An update on Strathcona Resources.

Our take on the SCR/MEG offer.

By: Jon Costello with input from Wilson

Note: Dollar values in this article refer to Canadian dollars unless otherwise specified.

Strathcona Resources (SCR:CA) (OTCPK:STHRF), a core holding of our HFIR Energy Income Portfolio, dominated the E&P headlines this week. The company’s numerous bold moves underscore its ambitions to become a premier Canadian heavy oil E&P.

A quick summary of events is as follows: Wednesday evening, SCR announced the sale of its Montney conventional oil and natural gas assets for $2.84 billion and the Hardisty Rail Terminal for $45 million. Then on Friday, SCR announced its “intention to commence” a bid to acquire MEG Energy (MEG:CA)(OTCPK:MEGEF) for $23.27 per share, which represents a 9.3% premium to MEG’s previous-day closing price of $21.30. SCR also disclosed that it had acquired 23.4 million MEG common shares, equivalent to 9.2% of the company’s outstanding shares year-to-date through open-market purchases as of May 5.

Today, SCR shares traded 2.1% lower, to $30.26, while MEG shares have gained 18.7% to close at $25.29, 8.7% above SCR’s proposed offer price. The market’s reaction indicates that the deal won’t get done at the offer price and that higher offers for MEG could be forthcoming.

I own SCR shares through the HFIR Energy Income Portfolio and MEG shares through other funds I manage. For SCR, the sale of Montney assets was brilliant. I’m significantly more bullish about the long-term outlook for oil prices than natural gas prices, and as an investor who plans to hold SCR for years, I believe I’ll do better with a pure-play heavy oil producer than a more diversified oil and natural gas producer.

As a MEG shareholder, I’m less enthused. SCR’s proposed MEG offer is far too low to be taken seriously. No MEG shareholder in their right mind will support this deal. Eric Nuttall, a major MEG shareholder, has already registered his opposition to the deal, and other large shareholders are likely to follow.

In the end, I expect SCR’s bid to be successfully opposed.

