(Idea) ARC Resources - Conservative Play With Big Upside

Please see the previous write-up on ARC Resources:

By: Jon Costello

It’s “batten down the hatches” time in the oil patch. Front-month WTI now trades below $60 per barrel, the physical oil market is weakening, and global supply is set to significantly surpass demand for several quarters. To make matters worse, oil stock prices remain elevated relative to the negative near-term outlook.

I’ve learned that during times like these, when bargains are hard to find, it’s wise to tread cautiously. Favor companies that have conservative balance sheets, strong operational track records, and a reasonable stock valuation. If macro conditions improve, the shares should perform well. If, on the other hand, conditions worsen and pull the entire sector lower, the investor can sell their conservative holding and switch into a more aggressive, cheaper alternative to position for a cyclical recovery.

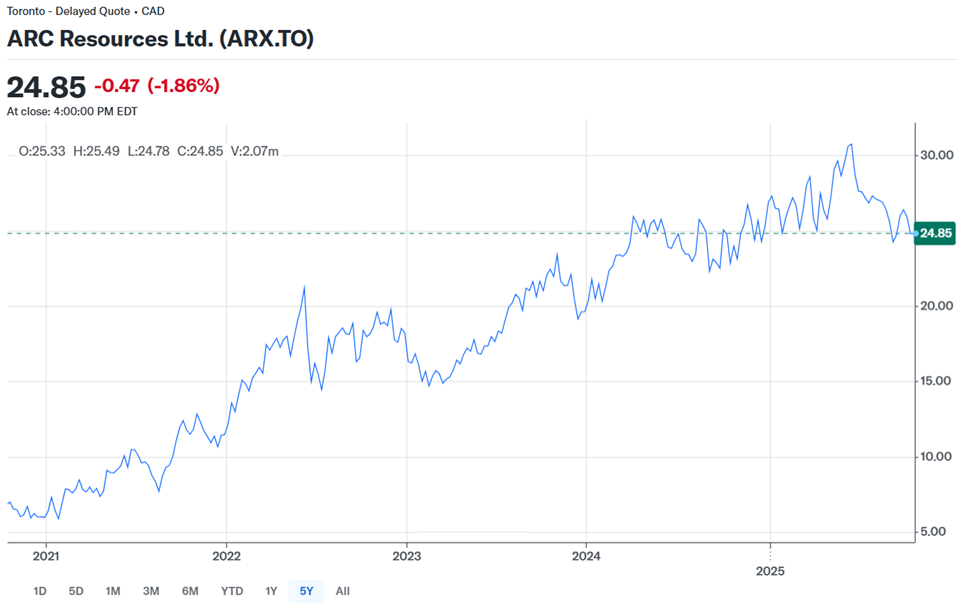

ARC Resources (ARX:CA) fits the conservative profile to a tee. ARC’s share price has been flat over the past 18 months.

Source: Yahoo! Finance, Oct. 16, 2025.

I expect the shares’ long-term upward trend to resume as macro and company-specific catalysts play out over the coming quarters and years.

In recent months, ARC shares were driven lower by the company’s lower quarter-over-quarter production and increased capex guidance. ARC also lowered its 2025 production guidance, reducing oil and condensate production by 8%, NGLs by 5%, and natural gas by 2%. Overall production is expected to fall by 5%.

The quarterly production decline was mainly due to natural gas curtailments in response to low prices, as well as a delay in the production ramp of its Attachie Phase I project. The higher capex is aimed at optimizing its newly acquired Kakwa acreage and preparing its Attachie asset for Phase II of its production growth.

All these negative developments are temporary. They are a rational response by the company to a difficult operating environment and necessary investments to support long-term growth. As conditions improve and production is brought back online, ARC shares are likely to trade higher.

The Macro Catalyst: Condensate and Natural Gas Exposure

ARC’s liquids production is comprised mainly of NGLs and condensate rather than crude oil. This benefits the company in several ways.

First, since its liquids production is a byproduct of natural gas production, its operating costs per Boe are lower than those of other liquids-weighted E&Ps. At the same time, the high liquid content of ARC’s production bolsters its top line compared to its gas-weighted peers, most of which have more “dry” gas in their production mix. The relatively high margins ARC achieves on its production make it one of the lowest-cost major oil and gas producers in North America.

Second, about a quarter of the company’s production consists of condensate, which has a particularly promising future in Canada.

As I detailed at length in my NuVista Energy (NVA:CA) article in August, Western Canada doesn’t produce enough condensate to satisfy its domestic demand. In fact, the region imports 40% of its condensate from the U.S. This condensate shortage in Western Canada causes prices to trade at a premium to WTI, significantly above the local Western Canadian Select price realized by the region’s heavy oil producers.

