(Public) What The HFI Research 2025 Oil Market Supply/Demand Balances Mean For Investors

By: Jon Costello

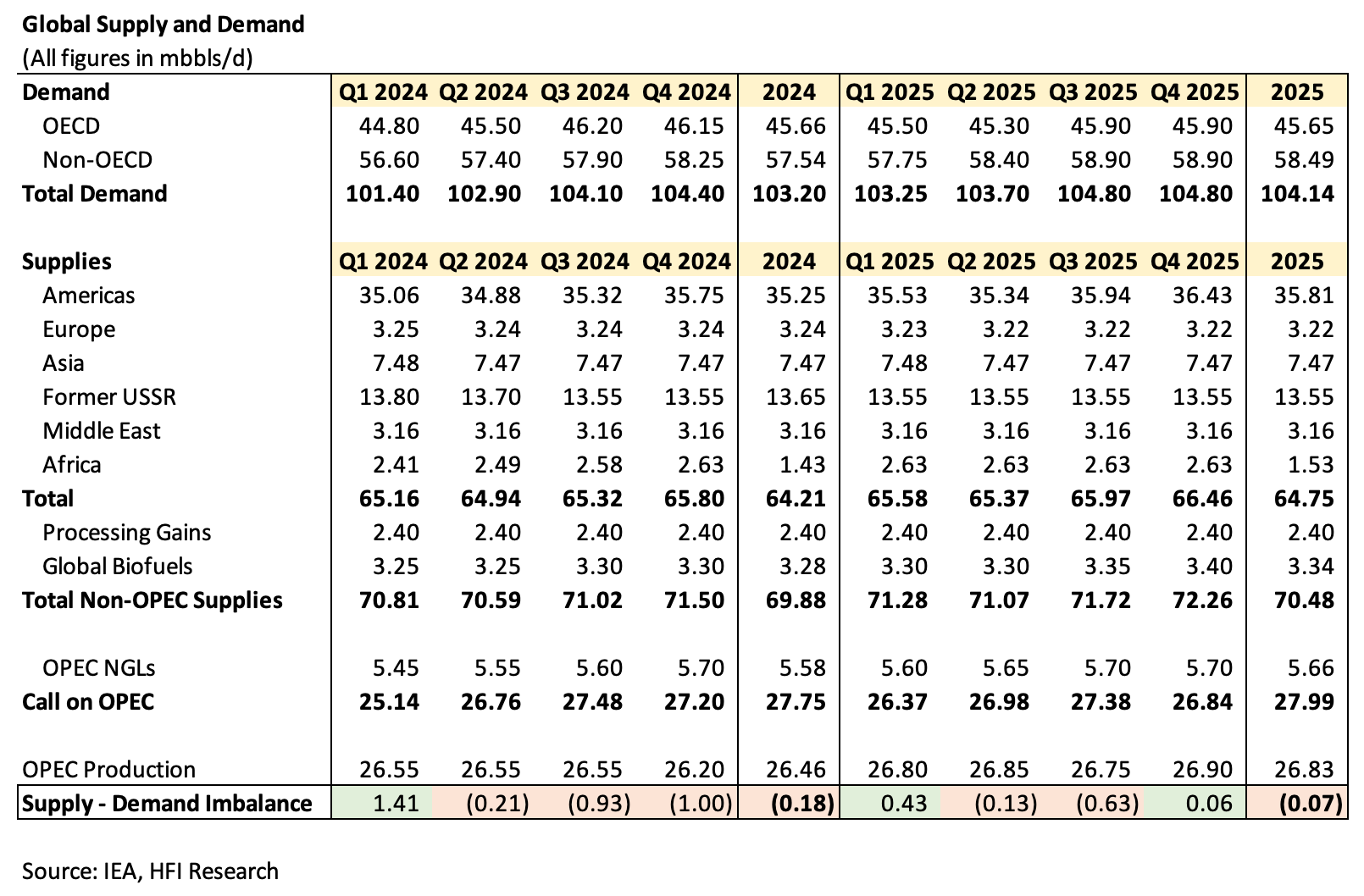

Yesterday, Wilson published his first look at 2025 oil market supply/demand balances. His forecast is reproduced below.

The balances call for a 70,000 bbl/d draw in 2025, or 25.6 million barrels below year-end 2024.

What Conclusions Can Investors Draw from These S/D Balances?

The following conclusions can be drawn from the forecast:

Supply and demand in 2025 are essentially balanced. There’s a wide margin of error required to properly interpret them due to the unknowns and inevitable unexpected events. The 70,000 bbl/d called for in the forecast falls well within that margin of error. Lower prices increase the chances of production stalling; higher prices will boost production. Overall, however, this forecast is neither bullish nor bearish given that global oil inventories at the moment are not bloated.

The first quarter will be the most bearish for fundamentals. One year ago, there was a similar setup for 2024, with investors expecting builds throughout the year that were most severe in the first quarter. The late-2023 and early-2024 selloff turned out to be an attractive buying opportunity, as prices inflected higher once the fundamental outlook improved. In 2025, the outlook will be determined by whether a recession reduces demand, as well as by the extent to which supply underperforms. E&Ps around the world are devising their 2025 capex budgets amid today’s bearish pricing outlook, so we don’t expect any major producing country or company to outperform significantly. As for potential supply underperformance, we’re looking at Canada, the U.S., and Brazil. Notice that these regions as a group—all included in the “Americas” line of the chart above—are expected to drive 2025 production growth. Material supply disappointments by this group amid flat or healthy demand can create a larger-than-expected supply deficit and send oil prices significantly higher.

