(Idea) ARC Resources

ARC Resources (ARX:CA) offers investors a conservative way to benefit from the structurally higher natural gas prices we expect over the coming years.

While natural gas supply has been more than ample over recent years, today's 102 Bcf/d gas market is about to undergo a whopping 11.4 Bcf/d demand boost from the arrival of LNG export terminals in the U.S. and Canada through 2027.

The chart below details the LNG export projects and when they are expected to enter service.

Source: EIA.

The sheer volume of additional gas demand is likely to increase the price of the marginal unit of gas production.

On the supply side, it is likely to accelerate the depletion of natural gas reserves and bring forward the point at which the U.S. shale basins plateau. Consider that natural gas production in the Fayetteville and Barnett shale plays plateaued and then began to decline once they produced half of their reserves. The Haynesville and Marcellus will suffer a similar fate—the only question relates to timing.

Another important demand factor known with less precision stems from increasing power burn. Economic and population growth, the renewables buildout, coal-to-gas switching, and the proliferation of AI data centers will all increase North American natural gas demand above and beyond the demand derived from LNG export facilities.

It is against this backdrop that ARC Resources shines. ARC offers investors a multitude of positives in a single stock. These include one of the lowest-cost production bases among independent North American E&Ps, returns on capital employed sustained in excess of 20%, a 12% free cash flow yield at current commodity prices on next year’s production, a conservative balance sheet, a diversified product mix between liquids and natural gas, a safe 2.8% dividend yield with prospects for significant increases, mid-single-digit percent annual production growth, and superb capital allocation featuring long-term dividend growth and share repurchases.

In light of all these positives, an investor would expect ARC shares to sell at a hefty premium to intrinsic value. But that’s not the case. In fact, we see 18% upside from the stock on next year’s production numbers, as well as significant production growth and share price appreciation over subsequent years. We value ARC shares at C$30.00, implying 25% upside from their current price of C$24.00.

ARC Resources Background

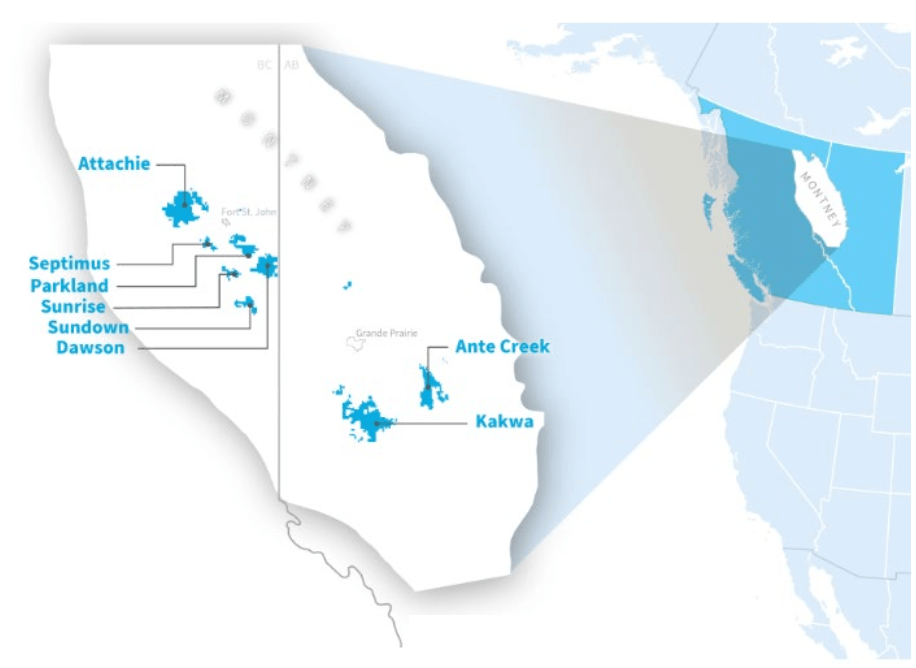

ARC stands out as the largest Montney producer of both oil and natural gas, as well as Canada’s largest condensate producer and its third-largest natural gas producer. In the first quarter, it produced 352,328 boe/d of oil and gas, which featured a 63%/24%/12% mix of natural gas/crude oil and condensate/NGLs.

Source: ARC Resources May 2024 Investor Presentation.