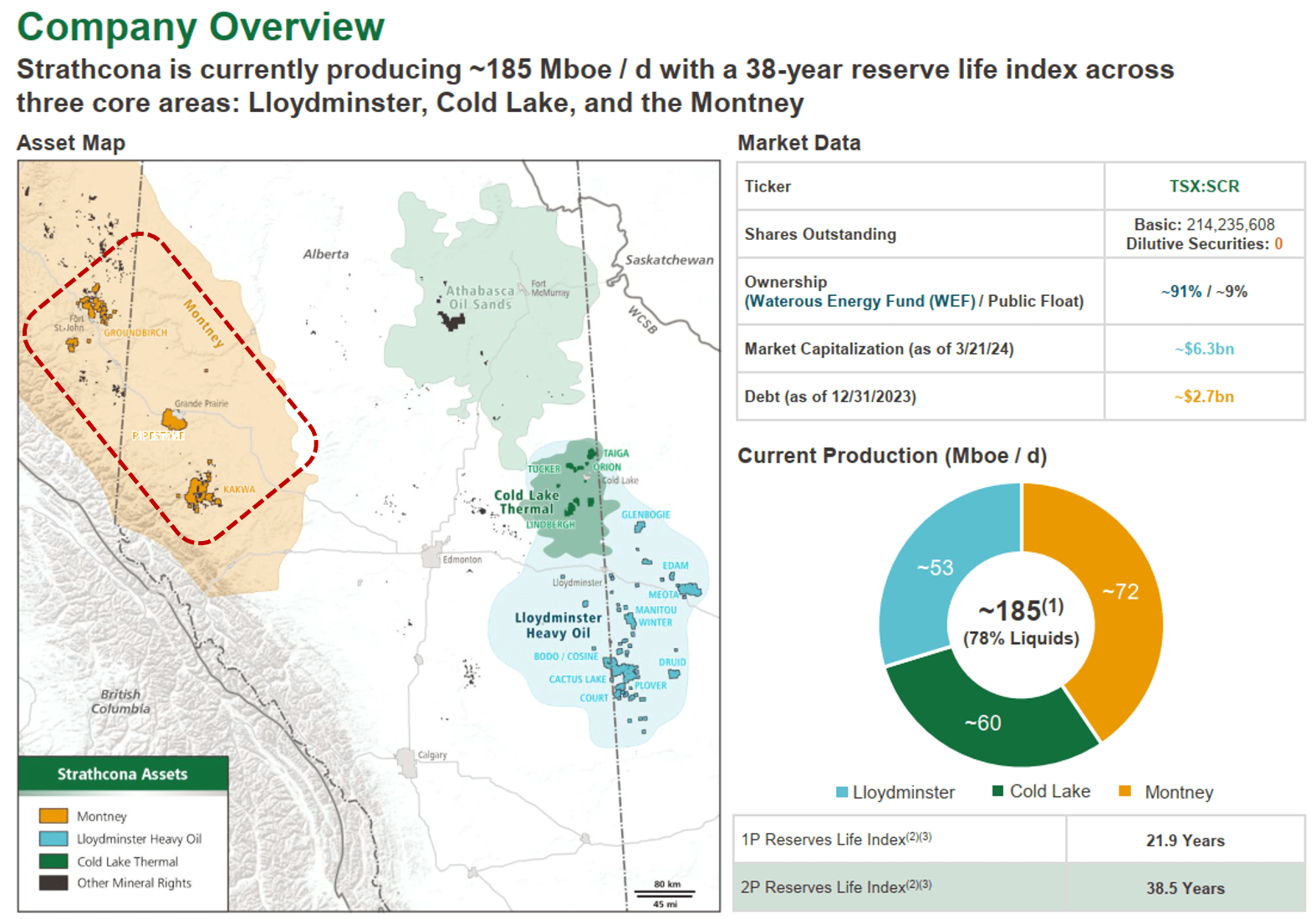

SCR's Montney Asset Sale

SCR’s sale of its Montney assets was a masterstroke. The $2.84 billion in proceeds represent half of SCR’s market cap but account for only 12% of its earnings. The proceeds will cause SCR’s net debt to fall from $2.9 billion to approximately $50 million.

The assets were sold to ARC Resources (ARX:CA), Tourmaline Oil (TOU:CA), and Canadian Natural Resources (CNQ). The deals are expected to close by July. They are shown within the red-dotted line on the map below.

Source: Strathcona Resources March 2024 Investor Presentation. Red-dotted line added by author.

SCR emerges from the sale as a pure-play oil sands producer. Its natural gas weighting falls from 29% to zero. Furthermore, the deal will lower SCR’s breakeven cost per barrel, which had been higher than its oil sand peers. A lower breakeven cost will be advantageous if oil prices remain depressed over the coming quarters.

Arguably the biggest coup SCR scored in the deal was the attractive prices for which it sold its Montney assets.

SCR sold its Pipestone asset to CNQ for $850 million, approximating PDP value. The deal represents a reasonable price but provides CNQ with development upside. SCR isn’t interested in developing natural gas-weighted resources, so its sale to a company that places a higher priority on developing the assets was a smart move.

SCR sold its Kakwa assets to ARC Resources—another large holding in our HFIR Energy Income Portfolio—for $1.695 billion. The assets produce approximately 150,000 boe/d and include two natural gas processing plants. Like the Pipestone assets sold to CNQ, the remaining drilling inventory of the Kakwa acreage is heavily weighted toward natural gas and NGLs.

SCR also sold its Groundbirch asset in the Montney to Tourmaline for a relatively pricey $292 million in Tourmaline common shares.

The divested Montney assets were contiguous with the existing assets of each respective buyer. For example, ARC Resources’ purchase of SCR’s Kakwa asset completes its consolidation of the core of the play, as shown below.

Source: ARC Resources Press Release, May 15, 2025.

