Editor’s Note: This article was first published to paying subscribers on June 11, 2025. Please note that the market data reflects the time of the publication (not updated).

We wrote an update on Whitecap here following the Q2 results.

By: Jon Costello

Note: Dollar references in this article are to Canadian dollars unless otherwise specified.

Whitecap Resources (WCP:CA) has emerged from its acquisition of Veren as a premier large-cap North American E&P.

An overview of the combined entity is shown below.

Source: Whitecap Resources May 2025 Investor Presentation, May 28, 2025.

The combined entity features a current production capacity of 365,000 boe/d, with production comprised of 54% light crude oil, 11% NGLs, and 35% natural gas. The greater scale and operating synergies brought forth by the combination will enhance the combined entity’s drilling economics and capital efficiencies.

After the combination, Whitecap’s acreage possesses a deeper core liquids drilling inventory than any Canadian E&P peer outside of the oil sands, with considerably more than 20 years of high-quality inventory. The depth of Whitecap’s inventory exceeds that of every independent public Permian E&P. Only Diamondback (FANG) comes close to matching Whitecap’s inventory depth.

Whitecap intends to grow its production by 3% to 5% per year, with production growth driven by legacy Veren’s liquid-rich Montney acreage. I expect its production to increase to more than 450,000 boe/d over the next five years, at which point it will still have decades of high-quality drilling inventory.

Whitecap has consistently built value for its shareholders, and I expect that to continue. Its management’s long-term track record of value creation is among the best among Canadian energy companies.

The chart below presents some important value metrics. Management’s record is particularly impressive considering how difficult macro oil and natural gas market conditions have been throughout long stretches of time during this period.

Source: Whitecap Resources May 2025 Investor Presentation, May 28, 2025.

The combined entity’s stock will be more desirable to large equity investors interested in a multi-year holding period than either Whitecap or Veren were on a standalone basis. The standalone entities had been stuck in the no-man’s land of Canadian E&P mid-caps in recent years. They traded at a perpetual discount to larger North American peers, irrespective of their underlying economics or growth prospects. I expect that to change with the combined entity as larger investors appreciate the wider implications of the end of U.S. shale growth and seek a reliable means of oil exposure.

The discount on Whitecap shares provides an attractive entry point for long-term investors. As the company’s strengths are borne out over the coming quarters in its operating and financial results, I expect investors to embrace the combined entity and bid its shares to a sustained higher multiple.

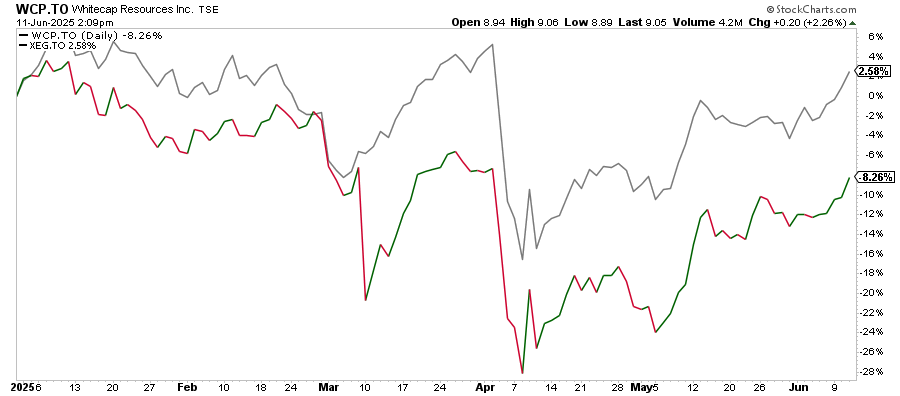

Whitecap Shares Have Underperformed, Creating Opportunity

Despite Whitecap’s positive attributes, its stock has underperformed Canadian large caps in recent months. The chart below plots their year-to-date performance against the Canadian E&P exchange-traded fund XEG (XEG:CA).