Operationally, the company executes well quarter after quarter. In the first quarter of 2024, its production beat analyst expectations of 345,000 boe/d, while cash flow and capex were in line with expectations.

ARC’s assets are capable of sustaining as much as 500,000 boe/d of production. Given management’s penchant for organic growth, we expect it to reach that point over the next decade without any production added from acquisitions.

Since 2014, the company has undergone a transition from a collection of fifteen distinct operating areas scattered across multiple regions of British Columbia, Alberta, and Saskatchewan to being focused exclusively in the Montney play in British Columbia and Alberta. The Montney is currently one of the hottest plays in Canada, and ARX operates a massive, one-million-acre asset base in the regions of the basin that produce crude oil, NGLs, condensate, and dry gas.

ARC has generally shunned major acquisitions. Instead, it has focused on narrowing its operational focus and growing reserves and production organically. The one exception came in 2021 when it acquired Seven Generations Energy—a liquids-weighted Montney E&P—in a C$2.7 billion all-stock deal. Before the deal, ARC produced 162,000 boe/d with a 76%/24% gas/liquids mix. At closing, the combined entity produced 340,000 boe/d, including 1.2 bcf/d of natural gas and 138,000 boe/d of liquids, for a 59%/41% gas/liquids split.

The all-stock deal was a masterstroke. It combined Seven Generations’ liquids-weighted production with ARC’s gassier production to create a Montney behemoth. It enhanced the flexibility of the company’s capex program in response to commodity price changes and allowed the cash flow generated from Seven Generations’ high-value liquids production to fund the growth of ARC’s underdeveloped but high-return Attachie asset, which is now the focal point of its long-term growth.

Growth Is Set to Continue

ARC’s overarching goal is to organically grow production while pursuing initiatives to enhance margins over the long term. Growth is currently focused on developing the company’s Attachie Phase I project. The project is expected to cost C$740 million and to add 40,000 boe/d of production comprised of 60% liquids by late 2024. Attachie Phase I is expected to drive full-year 2025 production to 388,000 boe/d, up 9.3% from 2024.

Longer-term, management’s five-year plan calls for the addition of Attachie Phase I to sustain the company’s production at approximately 390,000 boe/d through 2027. Over this period, the company plans to invest in Attachie Phase II. It expects Phase II to commence production in 2028, growing ARC’s production to approximately 425,000 boe/d. Through 2028, management is guiding for 150% growth in free funds flow per share—a 20% compound annual growth rate—with likely greater growth in free cash flow per share.

We tend to give short shrift to five-year plans, particularly with E&Ps. However, ARC’s track record of executing operationally and meeting its guidance puts serious credibility behind its stated expectations. The 150% free cash flow growth over the next five years could result in ARC shares more than doubling over that timeframe.