Since acquiring contiguous acreage allows the buyers to quickly realize cost synergies, they can justify higher bidding prices.

Moreover, the buyers are also among the most sophisticated E&P operators. They will wring far more value from the assets than less sophisticated peers, which is another factor that allows them to bid richly.

SCR’s $2.84 billion asset sale represented 145% of the assets’ $1.159 billion PDP PV-10 value and a 22% premium to the assets’ $2.322 billion proved reserve value. The sales price was boosted by the presence of infrastructure and natural gas processing plants that accompanied the acreage.

By disposing of its Montney asset, SCR extended its proved reserve life by six years, from 23 years to 29 years. It extended its 2P reserve life index by ten years, from 40 to 50 years. SCR will emerge from these transactions with one of the longest reserve lives of North American oil and gas producers. The transaction also lowers the company’s corporate decline rate and improves its capital efficiency.

In light of SCR’s strategic priority to focus on oil over gas, it’s tough to find any negatives about its Montney asset sale. The only notable negative is that its sale of its condensate assets used to dilute its heavy oil represents the loss of valuable vertical integration.

Don’t Overlook the Rail Terminal Purchase

In a separate deal, SCR acquired the Hardisty Rail Terminal, the largest crude-by-rail terminal in Western Canada.

The terminal was formerly owned by USD Group (OTCPK:USDP) in its diluent recovery joint venture with Gibson Energy (GEI:CA) and ConocoPhillips (COP). The terminal has throughput capacity of 262,000 bbl/d, though year-to-date it’s only shipped 50,000 bbl/d.

This was an outstanding bargain purchase by SCR. SCR claims the terminal has a replacement value of $200 million, but when the prospects for its Diluent Recovery Unit improve, I suspect the returns from the asset will boost its value far above $200 million.

SCR’s ownership of the terminal is a brilliant strategic move. The Western Canadian Sedimentary Basin (WCSB)—where most Canadian oil is produced—currently has sufficient egress capacity to transport all its production. However, once the TMX pipeline reaches full capacity over the next two years, the basin will once again face egress constraints that cause WCS prices to trade at a greater discount to WTI. The difference between the two benchmarks has to widen to a point at which it incentivizes rail transport.

SCR’s ownership of a crude-by-rail terminal with greater capacity than its total corporate production improves its cost structure relative to its large Canadian oilsands peers who rely on third parties for long-haul transportation. It also insulates SCR from major blowouts in the WTI-WCS differential that occur from time to time in the WCSB. Memories of the painful 2018 episode are still fresh. When SCR’s peers are suffering financially from the next WTI-WCS blowout, its relative outperformance will allow it to execute acquisitions for assets or companies on the cheap.

Next Up: SCR’s Bid for MEG Energy

Another positive from SCR’s asset sale is its emergence with a cash war chest with which it can pursue new deals.

Witness today’s news.

