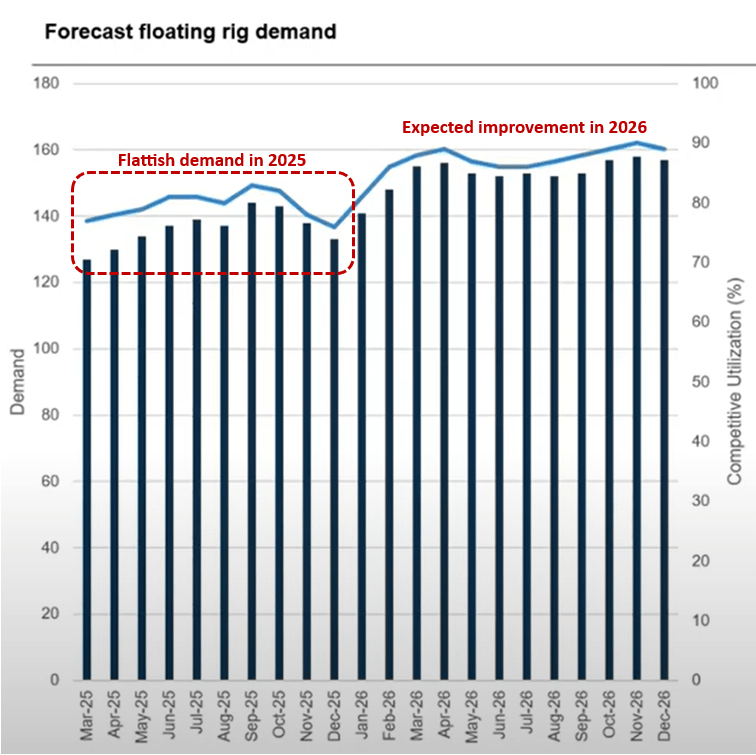

Even with prices where they are today, offshore activity is poised to pick up from 2026 onward. Various industry sources report that the current pipeline of deepwater projects is the deepest in a decade.

At current oil prices of ~$70 per barrel WTI, Esgian's forecast below reflects the wider expectation of a recovery beginning in 2026.

Source: Esgian Rig Analytics, Feb. 18, 2025.