In the event inventories stay flat in 2025, prices are likely to zig-zag above and below $80 per barrel, as they did in 2024. This will set up ideal conditions for trading E&Ps. As we saw in 2024, when inventories alternate between builds and draws starting from today’s levels, we’re likely to see WTI trade between $70 and $90. Weakness below $75 should be bought; strength above $85 should be sold.

The setup for 2026 looks favorable under the HFIR 2025 balances, though what happens in 2026 will ultimately depend on how supply performs over the next few quarters. If supply underperforms, as I suspect it will if WTI averages $75 or below, the setup for 2026 will be strong assuming demand grows at roughly 1 million bbl/d per year. If prices remain low and supply underperforms in 2025, we recommend that long-term investors increase their weighting to E&Ps over the course of the year to benefit from the next era of the oil market, in which U.S. shale production isn't capable of driving meaningful supply growth.

Among some other observations, HFIR balances are more bullish than consensus. Bearish consensus projections are a leading cause of today's pitiful sentiment among energy investors.

Consider that the major private consultancies are calling for large builds. Energy Aspects, for instance, expects inventories to build by 800,000 bbl/d on average in 2025. However, their balances assume OPEC+ brings back production as scheduled. I don't believe this is likely when oil prices are low because it would create a contango that would allow U.S. shale E&Ps to hedge, and it would result in a massive inventory surplus that would have to be down over time. Both of these outcomes represent headaches for OPEC+ that the group wants to avoid.

Meanwhile, investment bank commodity analysts are now toeing the line close to strip pricing in their oil price forecasts, at least for next year. They do so even though strip pricing is useless as a forecasting tool. Strip pricing for WTI is averaging $66 per barrel over the next few years, which is unsustainably low considering that U.S. shale production is likely to decline with WTI at that level for a few quarters.

Against this backdrop, the neutral HFIR balances for 2025 imply that today's consensus supply/demand expectations, investor sentiment, and oil prices are too bearish.

What HFIR Balances Mean for Energy Stocks in 2025

Energy investors will have plenty of opportunities to trade and invest in the energy sector if the HFIR forecast comes to pass.

Avoid shale E&Ps. Next year will represent another year of inventory depletion. Underperformance by independent shale E&Ps will create headwinds for production growth in 2026 and beyond. The only U.S. shale E&Ps we’d be comfortable holding are Occidental Petroleum (OXY) and Diamondback Energy (FANG). Both could capitalize on the situation through bolt-on acquisitions.

The balances are bullish natural gas. Less oil production will have the effect of decreasing the volumes of gas produced as a byproduct of oil production. This lower supply, coupled with higher demand from LNG facilities entering service, will create a bullish tailwind for natural gas prices. Antero Resources (AR), the new Expand Energy (EXE)—formerly Chesapeake Energy—in the U.S. and Tourmaline Oil (TOU:CA), ARC Resources (ARC:CA), Peyto Exploration (PEY:CA), and Spartan Delta (SDE:CA) in Canada are poised to benefit from higher natural gas prices.

They imply today's sentiment is too bearish. Even with bearish consensus balances for 2025, today’s extremely bearish sentiment is not justified for those with anything but a very short-term view. We’re in oil to play a long game. We expect supply constraints driven by the end of U.S. shale growth and years of underinvestment outside of shale to put upward pressure on prices. Those with a three-to-five-year time horizon for their investments will find a period of weakness to be bountiful for identifying high-quality investment candidates.

On the oil side, we continue to favor MEG Energy (MEG:CA), Athabasca Oil (ATH:CA), Cenovus Energy (CVE:CA), Suncor Energy (SU:CA), Strathcona Resources (SCR:CA), and Veren (VRN:CA).

The balances create a trader's market. Speculative traders looking to play the $70-to-$90 range that I expect for WTI in 2025 should opt for higher-beta names for maximum profits, though they’ll have to be comfortable suffering through inevitable downdrafts. We prefer Veren (VRN:CA), Tamarack Valley Energy (TVE:CA). Both have debt but also have enough inventory to make it through 2025 unscathed. I’d avoid Baytex Energy (BTE:CA) due to their more limited reserve life, though I’ll reassess BTE if its reserve report contains positive changes.

Income investors should stay the course. Income investors should stick to the names I own in the HFIR Energy Income Portfolio. I added to Genesis Energy (GEL) yesterday at $12.90. Enterprise Products Partners (EPD), Energy Transfer (ET), and TC Energy (TRP) are also good alternatives, as is MPLX (MPLX), which just announced a 12.5% increase in its quarterly distribution beginning in the fourth quarter.

I expect South Bow (SOBO) to be acquired over the next year or two, so it may be worth holding due to that outcome. The Canadian listing yields 7.3%, so investors will be well paid to wait. Western Midstream (WES) also appears to be setting itself up for a sale, given yesterday’s appointment of a CEO with an investment banking background steeped in M&A. It yields a healthy 9.2% and is another good choice for income investors who are comfortable with MLPs. I expect its unit price to be supported by expectations for a sale, and I expect it to sell at a premium to its current price.

Conclusion

Investors should try to keep their emotions out of the picture and focus on opportunities. I prefer the setup in which a portfolio of growing income-producing midstream names funds purchases of E&Ps during times of weak crude pricing. All my trading will be done with a view to the longer term, with a bias toward high-quality names. In today’s overpriced equity market, I believe it’s the most sensible course in what is surely the most hated sector.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of the HFI Research Energy Income Portfolio, SDE:CA, VRN:CA either through stock ownership, options, or other derivatives.