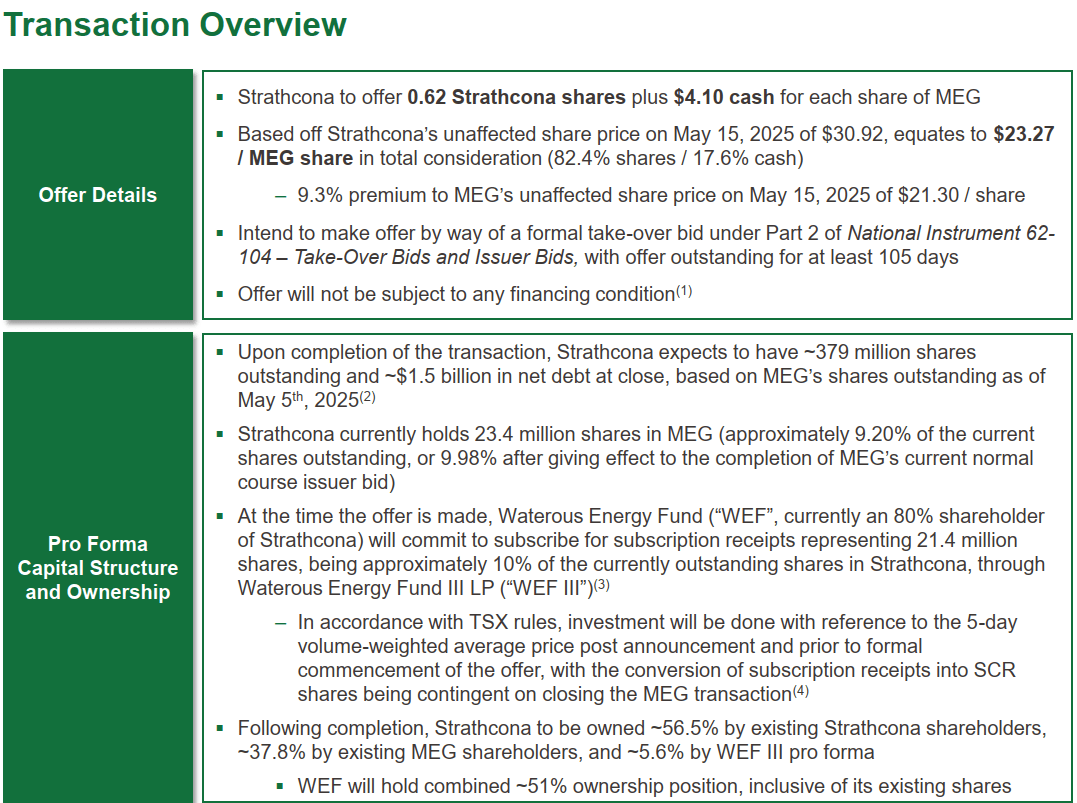

SCR’s $6.9 billion proposed offer for MEG came as a complete surprise in the Canadian oilpatch. SCR provides a summary of its offer in the graphic below.

Source: Strathcona Resources MEG Combination Presentation, May 15, 2025.

SCR is proposing an offer of 0.62 SCR shares and $4.10 in cash for each MEG share. The consideration is equivalent to $23.27 per MEG share, a 9.3% premium to its closing price of $21.30 on Thursday, May 14.

This offer won’t be taken seriously by any MEG shareholder, director, or executive. MEG has already spurned the deal. In fact, it has turned down at least one offer from large-cap peers in recent years that was far superior to what SCR offered today.

Nevertheless, today’s events are clearly a positive for MEG’s shareholders. SCR’s offer will cause investors to take a closer look at the tremendous value that exists in Canadian heavy oil assets. As that value is more widely appreciated, the stocks of MEG and its large-cap oil sand peers are likely to trade at higher multiples. I’ve often been bewildered at the significant discount to which Canadian oil-weighted E&Ps have traded relative to U.S. shale E&Ps. Perhaps that discount will shrink, or even shift to a premium, as more investors appreciate value and bid the Canadian names higher.

As for SCR, the company stands to win in any outcome. Its purchase of 9.2% of MEG shares throughout 2025 at discounted prices will allow it to profit even if it loses its bid for MEG. Consider, for instance, that year-to-date, MEG shares have traded at an average price of $22.65. Today, they hovered around $25.00, representing an attractive annualized gain over the few months that SCR has held its MEG shares.

Since April 1, however, MEG shares have averaged $20.64. Given SCR’s impeccable nose for value and aggressive approach to acquiring underpriced assets, I suspect the company’s cost for its MEG shares is closer to $20 than the 2025 average of $22.65. It therefore stands to reap a very healthy annualized return at a price above its initial offer price.

If, by chance, a competing bid emerges and pushes MEG's share price higher, SCR would make a sizeable gain irrespective of its success or failure in acquiring MEG.

MEG’s Assets Would Upgrade SCR's Asset Quality

If SCR were to succeed in acquiring MEG, it would emerge with a higher-quality asset portfolio. MEG’s Christina Lake SAGD asset features greater well productivity than SCR’s assets. The asset’s advantageous geology and contiguous footprint have lower operating and capital costs, so it breaks even at a lower price and requires less capital per barrel of oil produced to maintain production.

