By: Jon Costello

The oil bulls have capitulated.

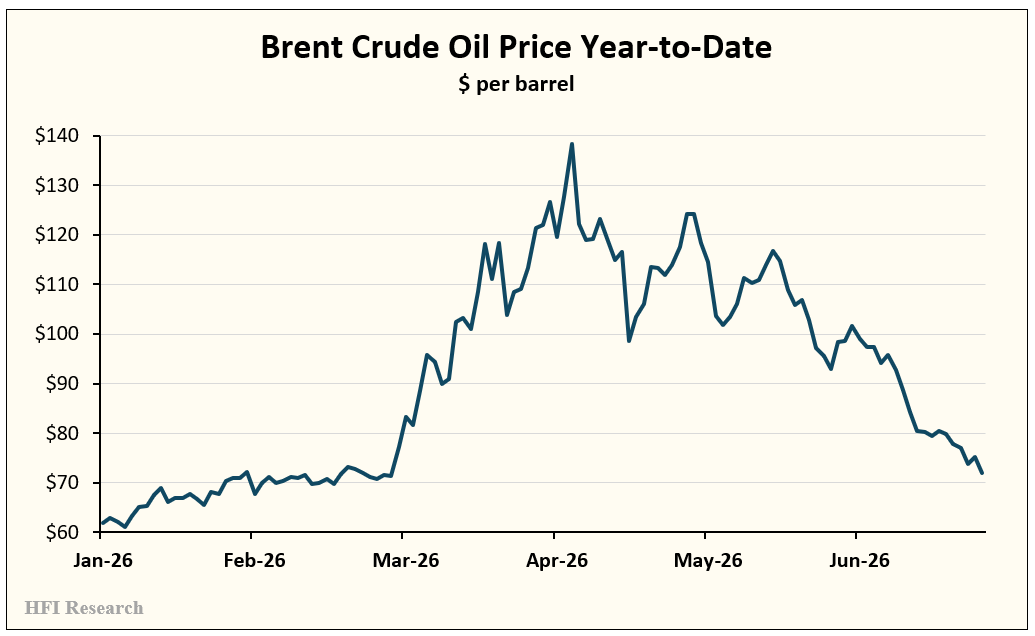

For the past two weeks, crude oil has relentlessly sold off. The war premium has evaporated. WTI has fallen back to around $70 per barrel, Brent has retreated into the low $70s, and sentiment has shifted from fear of a supply shock to anticipation of another period of oversupply.

Prices are now approaching the levels seen before the war began on February 28.

Judging by price action alone, the market appears convinced that the disruption in the Strait of Hormuz is effectively over.

But that conclusion is contradicted by the evidence. Commercial inventories continue to tighten. Refining margins remain at historically high levels. Iran has demonstrated that it retains the ability—and the willingness—to interfere with shipping in the Arabian Gulf. At the same time, approaches for deriving a fair range of oil prices from inventory levels suggest prices materially above today’s market. Those observations stand in direct contradiction to oil prices, now trading at pre-war levels.

When prices and fundamentals appear to contradict one another to such a stark degree, I find it useful to separate what the market is pricing today from what the underlying economics suggest over the investment horizon that actually matters to me. Today, those two perspectives have diverged sharply. Understanding this divergence is, in my view, the key to understanding both the recent collapse in oil prices and why I remain constructive over the medium term.

As a long-term equity investor with specialization in the energy sector, I’m not trying to predict where oil will settle next Tuesday or even next month. My investment theses depend on where industry fundamentals are likely to stand over the coming quarters and years, because those fundamentals ultimately determine the intrinsic value of the businesses I own and, by extension, the returns on my investments. Short-term price movements matter, but primarily because they are caused by developments that have less bearing on the long-term outlook, not because they necessarily change an investment’s economics.

When viewed from this broader perspective, I think much of today’s acute bearishness misses an important point: that the bulls and the bears are not necessarily disagreeing about supply and demand. Rather, they’re disagreeing about the element of time.