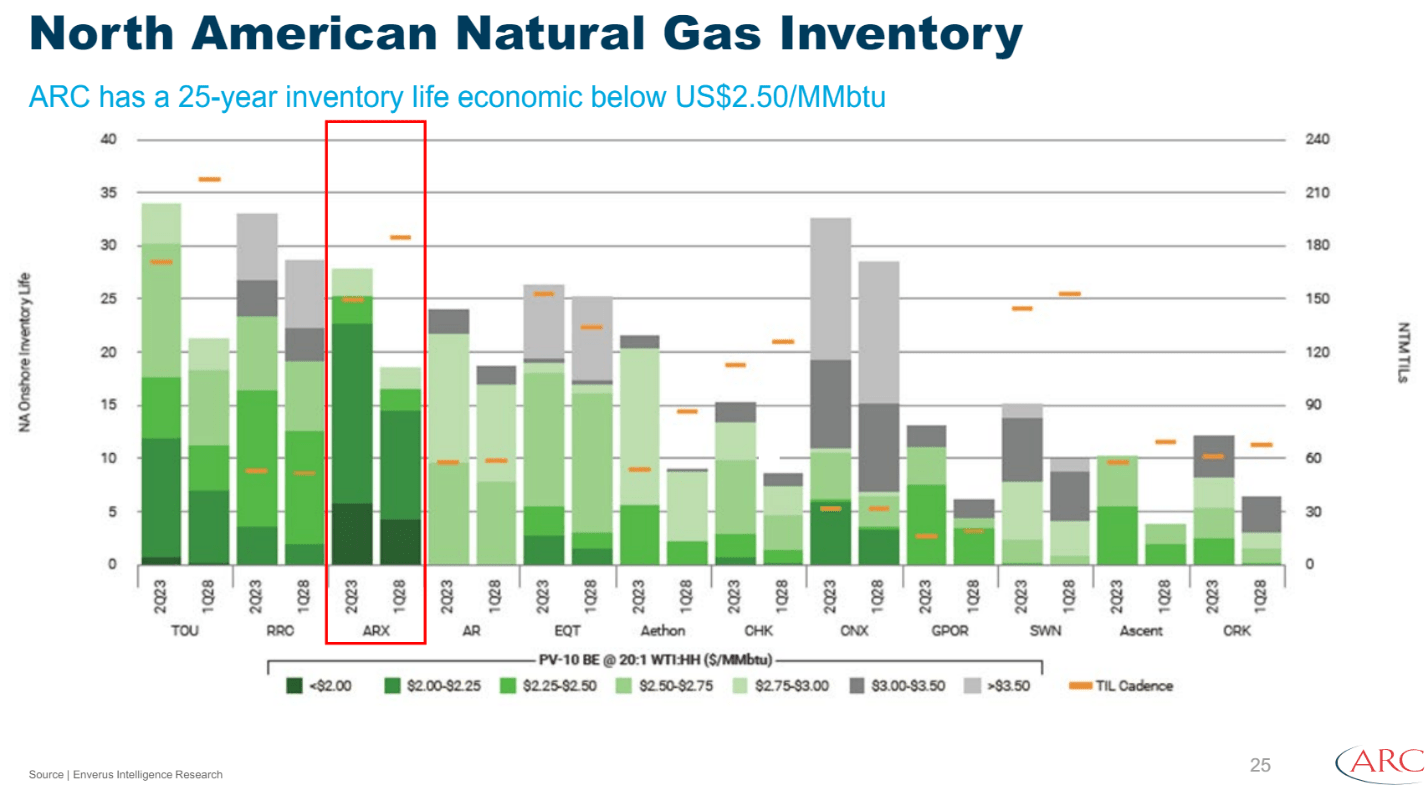

ARC’s deep inventory of low-cost drilling locations adds credibility to its growth plans. The chart below shows that ARC has the most attractive drilling inventory relative to its natural gas-weighted E&P peers in terms of break-even costs and inventory life.

Source: ARC Resources May 2024 Investor Presentation.

ARC’s unmatched inventory profile has enabled it to press ahead with growth even as many of its peers curtailed production in response to low gas prices. For instance, ARC did not curtail production at its Sunrise dry gas asset despite extraordinarily depressed AECO pricing because the asset’s economics could withstand the low prices.

Low-cost production is a foremost virtue among commodity producers, and ARC has it at scale.

Marketing Agreements Add Stability

ARC also benefits from long-term marketing agreements it has made with LNG producers. These agreements diversify its revenue stream, stabilize its realized pricing, and enhance its pricing upside.

These deals allow ARC to sell its natural gas through contracts in which pricing is indexed to benchmarks other than the perennially depressed AECO. The company has struck long-term LNG supply deals with LNG Canada for gas delivery starting in 2025, Cheniere Energy (LNG) for gas delivery starting in 2029, and, most recently, Cedar LNG for delivery starting in 2028. Each of these LNG producers seeks vertical integration to ensure their own customers that supply will always be available.