I estimate that MEG’s breakeven cost per barrel necessary for sustaining flat production is approximately US$45 per barrel WTI. By contrast, SCR's heavy oil assets break even in the low-US$50s per barrel WTI.

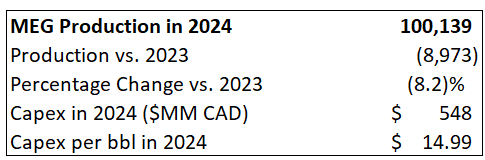

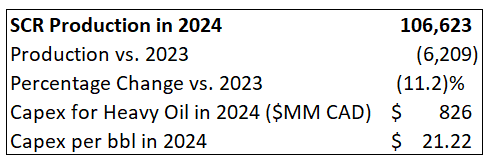

MEG’s superior geological and operating characteristics allow it to produce significantly more oil for every dollar of capital invested in production. Consider, for instance, that MEG spent $14.99 of capex per barrel to generate its 100,139 bbl/d in 2024, while SCR spent $21.22 per barrel to produce its 106,623 bbl/d.

Even at MEG’s lower rate of capex per barrel, its production declined less on an annual basis in 2024 than SCR’s. Despite the year-over-year declines, both companies intend to grow their heavy oil production over the coming years.

During SCR’s conference call announcing the deal this morning, Adam Waterous referred to MEG as SCR’s “doppelganger” and its “identical twin.” With all due respect to Waterous’s expertise, I take issue with his statement. The facts make it clear that MEG’s Christina Lake SAGD asset is higher-quality than SCR’s oil sands assets.

Throughout 2025, SCR and MEG shares have traded at roughly similar multiples of 2P net asset value and EV/DACF. After SCR’s recent asset sale, it trades at a discount to MEG because the smaller net debt component of SCR’s enterprise value after its asset sale reduces its EV-based trading multiples, such as EV/DACF and EV/Boepd.

However, I’d argue that MEG deserves to trade at a premium multiple relative to SCR due to its:

Longer track record of consistently successful operating results.

Simpler operations.

Higher overall asset quality and superior capital efficiency.

Certainty of production growth prospects.

Higher return on capital employed

More liquid stock.

Less risk of making strategic mistakes.

More conservative balance sheet.

Consequently, attempts to justify SCR’s acquisition proposal by claiming it’s paying up for MEG should fall on deaf ears.

Other Potential Suitors for MEG

Of the other suitors likely to emerge, I suspect Canadian Natural Resources (CNQ) and Suncor Energy (SU)—also a holding of our HFIR Energy Income Portfolio—would be the most likely to make a bid.

The first thing that CNQ has going for it is its massive scale. Its enterprise value stands at $108 billion, so it will have no problem making a bid for MEG, with its $7 billion enterprise value. And since CNQ’s shares trade at a significant premium to MEG’s, it can afford to offer stock as consideration in a deal. CNQ's premium makes a MEG acquisition more accretive to it than it would be to other suitors with shares trading at lower multiples.

MEG could also be an attractive addition to CNQ’s extremely high-quality asset base.

Offsetting the possibility of CNQ making an offer for MEG are two considerations. First, CNQ’s assets are generally of higher quality than MEG’s. CNQ’s oil sands assets have lower operating costs and cash flow breakeven costs per barrel. As a result, an acquisition of MEG could negatively impact CNQ's heavy oil operating and financial metrics.

But perhaps even more importantly, throughout CNQ's long history, it has avoided engaging in bidding wars. I don’t expect it to start now. Rather, CNQ is more likely to remain culturally and strategically averse to making a competing bid in a hostile takeover of MEG.