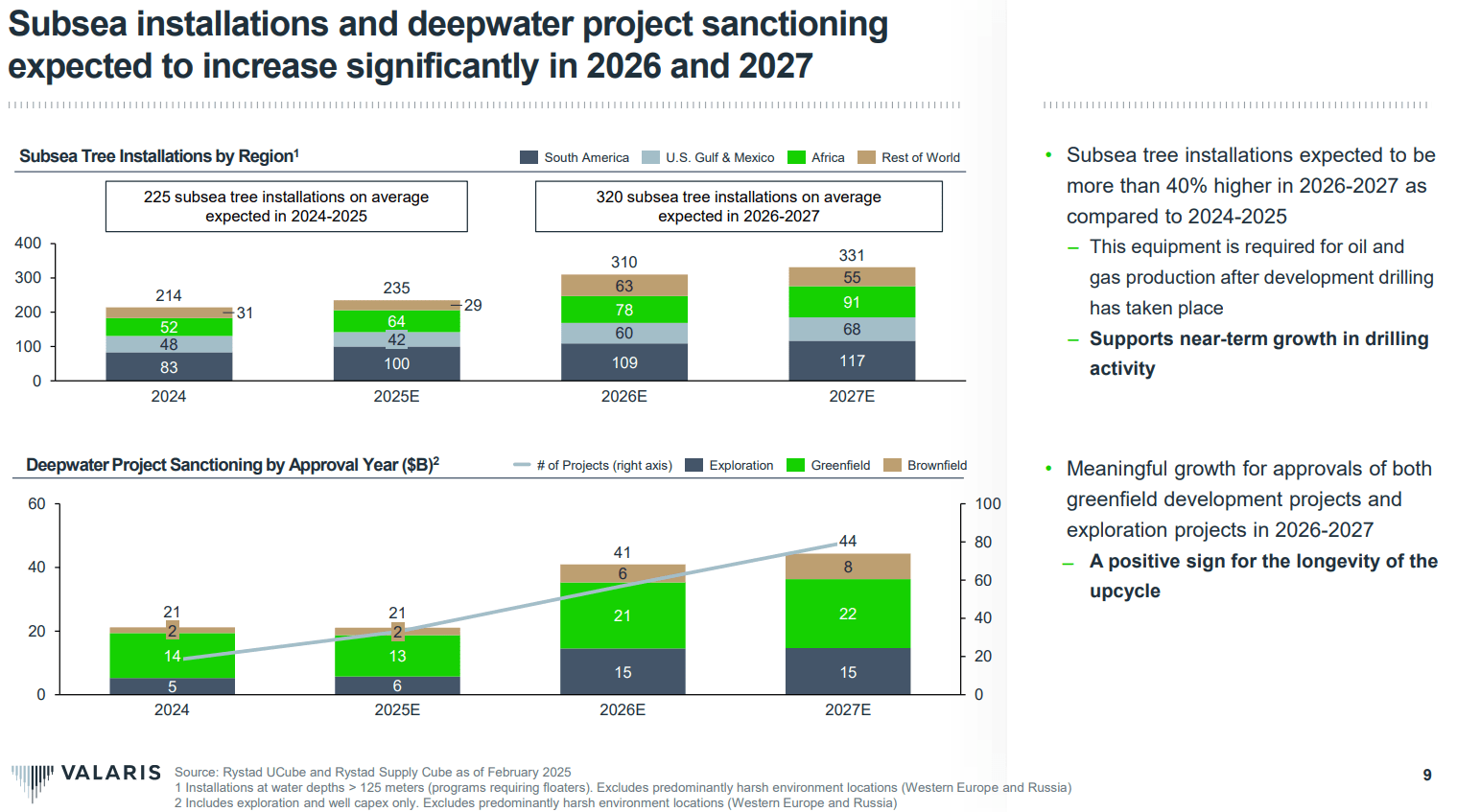

Beyond 2026, the outlook for offshore project sanctioning remains healthy. VAL includes the following slide in its investor presentation.

Source: Valaris March 2025 Investor Presentation.

By 2026 and 2027, VAL’s management expects project approvals to reach the highest levels in more than a decade and more than double the approvals anticipated for 2024 and 2025. The company should have ample opportunity to contract its currently uncontracted drillships and semisubmersibles at attractive long-term day rates.

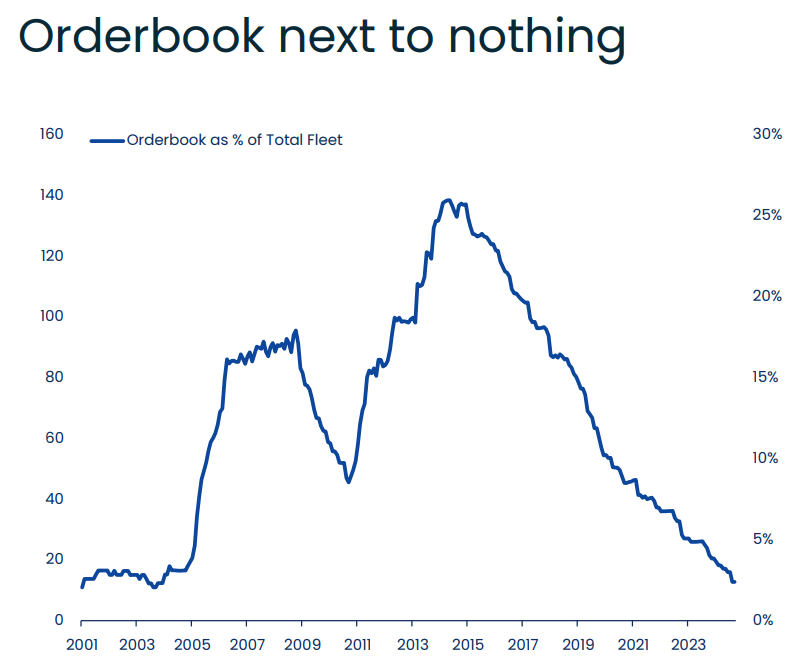

Increasing demand for offshore drilling services will meet increasingly constrained supply.