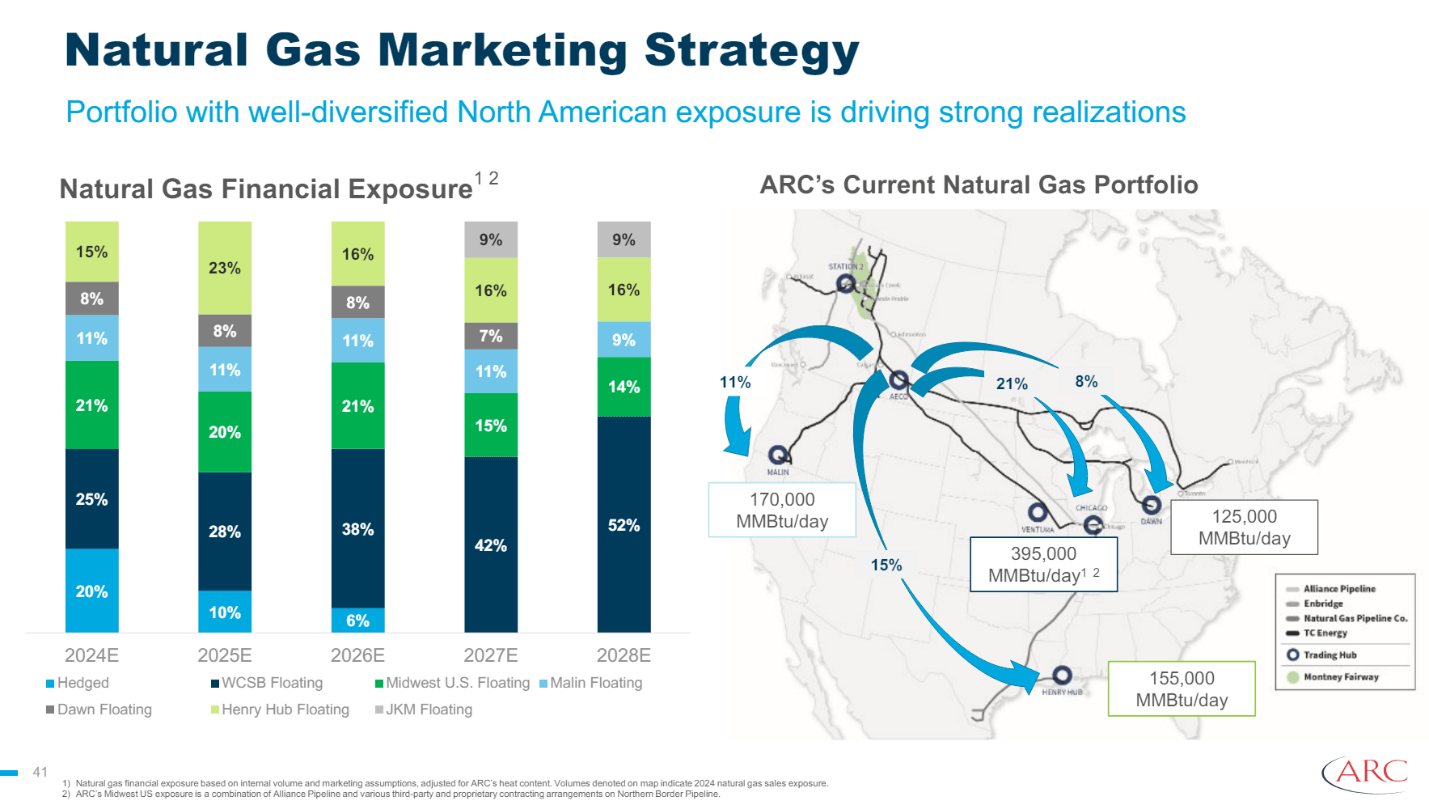

The makeup of its transportation and marketing portfolio is shown in the graphic below.

Source: ARC Resources May 2024 Investor Presentation.

For 2024, ARC has only 25% of its natural gas production tied to AECO. This year, it will realize approximately C$3.30 per mcf on its hedged pricing even as AECO has spent much of the year below C$2.00.

ARC is able to enter into these deals due to its long-lived reserve life, which can sustain 1.8 bcf/d of LNG feedgas for 10 years. Inclusive of management’s estimates of ARC’s unbooked drilling locations, that timeframe extends multiple decades.

ARC’s long-lived reserves provide it with a considerable competitive advantage in striking deals to stabilize cash flow, enhance cash flow certainty, and ultimately allow management to grow value for shareholders.

Outside of natural gas, ARC has an attractive growth opportunity in Canadian condensate market. Oil sands producers in the Western Canadian Sedimentary Basin already import 35% of the condensate they need to dilute their production into a transportable form. As oil sands production increases over the coming years, ARC will be able to sell its growing condensate production locally at prices near or above the price of WTI. The growth of ARC’s Attachie asset will increase the volume of condensate in its production mix, thereby increasing free cash flow per share amid sustained high oil and condensate prices.

Commodity Price Sensitivity & Valuation

ARC’s cash flow has significant torque to natural gas prices. Unlike most of its gas-weighted peers—such as Tourmaline Oil (TOU:CA)—ARC’s liquids weighting gives its cash flow torque to crude oil prices, as well.

The company’s free cash flow sensitivity to commodity prices is evident in its current guidance of 355,000 boe/d of production in 2024.