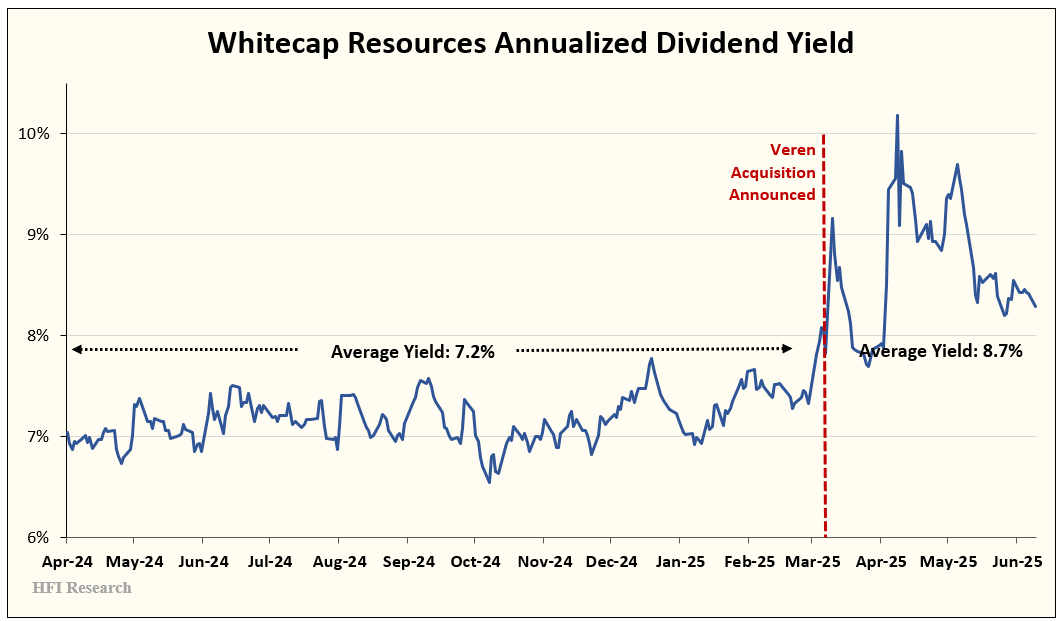

The low price of Whitecap shares translates into a higher dividend yield than they’ve maintained throughout the company’s recent history.

The higher yield partly reflects the likelihood of a dividend cut, though I view a cut as unlikely in 2025 and beyond if WTI averages above US$60 per barrel.

A return to Whitecap’s average dividend yield in the year before its Veren acquisition implies a stock price above $10.00, 12% above the current stock price of $8.90.

Whitecap shares remain depressed versus peers for several reasons. For one, investors face uncertainty because the company has yet to release a quarter of results as a combined entity. Larger investors, in particular, seek confirmation that management can execute at a larger scale. The shares are also dogged by lingering bearish sentiment carried over from before the combination.

Legacy Whitecap-Veren Assets Offset One Another’s Weakness

Today’s Whitecap retains the strengths of standalone Whitecap and Veren while simultaneously diminishing their respective weaknesses as standalone operators. Consider the following:

Whitecap’s reserves were relatively gas-weighted, while Veren’s were more heavily weighted toward higher-value liquids. The combined entity’s production mix enhances its flexibility in navigating the ever-changing commodity landscape.

Veren’s more variable geology caused its well results to be less consistent than those of Whitecap. By the same token, Whitecap’s consistent execution was largely attributable to the more uniform nature of its geology. Operating results for the combined entity are likely to be more consistent over time. It can also be more selective about where it chooses to drill, minimizing the risk that a few sub-par wells materially hurt companywide results.

Whitecap’s lower-decline asset base offsets Veren’s higher-decline assets. Whitecap’s liquids-rich natural gas wells reduce its AECO breakeven to less than $1.00 per MMBtu, while Veren’s deep crude oil inventory enhances the combined entity’s cash flow torque to crude oil prices.

