The Oil Math And Why The Broader Market Is Crazy To Ignore It

HFIR's head of ideas, Jon Costello, shares his thoughts on the oil math.

By: Jon Costello

The oil market is undergoing its largest supply disruption in history. The disruption has opened up an approximately 8.5 million barrels per day (bpd) net supply shortfall in today’s 103 million bpd global oil market.

Looking at stock prices and oil prices in isolation, however, one would never guess at the severity of the supply crisis. In fact, oil and equity markets are behaving as if a rapid resolution is at hand. WTI sits near $102, Brent near $110, with future months trailing downward rapidly in a sequential manner. December Brent futures trade below $80, reflecting roughly $34 of backwardation that prices in near-term normalization. Meanwhile, the S&P 500 is hitting all-time highs regularly.

In my view, both prices are wrong. As long as the supply disruption remains in effect, the historically strong inverse correlation between oil prices and inventories will exert upside pressure on prices; it’s only a matter of time. This outcome has various implications for investors, even as many ignore them.

At a minimum, current oil and stock prices fail to factor in the broader impact this disruption will have on the global economy and, by extension, U.S. corporate earnings and stock prices. Brent sustained above $100 will tax every consuming economy. The earnings of U.S. multinationals, including the megacap technology names that dominate the S&P 500, are exposed to a global growth shock that is not priced in at all. Nevertheless, the longer the outage continues, the higher the oil price will rise, forcing demand curtailment, which increases the risk to corporate earnings and stock prices. For these reasons, I believe investors should adopt a more defensive positioning and remain overweight in the energy sector.

The Disruption: 8.5 Million bpd of Crude is Off the Market

The U.S. and Israel launched their attack on Iran on February 28. In response, the Islamic Revolutionary Guard Corps (IRGC) formally closed the Strait on March 27. Since then, transit through the Strait has been minimal. Kpler data show transit down approximately 92%.

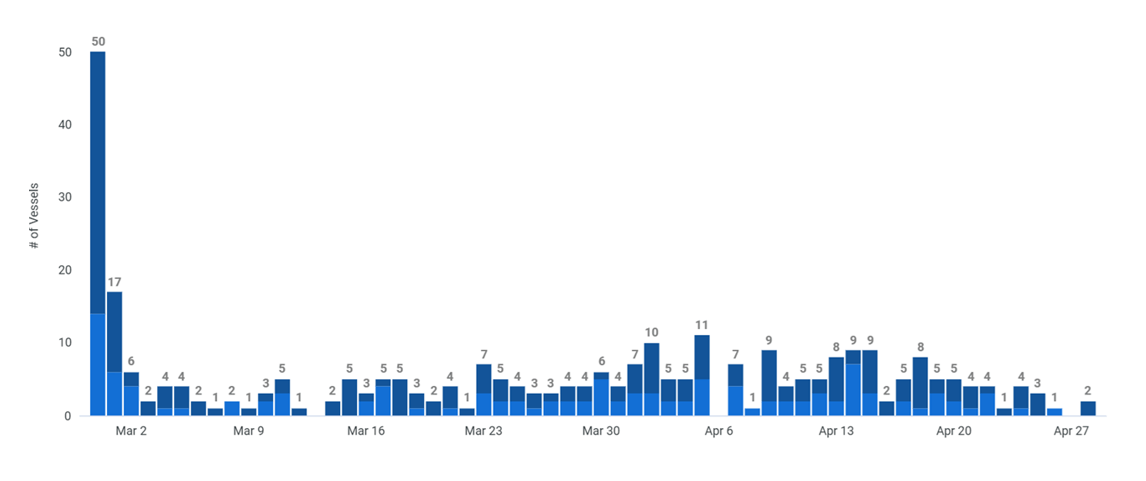

Source: Kpler, April 29, 2026.

S&P Global Market Intelligence has counted just 21 tankers transiting the Strait between February 28 and late April, against more than 100 ships per day before the conflict.

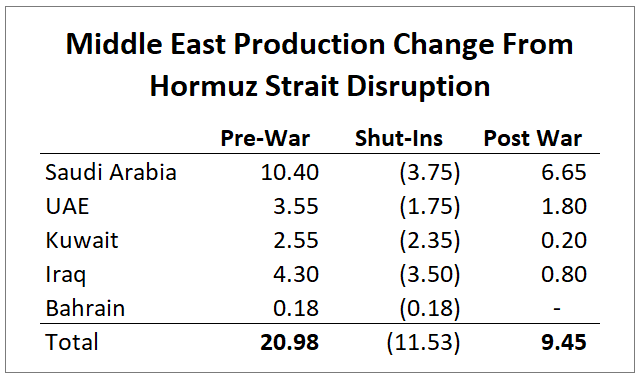

The closure of the Strait and the egress constraint it imposes on Middle East exporters has caused Saudi Arabia, the UAE, Iraq, Kuwait, Iran, and the smaller Gulf producers to shut in a cumulative 11.5 million barrels per day, more than 11 percent of the global oil market. Shut-ins by country are detailed below.

Source: HFI Research, April 20, 2026.

Some supply continues to reach the market through alternative routes, such as Saudi Arabia’s East-West Pipeline to Yanbu, the UAE’s ADCOP pipeline to Fujairah, and Iraq’s Kirkuk-Ceyhan pipeline to the Mediterranean. These workarounds are the means by which the 9.5 million bpd now being produced reaches the market. The volume is significantly less than the pre-conflict production of 21 million bpd, but enough to prevent a complete collapse of Middle East exports.

