By: Jon Costello

There is no shortage of refiner bulls right now, and I am sympathetic to them because I’ve been in that camp myself. In April 2024, I recommended buying Valero (VLO) “for the long term.” The stock has climbed from roughly $162 to around $266, a gain of about 64%.

The bullishness is justified from a macro perspective. Fundamentals for the industry are stronger than ever. Refining margins are at historic highs, U.S. gasoline inventories sit about 5% below the five-year average and distillate about 10% below, refineries are running flat out near 96% utilization, and my own forecast keeps refining margins supported for the next couple of years as global runs recover from this spring’s disruption and clean-product stocks take until the back half of the decade to rebuild.

So I’m not bearish on refining margins or, in a broader sense, today’s refiner sector fundamentals. Rather, I believe there are factors at play that are more consequential for long-term holders at current stock prices.

Today’s Macro Bull Case for Refiners Is Strong

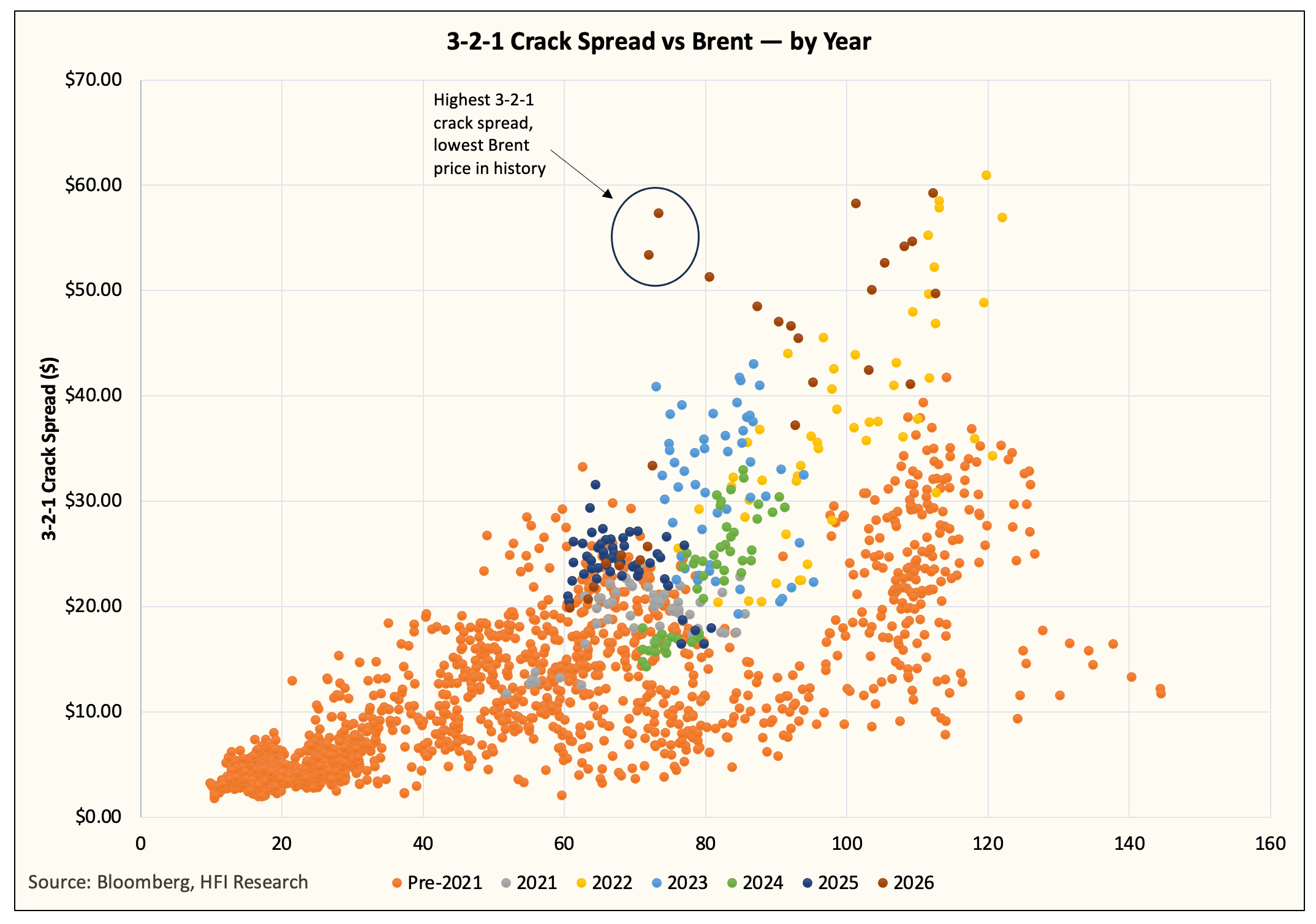

The strongest version of the bullish refiners thesis states that refining capacity has been rationalized across the West, the survivors are complex and well run, and product inventories are genuinely tight. Margins have remained elevated since 2022 and stand at their highest point relative to Brent prices in history, as shown in the following chart.

In point of fact, if margins remain at today’s levels, Valero will generate enormous cash flow, and so will Marathon Petroleum (MPC) and Phillips 66 (PSX). The problem is, first, I believe today’s high refining margins are likely to revert to lower levels, and second, refining economics at lower margins translate into lousy long-term investment returns.

Refiners Don’t Control the Variable That Matters Most

Refining is a spread business. A refiner buys crude at a price fully out of its control, sells a product at a price also out of its control, and keeps the difference, which is known as the “crack spread.” That spread forms the basis of a refiner’s fundamental performance.

The problem for the industry’s equity investors is that performance is determined by forces that are impossible to forecast, making valuation a complicated undertaking.