Whitecap’s natural gas marketing operations were a point of weakness before the combination. Veren was stronger on the marketing front. The addition of Veren’s marketing practices, combined with the company’s vast scale, can help enhance price realizations for the combined entity. For instance, its larger scale and deeper drilling inventory open the door to long-term LNG feedstock supply deals and the higher price realizations they bring.

The combined entity is properly capitalized for its size. Whitecap’s $270 million disposition of Saskatchewan assets shortly before the acquisition closed reduced the combined entity’s net long-term debt ratio to approximately 0.8 times debt-adjusted cash flow (DACF) at US$70 per barrel WTI, assuming $2.00 per MMBtu AECO natural gas prices. The figure stands at a reasonable 0.9-times debt-adjusted cash flow at US$65 per barrel WTI. Leverage is greater than legacy Whitecap—where net debt to DACF was less than 0.5-times at US$70 per barrel WTI—but lower than legacy Veren—where net debt to DACF was above 1-time at US$70 WTI. Today, the combined entity’s leverage ratio is roughly in the middle of the range of public independent North American E&Ps.

Despite Assertions by Critics, Asset Quality is High

With the combination now complete, legacy Veren’s critics who claim that the company had poor asset quality have carried their concerns over to Whitecap. Veren’s drilling results have already invalidated these concerns, but that hasn’t quelled the bears’ critiques.

The main thrust of the bearish argument holds that disappointing results on 12 wells Veren drilled in its Gold Creek acreage in late 2024 were indicative of poor geology in acreage the company viewed as core.

In reality, the poor well results were caused by an experiment by management gone awry. Specifically, management employed a “plug-’n-perf” completion technique in response to higher recoveries achieved in previous wells that used plug-’n-perf completions. For the 12 wells in the experiment, plug-’n-perf completions represented a move away from the company’s more reliable single-point entry completion technique.

After the experiment failed and well results disappointed, management vowed to return to single-point entry completions in its third-quarter 2024 earnings conference call on October 31. Management expected the new completion technique to rectify the experimental Gold Creek well results. The market didn’t buy it. Veren shares crashed, and management was penalized with a negative stigma in the market.

The price crash set up an outstanding buying opportunity. I bought the shares for the HFI Research Energy Income portfolio at a price equivalent to $6.72 per Whitecap share. I plan to hold the Whitecap shares for several years.

At the time of management’s mishap, criticisms by Veren bears ignored evidence that the company’s well results supported management’s claims that completion techniques—and not geology—were the cause of the poor results. Gold Creek wells in close proximity to the wells with botched completions had already delivered outstanding results. Subsequent well results have strengthened the claim that completion techniques caused the mishap in the impacted area. Moreover, in the months after the poor well results and before its merger with Whitecap, Veren applied for new permits in the same area.

Despite all the available evidence that Veren’s geology was intact, as well as the fact that Veren went on to drill some of the most productive oil and liquids-producing wells in the Western Canadian Sedimentary Basin in January 2025, the bears continue to view Whitecap’s acreage as subpar.

As long as questions remain about the company’s acreage—whether valid or not—they could weigh on the share price.

To the extent the bearish concerns depress Whitecap’s share price, I believe they also represent a source of opportunity. I’ve been a buyer of the shares during their selloff in recent months.

However, as positive well results continue to come in, the market will regain confidence in the combined entity’s management and asset quality. At that point, I believe improving sentiment will deliver a tailwind to Whitecap shares that causes them to outperform.

Dividend is Sustainable Below US$50 per barrel WTI

Aside from Whitecap’s asset quality, the other contested matter among Canadian E&P investors is the sustainability of its dividend. This is another area where I believe bears are wide of the mark.

Desjardins Securities analyst Chris MacColloch—a top Canadian E&P analyst whom I respect—recently stated in an interview that a dividend cut was “a painful but necessary step” for Whitecap. The cut would be necessary because strip prices on June 4 implied that Whitecap’s dividend payout ratio would be 110% in 2026. The backwardation in the curve at the time implies an average full-year 2026 WTI price in the low-US$60s per barrel.