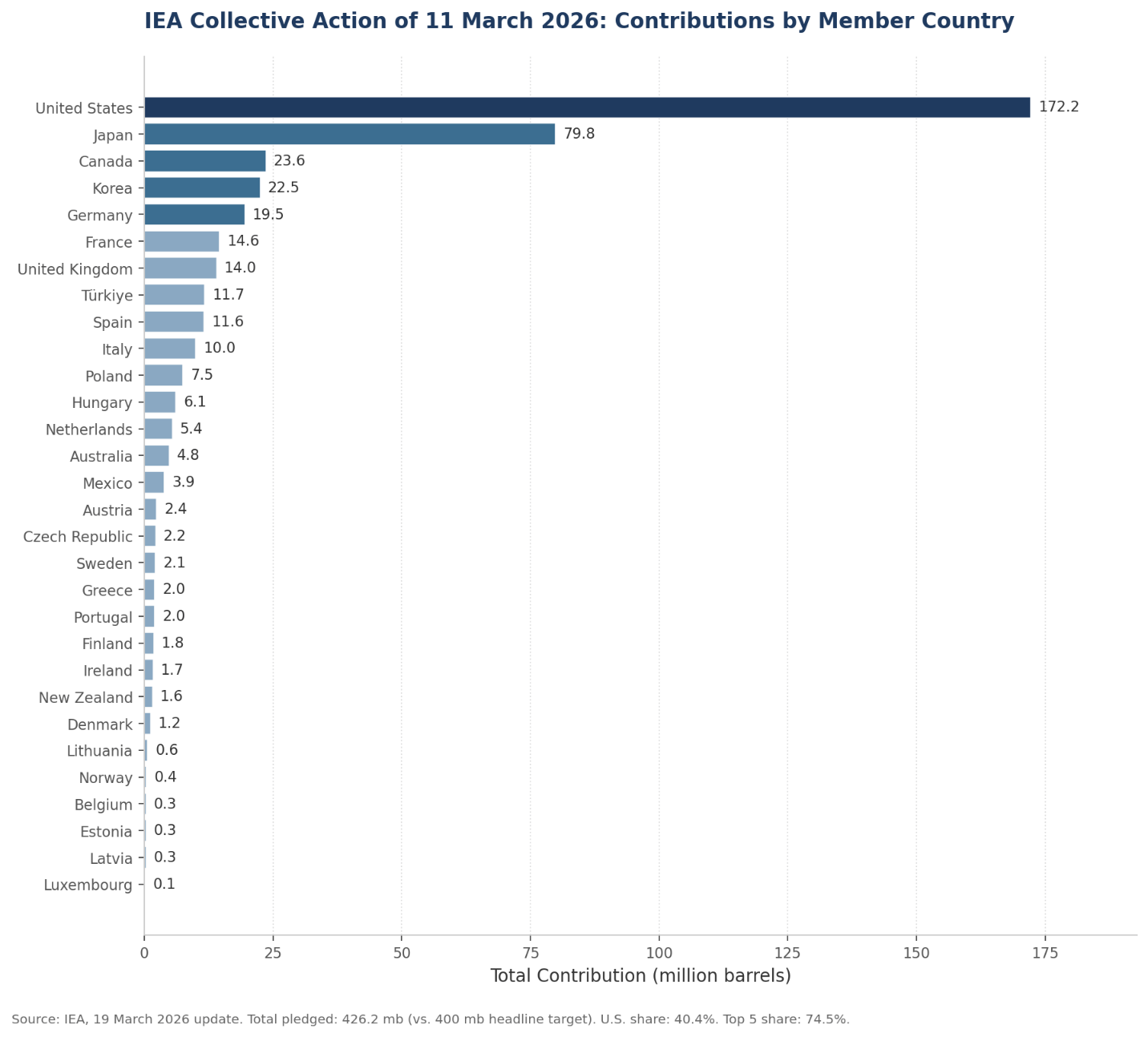

Strategic Petroleum Reserve (SPR) releases have managed to fill a portion of the supply shortage. The 32-member countries of the International Energy Agency (IEA) agreed on March 11 to a coordinated release of 400 million barrels of strategic reserves, the largest in the agency’s history. The U.S. is contributing 172 million barrels of the sum. Combined releases over the planned 120-day window add roughly 3 million barrels per day to global supply, of which the U.S.’s share is 1.4 million.

Source: IEA. March 19, 2026.

Even with the SPR, the rolling oil supply shortfall stands at a gargantuan 8.5 million bpd. It falls on inventories to absorb this difference. JPMorgan estimates that global observable inventories drew at 7.1 million barrels per day in April, after having drawn 4.0 million in March, for a cumulative draw of roughly 330 million barrels over two months.

As the inventory cushion is eroded, demand reduction will be the next factor to balance the oil market. This is already happening. JP Morgan estimates approximately 4.3 million bpd of forced demand losses in April, mostly in Asian and African importing nations that lack refinery capacity and have run out of fuel regardless of price.

Inventory drawdowns and forced demand destruction have so far done the work of balancing near-term supply and demand. However, the inventory part of that equation is about to run out.