To properly value a refiner, an investor has to discount the crack spread to a realistic price and arrive at a stock price suitable for holding through the industry’s cycle. It helps to have a view on the direction of margins, but I’ve found this exercise to offer little value outside of one or two quarters into the future—and even that is extremely difficult.

Complicating the picture further is the marginal barrel of refined product supply. China has built itself into the world’s largest refiner, adding 5.5 million barrels per day of capacity between 2011 and 2023. It now runs a structural surplus managed through government export quotas.

When Beijing increases those quotas, its refined products flood the seaborne market, driving global crack spreads lower. When it tightens them, the dynamic is reversed.

In other words, a U.S. refiner’s margin swings on policy decisions made in Beijing under the country’s five-year plan, as well as potentially in an ad hoc manner in response to market conditions. Layer on a global capacity wave still under construction and a Chinese gasoline market possibly approaching its peak as electric vehicles take market share, and the single most important variable in the business is one its investors and managers cannot influence at all.

Operating Leverage is Extraordinary, But Cuts Both Ways

Another complicating factor in valuing refiners and owning refining stocks is the operating leverage these businesses face. This is no secret, as the refiners disclose it themselves.

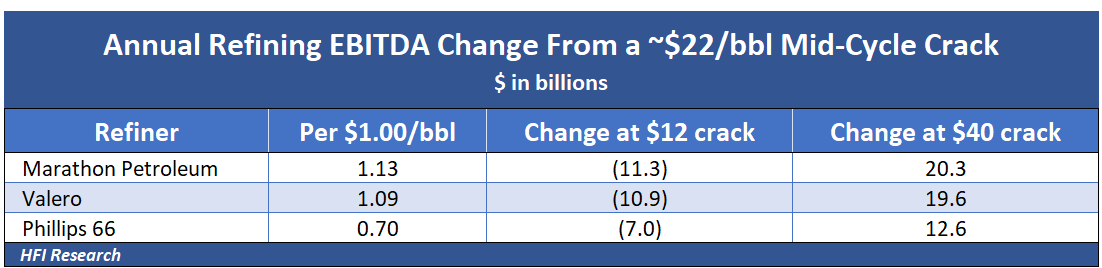

Marathon’s investor presentation states that a one-dollar move in the blended crack spread changes its annual refining EBITDA (its operating earnings) by roughly $1.1 billion; Phillips 66 puts a one-dollar move in its refining indicators at about $700 million; and Valero’s throughput of nearly 3 million barrels per day implies the same order of magnitude.

The 3-2-1 crack—the standard benchmark for the margin on turning three barrels of crude into two of gasoline and one of distillate—has ranged from the low teens to well above $40 a barrel in just the past few years.