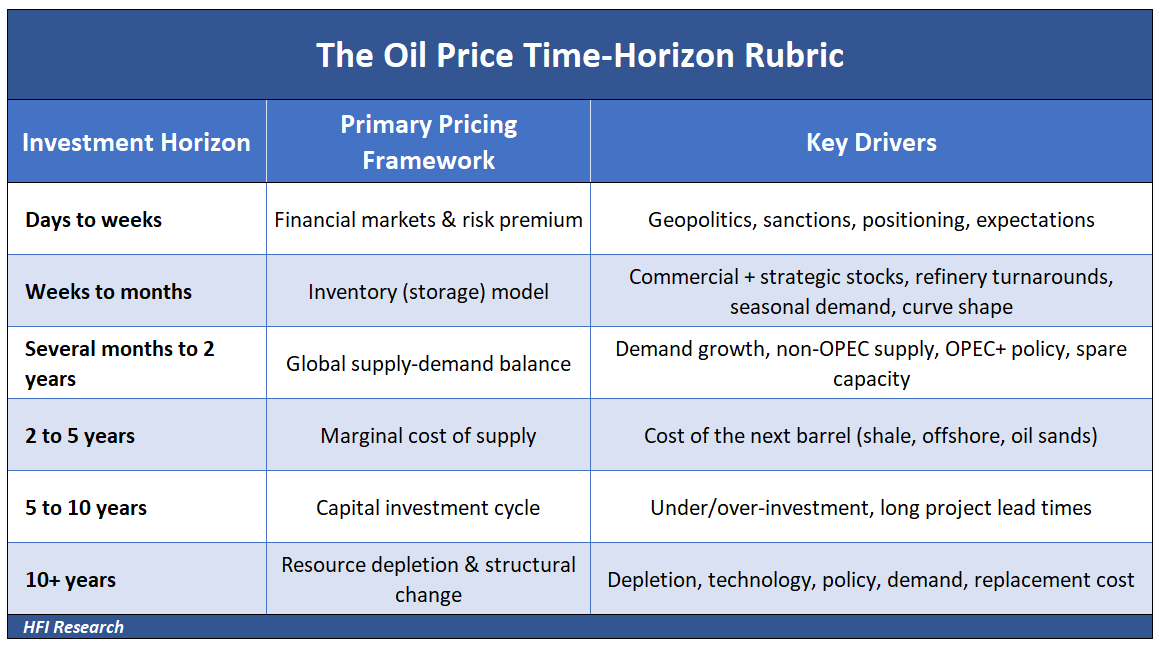

The Oil Market Doesn’t Have One Pricing Model

One of the biggest mistakes I see investors in the energy sector make is assuming that crude oil is governed by a single equilibrium model. It isn’t.

Oil is better understood as a series of nested economic models, each with its own influence across different time horizons. The table below illustrates some of the most prominent models of this kind.

Over days and weeks, prices are driven largely by financial positioning, geopolitical developments, and changing expectations.

Over the following months, inventories become the dominant variable. Small imbalances between production and consumption can lead to surprisingly large price swings because inventories act as the market’s buffer between supply and demand.

Over one to two years, the focus shifts toward the underlying balance between global production and consumption. OPEC+ policy, non-OPEC supply growth, and demand trends begin to dominate.

Beyond that, prices increasingly reflect the industry’s marginal cost of supplying the next barrel. If prices remain above that cost, investment accelerates and supply grows. If they remain below the marginal cost of supply, investment slows, production eventually tightens, and prices recover.

Finally, over the longest horizons, today’s capital spending decisions determine tomorrow’s productive capacity. Years of underinvestment cannot be corrected overnight, while excessive investment eventually creates its own oversupply.

Each of these models is valid.

The mistake is applying a particular model to the wrong time horizon. This is exactly what I believe the market is doing today.

The Futures Market Isn’t Pricing the Medium Term

If the medium-term outlook remains constructive, why isn’t today’s oil price already reflecting it?

The answer lies in understanding what oil futures actually represent.

It is tempting to think of the front-month futures contract as the market’s forecast of where oil prices are headed over the coming year. In reality, it is nothing of the sort.

A futures contract that expires in one or two months is fundamentally a pricing mechanism for crude that will be delivered over that time horizon. As time marches on, every futures contract eventually becomes the spot market. And as expiration approaches, the distinction between futures and spot disappears. That is why the nearby contract must ultimately price today’s physical equilibrium rather than where traders believe oil might trade months from now.