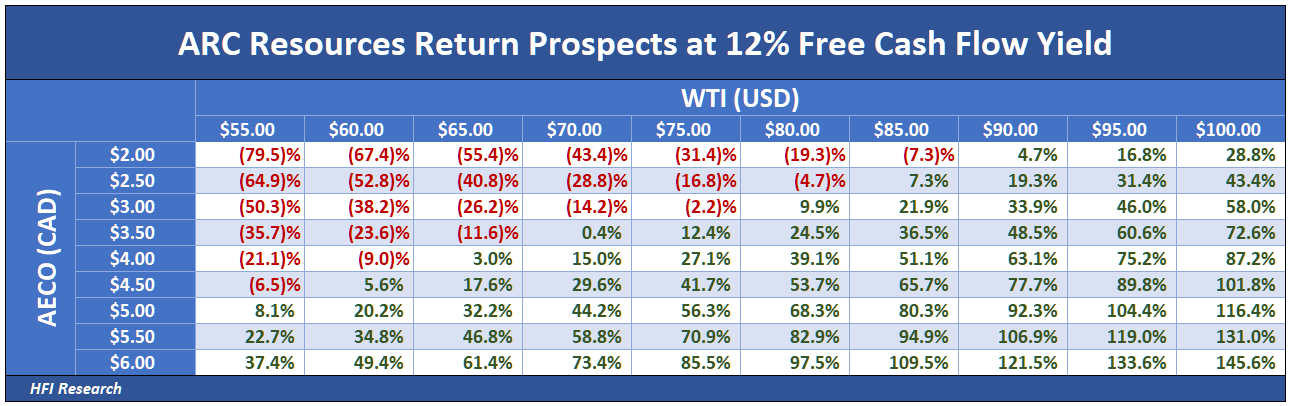

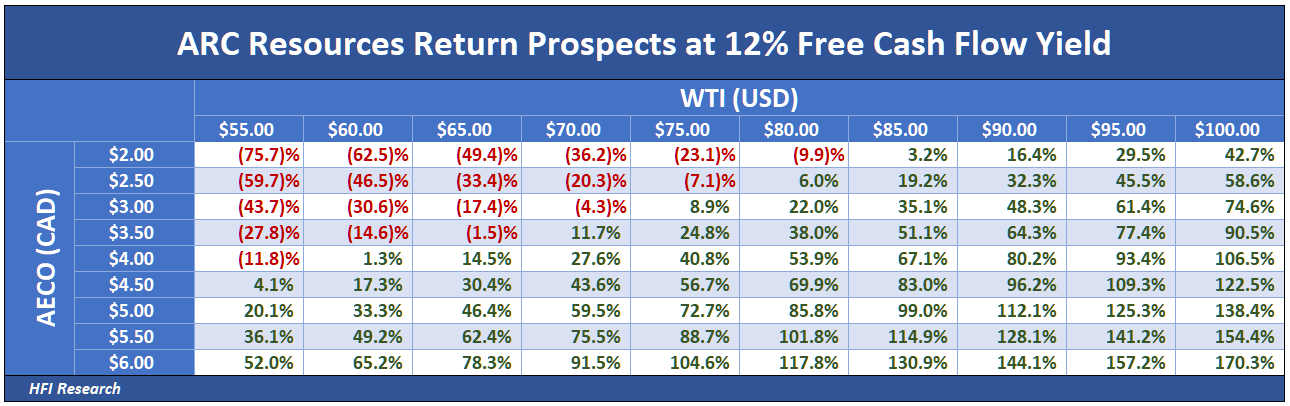

Below is ARC’s cash flow sensitivity under current commodity pricing, incorporating management’s 2025 production guidance and our C$1.4 billion estimate of maintenance capex.

ARC’s current free cash flow yield on its 2024 production and C$1.3 billion of capex suggests its shares are slightly overvalued. Assuming current commodity prices, the shares trade at a 10.8% free cash flow yield. We consider 12% to be an appropriate free cash flow yield for an E&P, hence the overvaluation.

However, the picture brightens if we incorporate management’s 2025 production guidance of 388,000 boe/d into our valuation. At current commodity prices and C$1.4 billion of maintenance capex for 2025, the shares currently trade at a 12.1% free cash flow yield. Based on 2025 numbers, we consider them to be fairly valued.