And the volatility in crack spreads can cause cash flow to swing wildly. A $10 move in the crack, comfortably inside that range, swings annual earnings by roughly $11 billion at Marathon, $11 billion at Valero, and $7 billion at Phillips 66. This all-important variable is therefore not a reliable input for valuation. It’s ultimately more of a guess about a quota number set in Beijing and the world’s oil chokepoints, and the companies are telling you so in their own presentations. A proper valuation has become too difficult for me to render on a reliable basis, and, frankly, I’m wary of anyone who claims they can do so.

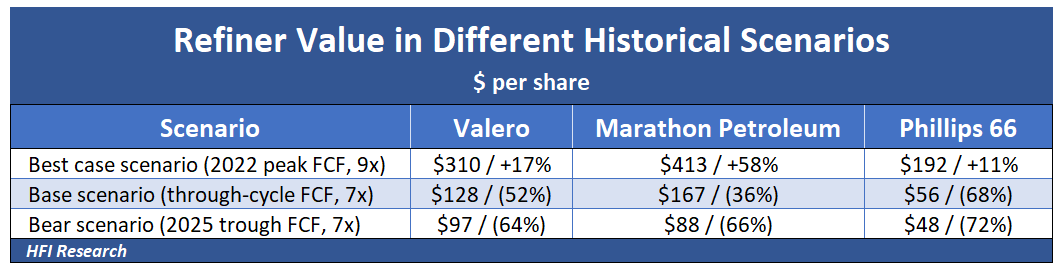

Put that torque in per-share terms, and the value trap to which current refining investors are exposed comes into focus. At the 2022 peak—the best year these businesses ever posted —Valero threw off about $34 of free cash flow per share, Marathon roughly $46, and Phillips 66 about $21. Capitalize that peak at nine times, the peak multiple the market has paid for refiners for years, and the math puts Valero’s stock at $310, Marathon’s at $413, and Phillips 66’s at $192. That represents upside of 17%, 58%, and 11%, respectively, from today’s prices. And that is the reward for everything breaking right at once, including a peak crack spread, peak cash flow, and a peak multiple.

Now invert it. Using average free cash flow from 2023 to 2025 valued at a more sober seven times, Valero is worth about $128, Marathon $167, and Phillips 66 $56. That is 36% to 68% below where the three trade today.

The bear case, which assumes trough cash flow on the same multiple, gets worse still. Today’s price already covers the best year on record, and the base case sits one-third to two-thirds lower. Exhibit 2 sets the three scenarios side by side.

The asymmetry between these three scenarios is the whole case. At their current prices, these stocks offer limited upside and significant downside. Moreover, that downside may be prolonged unless refining margins remain elevated at historic highs.

Beware of “Cheap” Refiner Stocks

There is a second trap inside the cheap-looking refining names. The refiners that screen cheapest are usually the inland and heavy-crude players whose competitive advantage, when they were built decades ago, was a wide discount on Canadian and other heavy-crude barrels. This discount represents the difference at which heavy Canadian crude trades below the U.S. WTI benchmark, which those refiners pocket as extra margin.

That edge has narrowed structurally. Since the Trans Mountain expansion (a new pipeline that gave Canadian crude another route to market) opened in 2024, the Western Canadian Select discount has narrowed by roughly $3 per barrel, now averaging around $13, compared with historical levels north of $20. Cheap, in refining, usually means most exposed.

HF Sinclair (DINO) and Delek US Holdings (DK) are the poster children.

For HF Sinclair, each of its seven refineries has the complexity to convert discounted, heavy or sour crudes into high-value products. Three of these refineries are fed by pipelines carrying Canadian barrels, namely, its El Dorado, Parco, and Puget Sound refineries, the last of which is supplied directly from the Trans Mountain system. This fall, the company is completing a project at El Dorado that allows up to 10,000 more barrels per day of heavy crude to be added to the mix. That is new capital tied to a discount that has already narrowed.

Delek learned the same lesson a cycle earlier. It can deliver roughly 200,000 of its 302,000 barrels per day of crude straight from West Texas, and its Big Spring refinery is the closest plant in the country to Midland. When Permian production outran the pipelines in 2018, local barrels sold for as much as $18 per barrel below the U.S. benchmark, and refiners buying at Midland prices pocketed the difference. However, new pipelines to the Gulf Coast cut that discount. It went as low as $1 per barrel by late 2019, and the windfall refiners were able to capture went with it.

Cheap-looking refiners are cheap because the discounts that made them money keep shrinking. The market isn’t missing the value. It is pricing in the reduced value.