The current orderbook for offshore rigs is nearly nonexistent. The chart below shows the orderbook for jack-up rigs.

Source: Borr Drilling Investor Presentation, Jan. 2025.

In January, there were a total of ten jack-up orders, representing only 2% of the global fleet.

With few new rigs entering the market, increased rig demand will cause existing high-spec rigs to be contracted at higher day rates. After those vessels are contracted, the existing crop of idled rigs will be returned to service. Over time, older and obsoleted rigs will be scrapped.

Offshore Discipline is Holding

Given the improving macro backdrop, it’s encouraging that the industry isn’t seeing further weakening of day rates on new contracts. In fact, drillers have acted rationally in recent months, taking measures that align rig supply with demand instead of undercutting one another on pricing. For example, in February, VAL and its peer Noble (NE) announced fleet retirements that will shrink the supply of idle rigs.

These moves are not characteristic of a new industry downcycle. They indicate that the sector is poised to resume its upcycle once demand returns. And when demand does return, industry dynamics indicate that day rates will continue to improve.

For one, most of today’s global offshore rig fleet has been consolidated into the hands of the largest operators. The current global fleet includes approximately 56 high-spec drillships, 44 of which are owned by the major operators, VAL, NE, RIG, and Seadrill (SDRL). The 12 owned outside of this group are owned by smaller operators ripe for consolidation.

Consolidation among the major players will further enhance the industry’s competitive position. One more merger among the largest operators would bring the number of major high-spec drillship operators from four to three. RIG and SDRL reportedly discussed a merger last October. A three-player offshore drilling industry would significantly enhance pricing power among the remaining operators.

All the while, rigs will continue to depreciate, and idle rigs will be scrapped. As additional supply comes offline, offshore drillers will become price setters rather than price takers. Cash flow will inflect higher, and returns to shareholders will increase considerably.

Why Valaris?

Despite VAL’s atrocious stock price action over the past few quarters, not much has changed with regard to its fundamentals.

VAL’s stock rose from the low-$20s in 2021 to $80 in 2024. Over this timeframe, drillship day rates more than doubled, from $200,000s per day to the high-$400,000s. The shares were then cut in half, even though day rates have only fallen to the mid-$400,000s range.

At present, VAL is operating at a slight free cash flow surplus. The company’s backlog covers 94% of its management’s revenue guidance for 2025. It remains conservatively capitalized, which offers downside protection in the event day rates remain weak.

All in all, VAL offers investors the best combination of newer, high-spec rigs, low debt, and increasing profitability as old contracts expire and the rigs in its fleet are recontracted at higher day rates. The company owns 20% of the world’s seventh-generation drillship fleet. Outside of the two eighth-generation drillships, these vessels will be the first to be leased, as they provide the most capital-efficient alternative to E&P customers.

With only $700 million of net long-term debt, VAL can afford to be disciplined in recontracting its vessels. We would prefer that management exercise patience with its contracting rather than hastily sign low-priced deals. VAL’s track record on this front hasn’t always been stellar, but its behavior over recent quarters is encouraging.

VAL's relatively low levels of debt and interest expense enhance its pricing flexibility versus its more highly leveraged peers.

Insiders have been buying. On March 5, VAL's CEO Anton Dibowitz recently bought $250,000 of VAL stock at $33.91 per share. John Fredriksen of Frontline (FRO) fame is one of VAL's largest shareholders. Fredriksen also recently bought in the $30s through his Famatown Finance entity. He currently owns 10.56% of VAL’s shares and has an observer seat on the company’s board of directors. His influence is a positive for VAL shareholders.

In a bearish oil price environment where WTI remains below $80 per barrel, I expect VAL and its peers to continue to improve their pricing power. In such an environment, demand for offshore drilling services is likely to remain stable while supply continues to shrink. The industry will be characterized by fewer competitors over time.