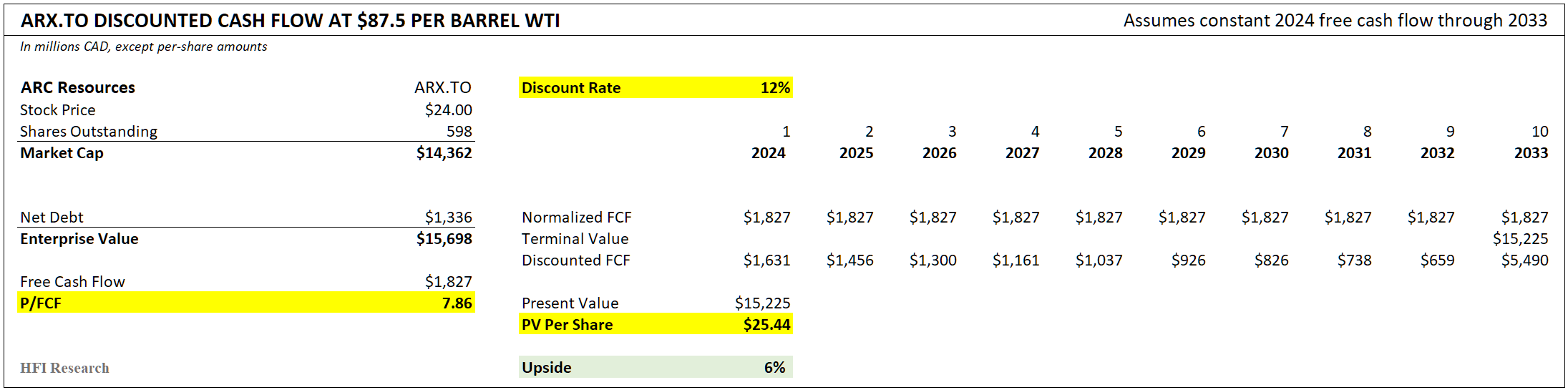

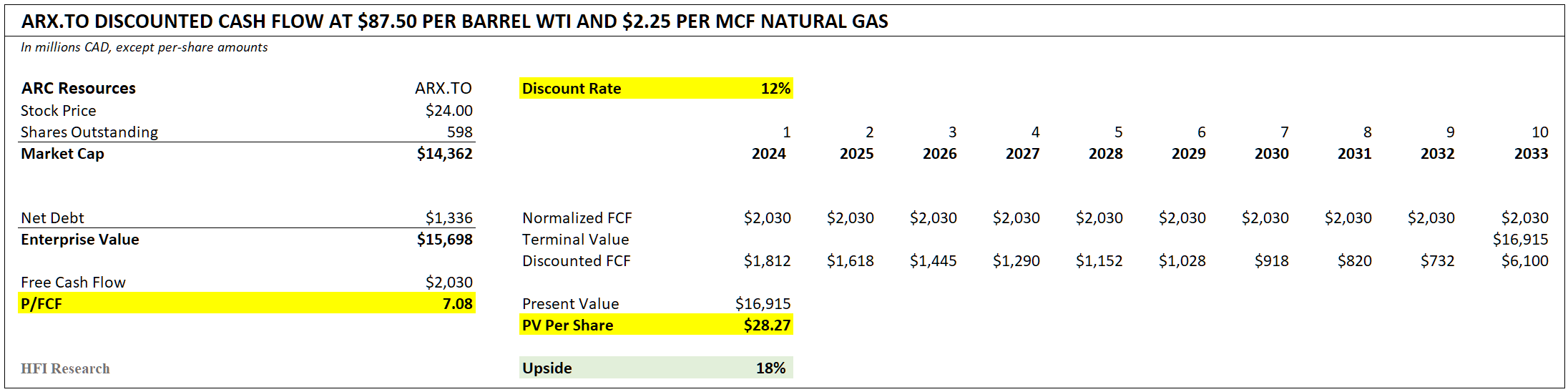

Using our commodity assumptions of $87.50 per barrel WTI and C$2.25 per mcf natural gas and maintenance capex of C$1.3 billion, our discounted cash flow valuation implies ARC shares are worth C$25.44, for 6% upside from ARC’s current share price of C$24.00.

This valuation indicates that while the shares aren’t cheap, they aren’t undervalued, either.