Moreover, the shape of the futures curve best balances today’s physical market across all delivery months. It emerges from current supply-and-demand conditions rather than from a collection of forecasts about future spot prices.

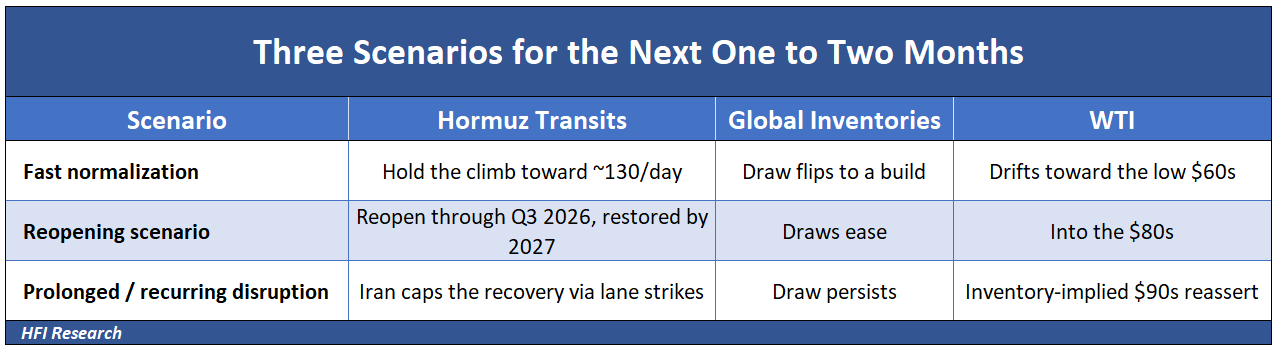

Viewed through that lens, the recent decline in front-month crude prices becomes much easier to understand. If temporary developments are expected to increase crude availability over the next several weeks—as I believe deferred cargoes and China’s reduced crude buying have done—then weaker nearby prices are entirely consistent with how the futures market is designed to function.

That tells us something important about current conditions.

The Short-Term Bears Are Right

Once the appropriate time horizon is identified, today’s market becomes much easier to understand. The short-term price weakness is not totally irrational. In fact, given recent developments in physical crude flows, it is largely understandable.

Many oil bulls have focused almost exclusively on the supply disruptions created by Iran’s interference with shipping in the Strait of Hormuz. Those disruptions are real, and they’re having a profound impact on fundamentals. Reliable estimates put the volumes of crude oil they have removed from global supply at more than one billion barrels over the past four months.

But they are only one side of the equation. At roughly the same time that Middle Eastern exports were being constrained, two powerful countervailing forces emerged, temporarily easing pressure on the physical market.