New rig supply will remain a distant prospect. The only way new offshore vessels will get built is if day rates increase to levels high enough to justify a return on the investment based on dayrates and contract terms. Estimates by the major oil market consultancies and analysts vary, but they tend to be at least $700,000, with some as high as $1 million. The latter would actually be in keeping with the previous cycle’s highs adjusted for inflation.

Needless to say, at these rates, the owners of existing structures would earn obscene returns on their investments. Even if a newbuild cycle were to begin, it would take four years to build a new drillship. The lag between newbuild orders and deliveries will give VAL time to maximize its cash flow and return capital to its shareholders.

Valuation

From the perspective of net asset value, VAL is currently trading at a $3.5 billion enterprise value. It owns 15 floaters—comprised of drillships and semisubmersibles used in deep water—and 28 jack-ups operated in shallow water.

If we consider the floaters alone, VAL’s enterprise value implies $233 million per floater. For context, a newbuild floater would run north of $1 billion.

VAL also owns a fleet of 28 jack-up rigs, 23 of which are active. Borr Drilling (BORR) owns a fleet of 24 newer jackups, 21 of which are active. BORR has an enterprise value of $2.6 billion.

If we value VAL’s floaters at $500 million apiece and value its jack-ups using one-half of BORR’s enterprise value, VAL’s enterprise value would come to $8.8 billion—clearly not heroic by historical valuation standards. At that enterprise value, VAL shares would trade at $111, implying 192% upside from today’s price of $38.