SU may be interested in MEG due to its need to address the depletion of its Base Mine, which accounts for a considerable part of its upstream production. The Base Mine has a remaining life of approximately ten years, and MEG’s multi-decade reserve life would be an attractive fit for SU. The Base Mine produces roughly 250,000 bbl/d for SU. MEG’s 105,000 bbl/d of production can be increased significantly before the Base Mine reaches depletion.

At What Price is a MEG Acquisition No Longer Accretive?

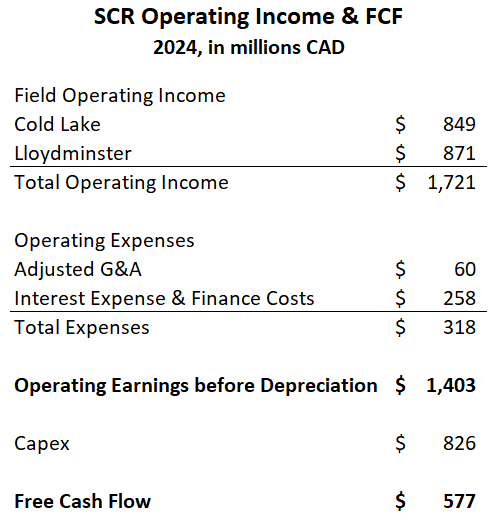

I estimate free cash flow using metrics that are as close to comparable as possible. I use SCR's 2024 field operating income figures in its heavy oil segment disclosures of its annual report to determine free cash flow. MEG's free cash flow is calculated from its income and cash flow statements.

SCR’s oil sands assets generate approximately $577 million in free cash flow in 2024, as detailed below.

Based on SCR’s current stock price of $30.30, its 214.2 million diluted share count, and its $59 million of net debt, its enterprise value is $6.55 billion.

In 2024, WTI averaged US$75.72 per barrel. At that price, SCR generates an approximately 8.8% free cash flow yield on its current enterprise value.

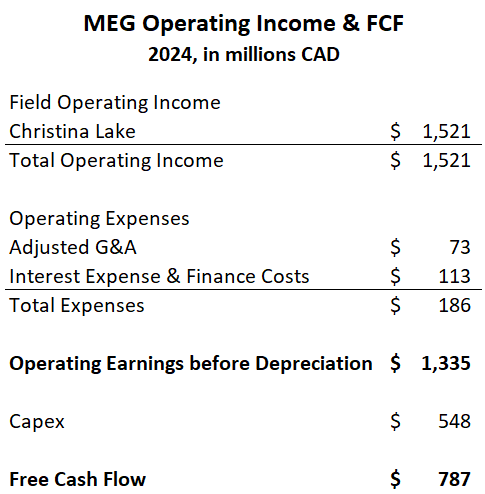

In 2024, MEG generated $787 million in cash flow, as shown in the table below.

For MEG, based on SCR’s offer price of $23.27 per share, the company’s 263 million diluted shares outstanding, and its $769 million in net debt, its enterprise value stands at $6.89 billion.

Based on EV/FCF multiples, SCR can offer as much as $31.04 per MEG share before the deal is no longer accretive on a FCF basis. However, I don’t expect MEG’s shareholders and directors to agree to a bid even at that relatively elevated level, as it undervalues MEG relative to the company's long-term prospects.

Conclusion

In the end, SCR’s bid for MEG is likely to fail. MEG won’t willingly accept an offer that significantly undervalues its shares. Furthermore, hostile takeovers are rare in Canada. Other potential acquirers may be unwilling to participate in this one. All these factors stack the odds squarely against SCR’s bid—or even a sweetened bid—succeeding.

I’m holding onto my MEG shares. Investors with a purchase price below SCR’s offer price should consider doing the same, as they’re likely to do very well over the long term by simply staying put.

Analyst's Disclosure: I/we have a beneficial long position in the shares of MEG:CA, SCR:CA, SU:CA, ARX:CA either through stock ownership, options, or other derivatives.

I think your cash flow yield numbers use FCFE/EV. Doesn't it make more sense to use FCFF/EV or else FCFE/Market Cap?