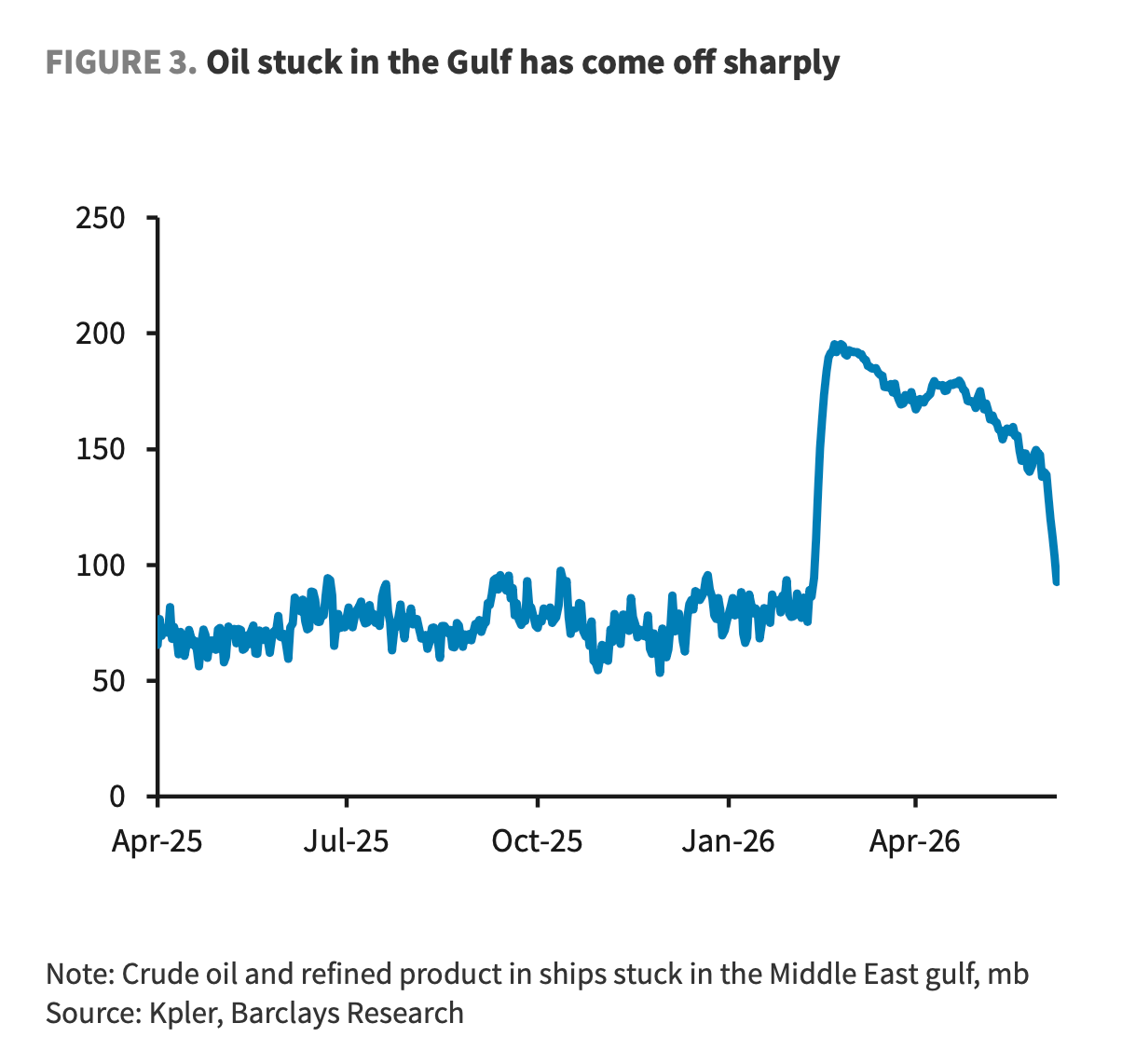

The first was the release of the crude cargoes from the Arabian Gulf.

When shipping through the Strait became uncertain, a substantial volume of crude accumulated aboard tankers waiting for a safer opportunity to exit the Strait. As transit gradually resumed following the U.S.-Iran memorandum of understanding and the subsequent easing of sanctions on Iranian oil exports, those deferred cargoes began moving to market. Meanwhile, the U.S. lifted sanctions on the sale of Iranian oil, allowing it to be sold globally. Combined, these measures released an estimated 170 million barrels from the Gulf.

Most trapped barrels have now exited the Gulf, as shown below.

Source: Barclays

This supply did not represent new production or a sustainable increase in global supply. Rather, it was the release of barrels that had been temporarily trapped by logistical disruptions. Even so, their arrival increased prompt physical availability just as refiners and traders were reassessing geopolitical risk.

This is a one-time adjustment rather than a lasting source of supply. Once the backlog has been cleared, the surge in supply represented by those barrels cannot occur again.

The second—and arguably more important—near-term factor depressing prices has come from China.

Rather than aggressively competing for replacement crude supplies, Chinese refiners have responded to the disruption by reducing refinery throughput, drawing down commercial inventories, and operating within Beijing’s existing restrictions on refined-product exports. The result has been a sharp decline in crude imports relative to first-quarter levels.

Importantly, that decline does not represent a collapse in end-user demand for petroleum products, at least not in full. Instead, it primarily reflects a temporary combination of lower refinery runs, inventory drawdowns, and policy decisions that have reduced China’s need to purchase crude on the international market. precisely when Middle Eastern supplies have become more difficult to move.