Whitecap shareholders should acknowledge that a dividend cut is a risk amid low oil prices. However, I believe the company is likely to sustain its current dividend unless WTI falls into the US$50s per barrel for a period of several months.

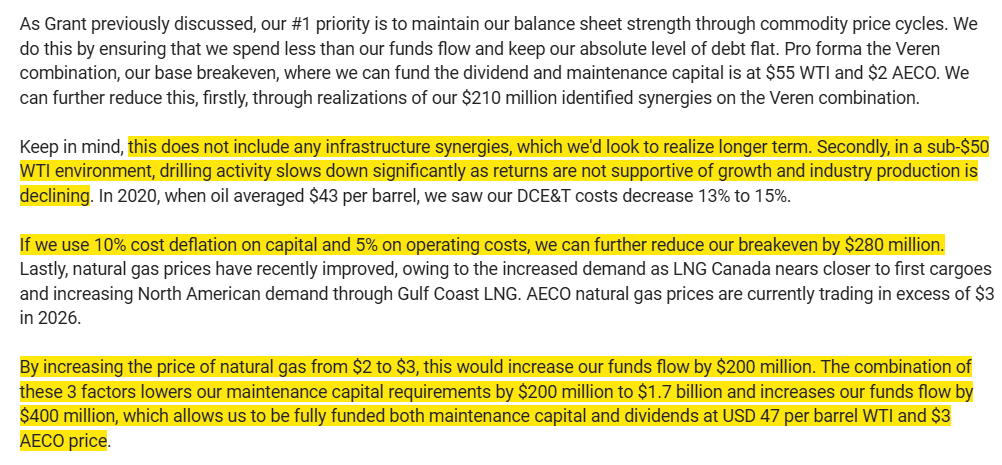

For one, management appears committed to maintaining the current dividend. The excerpt below is taken from Whitecap’s first-quarter earnings conference call on April 24, in which CFO Thanh Kang added the following to CEO Grant Fagerheim’s earlier commentary about factors likely to bolster the company’s cash flow and dividend sustainability if oil prices decline.

Source: Whitecap Resources Q1 Earnings Conference Call BamSEC transcript, April 24, 2025. Highlight added by author.

Second, MacColloch states that he assumes Whitecap’s 2026 capex will be $2.4 billion, consistent with management’s guidance. However, Whitecap plans to grow in the 3% to 5% range, so a portion of management’s 2026 capex guidance is aimed at production growth. Management can likely ratchet back capex to reduce the company’s cash flow breakeven price per barrel and support its dividend.