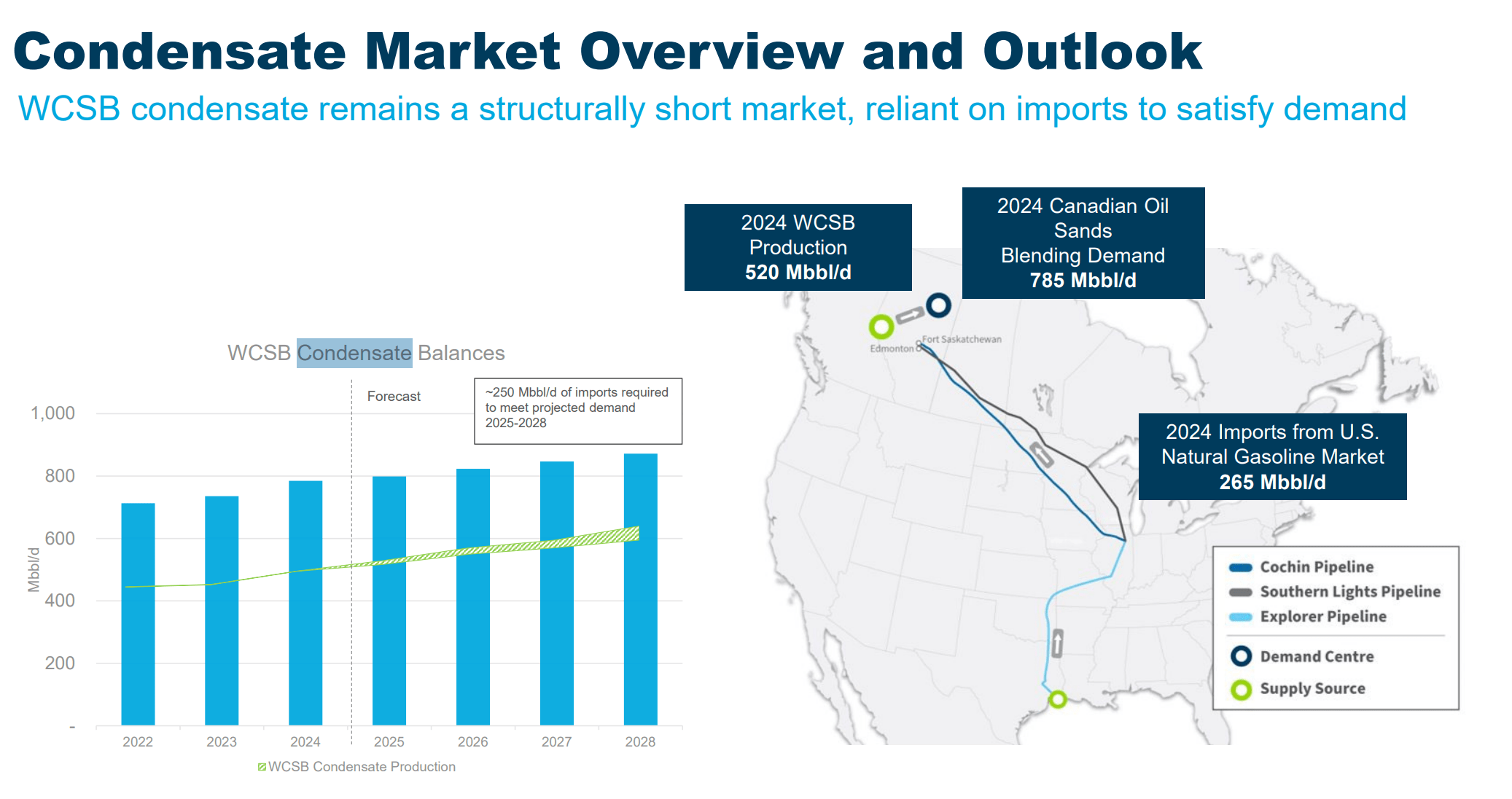

Western Canada’s condensate outlook remains robust. Condensate is used to dilute the bitumen produced in the oil sands, and recent growth in production has driven sharp increases in demand. As shown below, continued expansion will keep demand rising.

Source: ARC Resources Q3 2025 Investor Presentation.

ARC will benefit significantly from the structural condensate bull market. In the second quarter, condensate made up 57% of the company’s revenue despite representing only a quarter of its production. This is one reason I include it in the HFIR Energy Income portfolio.

The other key aspect of ARC’s macro story is its exposure to natural gas. Growing LNG demand for major liquefaction facilities set to start this November will help reduce the regional supply glut in the British Columbia Montney. Meanwhile, ARC’s agreements with Gulf Coast LNG producers such as Cheniere (LNG) will boost its price realizations.

In the event the widely promoted natural gas bull market takes hold, ARC will receive an outsized benefit relative to its Canadian oil and natural gas-weighted peers.