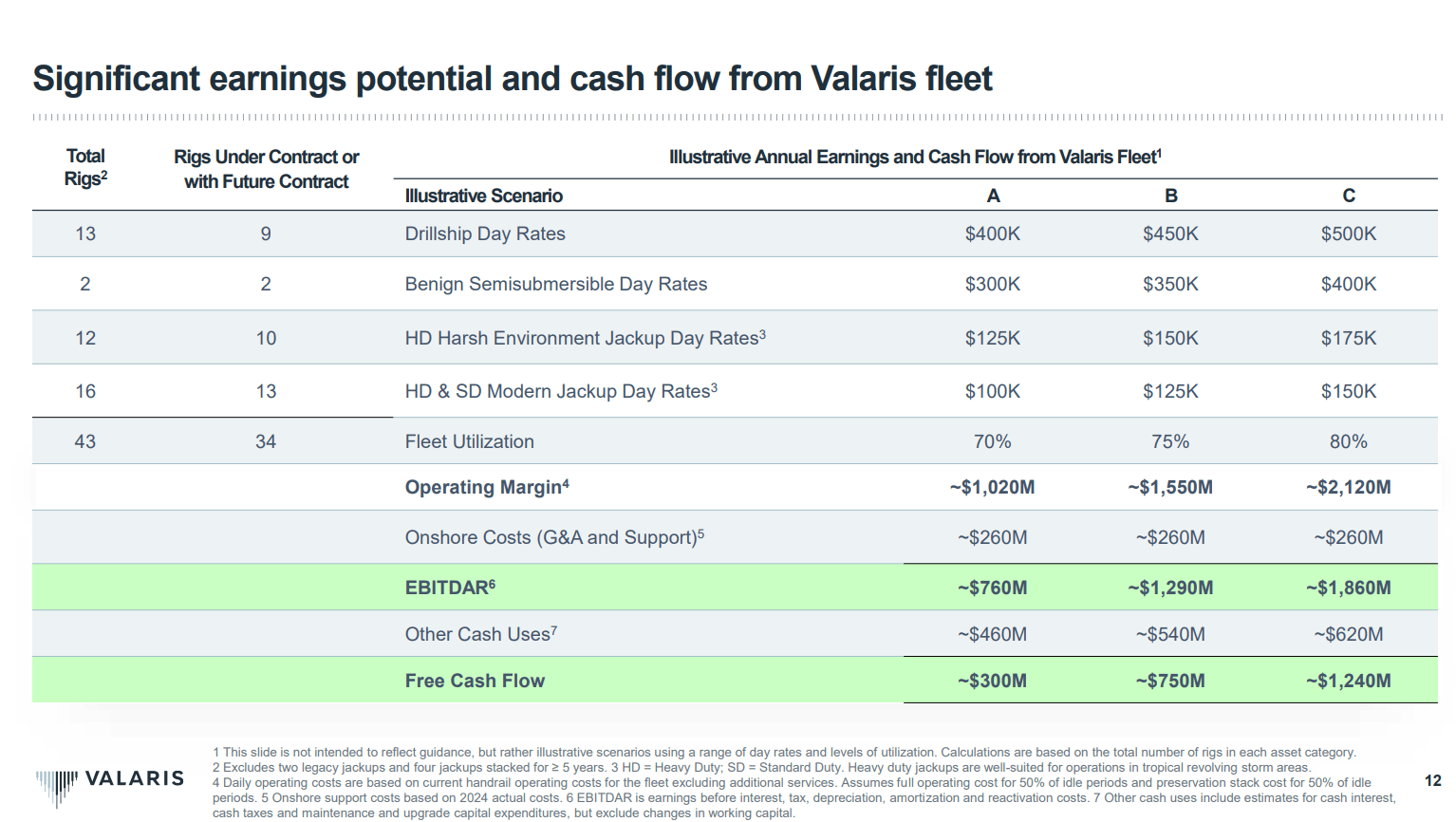

Turning to free cash flow, VAL includes the following slide in its investor presentation. The table illustrates how small changes in day rates equate to massive increases in free cash flow due to operating leverage.

These scenarios imply a stock price in the range between $34 and $142. With the stock at $38, they imply downside of 11% to upside of 274%.

Using my own cash flow model, if day rates remain flat at around $450,000 for VAL’s drillships and $280,000 for its semisubmersibles, and if its five inactive drillships returned to service, VAL would generate $364 million of free cash flow. If the shares traded at a 12% free cash flow yield, they would trade at $41.62, implying 10% upside. This is roughly what the market is baking in with the current share price.

If we consider scenarios where day rates approach the highs of the previous upcycle, the upside in VAL’s shares grows much larger. This scenario assumes day rates of $650,000 for drillships, $400,000 for semisubmersibles, $250,000 for harsh environment jack-ups, and $200,000 for other jack-ups. While high, these rates are well within the realm of possibility.

Assuming the currently idle rigs remain as such, and the active rigs are contracted at the last cycle’s highs, VAL would generate approximately $18.48 of free cash flow, implying a share price of $154 at a 12% free cash flow yield. If, instead, we assume VAL’s currently idle vessels also get contacted at the last cycle’s highs, the company’s free cash flow increases to $30.75 per share. At a 12% free cash flow yield, VAL shares would trade at $256, implying upside of 574%.

These valuations leave aside ARO Drilling, VAL’s joint venture with Saudi Aramco. The venture is building 20 rigs that will be contracted to Saudi Aramco. Both parties will make a $1.25 billion capital commitment to the venture. The joint venture generated $120 million in Adjusted EBITDA in 2024.

Risks

The primary risk to VAL investors stems from a prolonged bout of low oil prices that significantly reduces the free cash flow of the oil majors and national oil companies. One of the virtues of the offshore driller thesis is that, while it entails risk from macro forces—like any investment—its risks stemming from within the industry are unusually low, particularly for the energy sector.

Another potential risk is a shortage of attractive offshore prospects, which could cause the majors to reduce the capex dedicated to the space. I don’t consider this a very likely prospect. Exploration expenditures are likely to increase as the search for new prospects heats up. Combined with production enhancements stemming from advances in floating and production storage and offloading vessels (FPSOs), as well as seismic data analysis, I expect increased offshore exploration to bring new discoveries and development projects.

Conclusion

At their current price, VAL’s risk/reward is skewed overwhelmingly in the bulls’ favor. I’m adding the name to my roster of favorite non-income-generating energy stocks, along with Strathcona Resources (SCR:CA), Whitecap Resources (WCP:CA), and MEG Energy (MEG:CA). VAL’s shares recently bounced off their multi-year low, but they remain severely undervalued. Long-term energy investors should consider adding exposure now.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of VAL, VAL.WS, SCR:CA, VRN either through stock ownership, options, or other derivatives.