The shares’ upside increases considerably if we assume 2025 production of 388,000 boe/d and C$1.4 billion of maintenance capex. In this case, using next year’s numbers, they offer 18% upside.

ARC’s production growth will drive its value per share higher in 2026 and beyond, while share repurchases can add to that value. The extremely high probability that ARC grows its production profitably in the mid-single-digit percent range over the long term is the primary margin of safety for buyers of ARC shares at the current share price. It’s why we’re comfortable valuing ARC shares at C$30.00, which provides a 20% margin of safety on a purchase made today.

ARC’s stock offers more upside than that of its highest-quality E&P peers, including Tourmaline and Canadian Natural Resources (CNQ). Its greater liquids mix enhances its upside amid an oil price bull market, while reducing its downside relative to TOU amid a long-term downturn in natural gas prices. Its more reasonable valuation gives it more upside and less downside relative to CNQ.

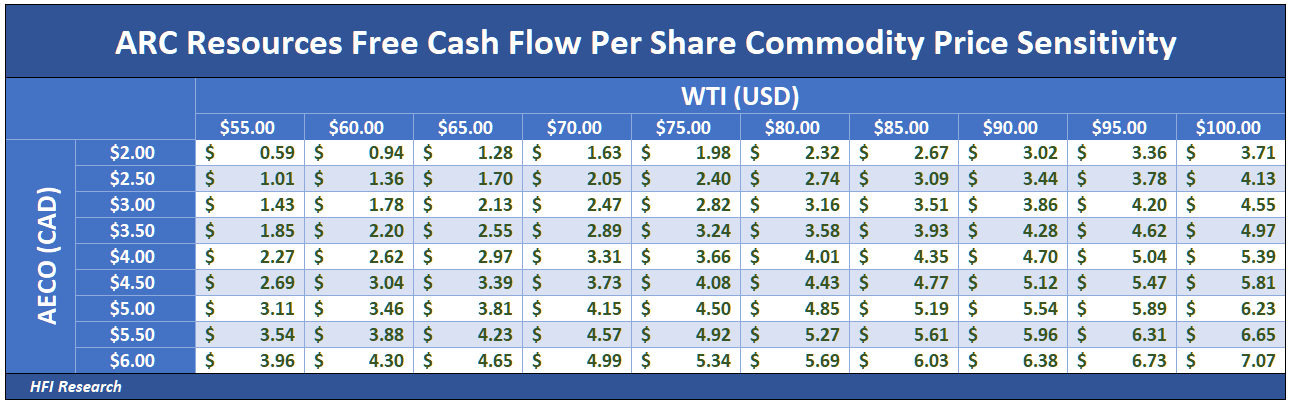

An important feature for ARC shareholders is the minimal risk of permanent value destruction amid a severe downturn that brings about a plunge in commodity prices. If ARC were to slash its capex to maintenance levels, its low-cost production and 62%/38% mix of natural gas to liquids will cushion its cash flow even if oil prices decline to $50 per barrel and gas prices fall below C$2.00 per mcf at the same time.

The table below shows that free cash flow per share remains positive amid extremely low commodity prices. This is as good as it gets among independent North American E&Ps.

ARC will be one of the last E&Ps standing in even the harshest commodity price environments. This attribute makes it one of the conservative E&P equity investments in North America. It’s also a reason why we’d be comfortable owning its shares with a relatively slim margin of safety compared with some smaller, more out-of-favor E&Ps.

Conclusion

ARC’s high quality puts it in the rarefied league of Tourmaline Oil and Canadian Natural Resources as some of the best E&P stocks in North America. Its low-cost production, steady growth in the low-single-digit percentage range over at least the next five years, deep drilling inventory, diversified product mix, and outstanding capital allocation make it a true energy stalwart. ARC is also more likely than its large-cap, high-quality E&P peers to be acquired at a premium to its trading price due to its smaller enterprise value of C$16.7 billion.

These factors should cause ARC’s shares to trade at a premium to intrinsic value, but when long-term prospects are considered, its shares are undervalued, with 25% upside to our C$30.00 valuation. ARC will perform well in either an oil or natural gas bull market, and they’re likely to significantly outperform in the event of the latter.

Whatever the future holds for commodity prices, however, given the bullish long-term macro outlook for both oil and gas, we're confident that investors who buy ARC shares around their current price and hold them over the next five years will generate attractive total returns.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.