“Rationalization Made Them Quality” Misreads the Market’s Verdict

The strongest pushback against these bearish factors complicating refiner valuation is that consolidation has changed the business and that the survivors are durable, quality earners now, not the boom-and-bust refiners of the past. I will concede the first half. Margins may well stay elevated for the next few years.

But the risk for equity investors is that elevated margins represent the top of a cycle, not a permanent plateau. In fact, a supply response that ends every refining up-cycle is already building, as runs recover, the capacity wave lands, and products rebuild in the late 2020s.

More to the point, the market has already run the cyclical valuation experiment. Refiners earned a fortune from 2021 to 2025. However, they were never awarded a quality multiple for it.

In my 2024 work on Valero, its shares traded within a 5x-to-9x free-cash-flow band for years, around their long-run average, even as their returns on capital improved. The group as a whole has never been re-rated as a compounder, meaning the market has never agreed to pay a higher multiple for the same dollar of refining cash flow. The reason is visible in the returns themselves.

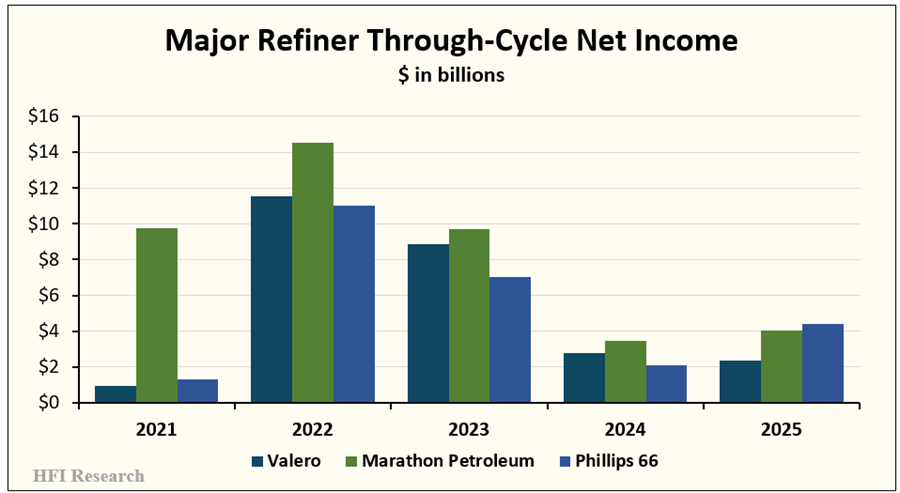

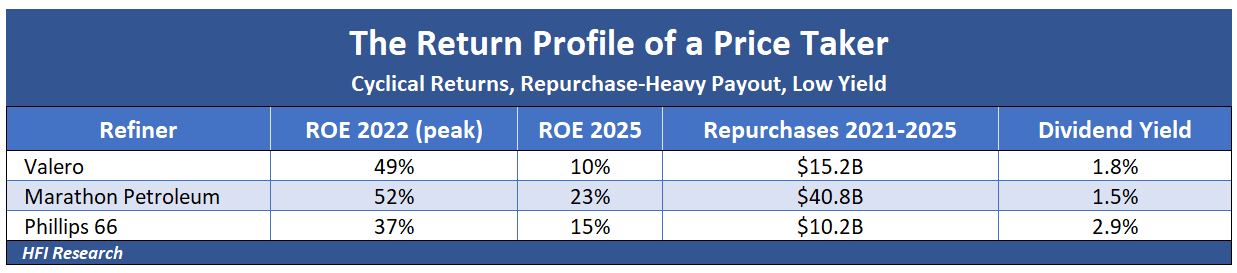

Start with the earnings, as shown in the following chart.

Valero’s net income ranged from under $1 billion in 2021 to $11.5 billion in 2022 and back to $2.3 billion in 2025. Return on equity, profit measured as a share of shareholder capital, told the same story.

A return on equity that swings from 5% to 49% and back is not a signal of a quality business. It is the signature of a price-taker. And the way the cash is distributed to shareholders compounds the issue for an income investor. These companies return capital overwhelmingly through repurchases. Valero spent $2.6 billion on repurchases versus $1.4 billion on dividends in 2025, and the group’s dividend yields now run from under 2% to about 3%, with Valero and Marathon both below 2%. That is a total-return trading vehicle, not an income holding.