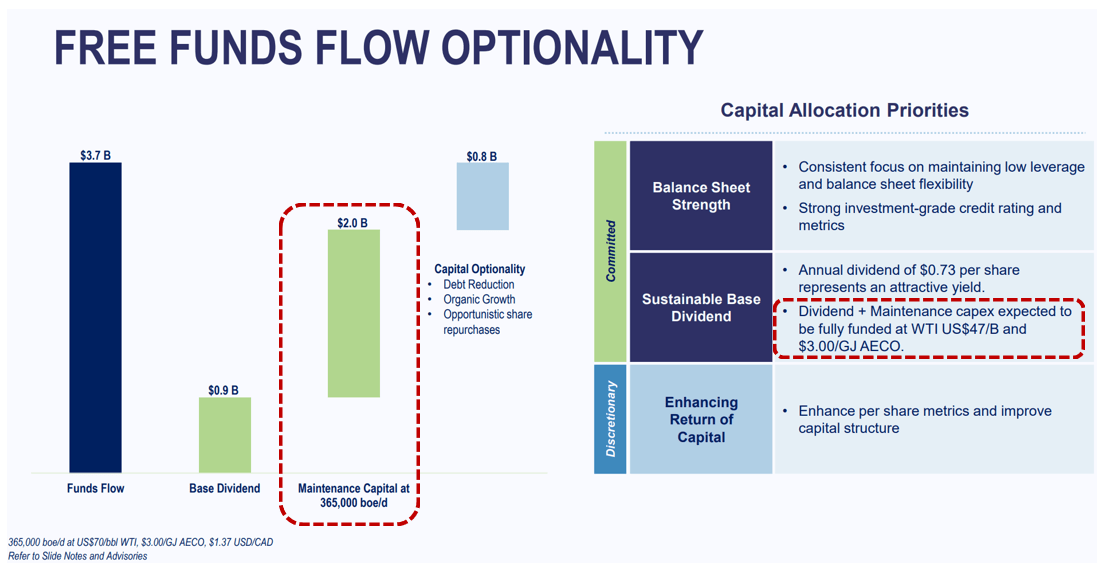

In its May Investor Presentation, Whitecap stated that its annual maintenance capex is $2 billion, as shown below in the red-dotted circle on the left. It also states that the dividend is sustainable down to US$47 per barrel WTI, shown on the right.

Source: Whitecap Resources May 2025 Investor Presentation, May 28, 2025. Red-dotted line added by author.

My modeling indicates that at $2.0 billion of capex, exclusive of hedges, Whitecap can fund its dividend down to US$56 per barrel WTI, assuming $3.00 per MMBtu AECO. Whitecap has hedged 31% of its production using swaps at a weighted average price of US$72 per barrel WTI. It has also hedged 9% of its production using collars with a floor of $68. Inclusive of 2025 hedges, I estimate the dividend can be covered down to US$49 per barrel WTI, which is in the ballpark of management’s estimate. Given that operating cost reductions would likely materialize at lower oil prices, management’s estimate of US$47 per barrel is indeed realistic.

The situation changes in 2026. Low oil prices and a backwardated futures curve have prevented Whitecap from hedging production for 2026. Consequently, next year, the dividend could be at risk if WTI is sustained in the mid-US$50s per barrel. Below those prices, Whitecap would likely join almost all of its peers, who also would slash their dividends in response to such low oil prices.

Even if WTI did fall to US$55 per barrel, it would probably not remain there for long. Such a low oil price would force dramatic cuts in U.S. shale production, which would put upward pressure on prices by reducing supply and may also induce action out of OPEC to stave off potential future supply issues.

This exercise simply shows that Whitecap’s dividend, while not bulletproof in every commodity environment, is sustainable down to very low levels. Its 8.2% yield therefore remains attractive among large-cap Canadian E&P stocks.

Valuation

Whitecap shares offer a very high probability of attractive returns over a holding period of three or more years.

I estimate that Whitecap’s current stock market valuation assumes US$65 per barrel WTI and $3.00 AECO. To the extent an investor believes long-term oil prices will exceed those levels, Whitecap shares offer an attractive alternative.

The company’s historical multiple of enterprise value to debt-adjusted cash flow (EV/DACF) is 3.9-times. I estimate the company generates approximately $3.6 billion of DACF flow at US$65 per barrel WTI. Whitecap’s net long-term debt is $3.45 billion, and its market cap is $11 billion, for an EV of $14.45 billion. This puts its EV/DACF around its historical average.