None of this means you cannot make money trading refiners. In theory, you can buy them cheap based on through-cycle earnings and sell them at higher prices later in the cycle. But trading a cyclical stock and owning a business for long-term appreciation and/or income generation require different approaches, and my process here embraces the latter.

Own the Toll Road, Not the Refinery

If you believe in refined-products recovery, I believe there are better ways to play it than by owning the refiners directly. Instead, you can own the refined product toll road. Midstream operators that gather, process, and move crude and products earn fee-based, contracted cash flows that do not depend on the crack spread. The volumes move whether the refiner’s margin is fat or thin.

My preferred vehicle is MPLX, LP (MPLX), the logistics partnership built around Marathon. It is, in effect, the toll road bolted to a refiner, and it is the better business.

MPLX is particularly attractive for income investors. It yields roughly 7.6%, more than double the refiners’, on a distribution covered comfortably, it earns well more than it pays out, and its distribution is growing at a 12.5% annual clip, backed by volume commitments running into the 2030s. MPLX is not without risk. It relies on Marathon as both a sponsor and its largest customer, and it comes with the K-1 tax form that some investors would rather avoid. But its cash flow is contracted, and its payout is covered through a cycle, which is precisely what the refiners cannot say. I have owned and recommended it for years, and the contrast in its business quality with refiner customers is the crux of this article.

Integrated Refiners Hedge the Spread

There is another way to maintain exposure to refining, albeit indirectly. Own it inside an integrated oil company, where the refinery spread that can’t be reliably valued is hedged by the barrels the company pumps itself.

Cenovus Energy (CVE) and Suncor Energy (SU), each a holding in the HFIR Energy Income Portfolio, combine oil-sands production with refining and marketing, so the two halves of the cycle offset one another. When crude is cheap, refining margins widen. When crude prices rise, the upstream segment earns it back. Refining stops being the whole investment and becomes a balancing weight, the one thing a pure refiner can never be. Both are long-life, low-decline producers with oil-sands reserves measured in decades rather than the five to eight years of a typical shale driller, and both now return cash through growing dividends and repurchases.

I have recommended both for years. I called Suncor a buy for its yield and its torque to higher oil after management’s capital-allocation turnaround took hold, and I have backed Cenovus repeatedly on weakness as the oil-sands laggard whose results kept beating the tape. Neither is a pure crack-spread bet. You keep refining in the mix and still own cash flows you can actually model.

Calumet as a Special Situation

One name breaks every rule in this piece, and it is a core holding in the HFIR Energy Income portfolio. Calumet (CLMT) has a refining segment, but it is not a commodity refiner. Its value sits in Montana Renewables, a low-cost producer of renewable diesel and sustainable aviation fuel. The rest is specialty products — lubricants, solvents, and waxes — sold into niche markets where Calumet holds real pricing power. Its returns hinge on renewable-fuel economics, a federal loan guarantee, and clean-fuel policy, not on the spot 3-2-1 crack.

All these are higher-quality business factors than those of refiners. A contracted, idiosyncratic, low-cost business is a different animal from a spread set in Beijing. I have owned and recommended Calumet since 2022, and I considered it one of the largest upside opportunities in my coverage universe, with returns largely uncorrelated with oil prices or the broader market. Importantly, what drives its stock price is completely unrelated to refining economics.

Conclusion

I am avoiding the U.S. independent refiners—Valero, Marathon, Phillips 66, and the smaller names alongside them—and that means reversing the Valero buy call I made in April 2024. The margin thesis was right, and the stock rose about 64%, and I would make that trade again. But this stock is not worthy as a core long-term holding.

I will change my mind under specific conditions: a durable re-rating of the group to roughly 10x free cash flow, through-cycle returns on equity that hold above the cost of capital rather than collapsing in every downturn, or refiners signing long-dated contracts that finally decouple their earnings from the spot crack. None of that is true today.

Until it is, I would rather own refinery-related stocks than the refiners themselves. An income investor holding pure refiners into this strength has better options, such as MPLX at more than double the yield on contracted cash flow, an integrated like Cenovus or Suncor that hedges the spread, or Calumet that sidesteps the negatives entirely, and every one owns assets and generates cash flows that lend themselves to business valuation.

Analyst’s Disclosure: Jon Costello has a beneficial long position in the shares of CLMT, CVE, MPLX, SU either through stock ownership, options, or other derivatives.