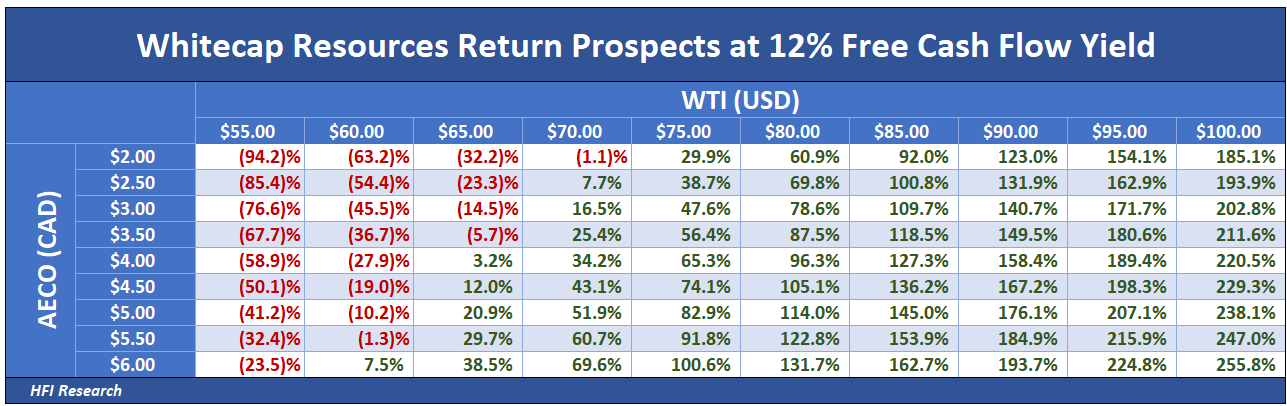

One of the chief attractions of Whitecap’s stock is its cash flow torque to commodity prices. The chart below captures the significant upside amid higher prices, assuming capex of $2.5 billion and that the shares trade at a 12% free cash flow yield.

The risks of permanent loss from the current stock price over a period of years is low. If commodity prices disappoint, Whitecap’s ample cash flow generation and conservative leverage profile ensure that it will survive any reasonable commodity price environment.

Risks

While Whitecap’s longer-term returns are clearly attractive from current levels, the shorter-term outlook presents a potential challenge.

For example, the current oil market consensus calls for large inventory builds beginning in late 2025 and persisting through 2026. If these builds approach the magnitude of current expectations, they’re likely to hold oil prices below US$70 per barrel. As long as significant inventory builds remain a clear risk, as they do today, long-term E&P investors should be prepared to endure a period of low prices and invest accordingly.

Despite the risk, I believe Whitecap’s dividend is sustainable below US$60 per barrel, so it remains an attractive investment candidate. Importantly, I believe a period of sub-US$70 per barrel WTI will give way to significantly higher prices over the subsequent years.

No one knows the extent of inventory builds or whether sub-US$70 per barrel prices will be sustained through 2026. I’m confident, however, that such low prices would stimulate demand and bring about lower U.S. production. If the downward trend in the international oil rig count amid recent oil prices is any indication, production outside the U.S. would also be at risk of declining. This then begs the question of whether OPEC+ would intervene with price cuts to forestall longer-term supply constraints and impairments. All these factors make sustained sub-US$70 per barrel WTI unlikely, barring a global recession, in my view.

In Whitecap’s case, the consensus natural gas outlook provides a counterpoint to the bearish oil consensus. If Henry Hub gas prices are sustained above US$4.00 per mcf, AECO natural gas prices will be more supportive of Whitecap’s cash flow and dividend sustainability than my modeling indicates.

Conclusion

Whitecap shares are one of the most attractive Canadian E&Ps at their current price. Their low risk of permanent loss, substantial upside potential, and large dividend yield provide an attractive risk/reward profile for any long-term investor.

Investors can take solace in the fact that management remains a large buyer of shares. CEO Grant Fagerheim owns 3.17 million shares and regularly buys in the open market. Management’s alignment with shareholders is a refreshing departure from legacy Veren’s management.

Like any E&P, its stock price will be sensitive to commodity prices. I believe it’s likely to make a large move higher once WTI rises out of the mid-US$60s per barrel range, where concerns about a dividend cut—whether valid or not—become less of an issue. At higher prices, dividend increases will deliver still greater value to shareholders.

Whitecap’s stock will become a favored destination for investors as shale production continues to mature and eventually decline. Investors should buy now before the investing herd heads north of the border.

Analyst’s Disclosure: Jon Costello has a beneficial long position in the shares of WCP:CA either through stock ownership, options, or other derivatives.