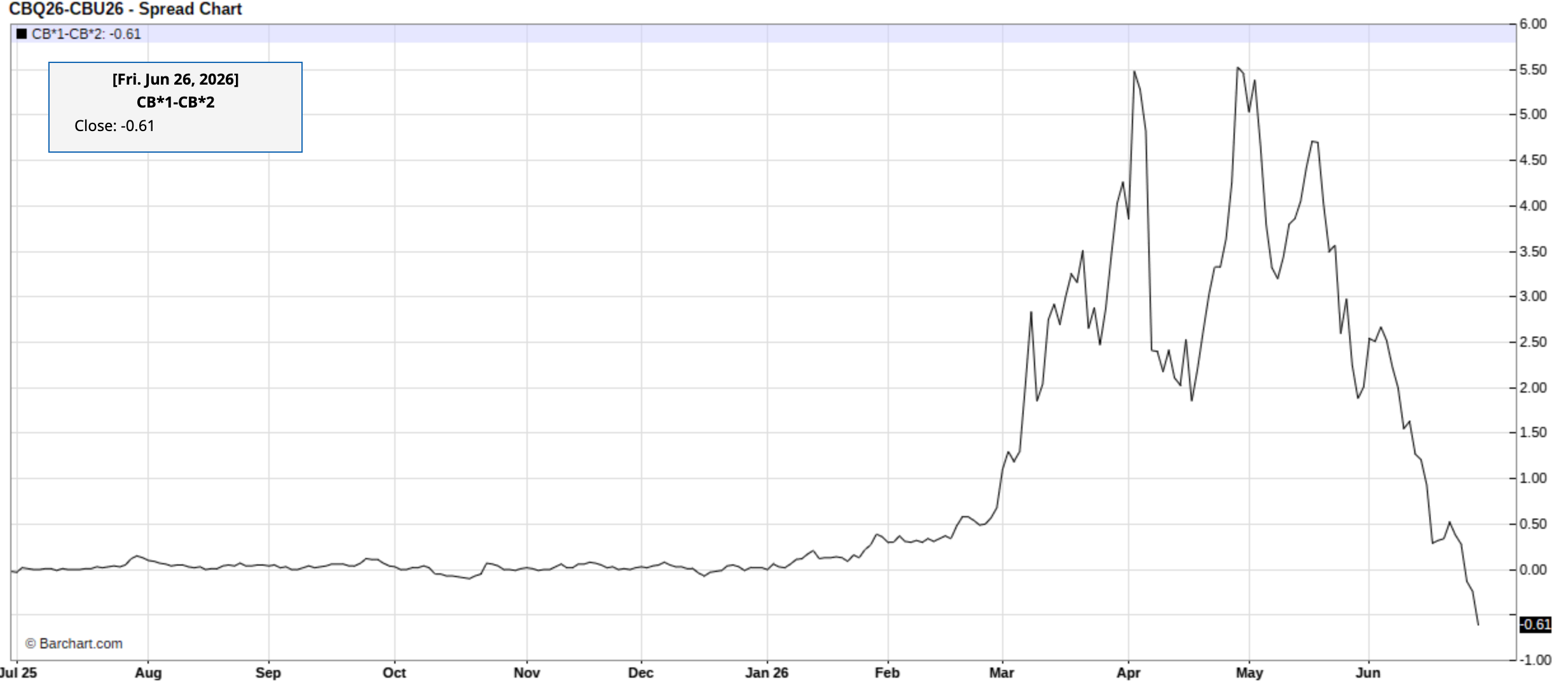

Together, these two developments have temporarily increased prompt crude availability while simultaneously reducing one of the world’s largest sources of incremental buying. It should therefore come as little surprise that Brent time spreads have weakened to year-to-date lows, and that nearby crude prices have come under pressure. In effect, one temporary force increased available supply while another temporarily reduced demand for internationally traded crude.

Source: Barchart.com, June 26, 2026.

In other words, the market is not behaving irrationally; it is correctly recognizing that near-term physical conditions have become less tight than many expected only a few weeks ago.

Where I differ from the market is not in that assessment. It is in what happens next.

Neither the release of deferred cargoes nor China’s policy-driven demand restraint represents a permanent improvement in the global supply balance. One is a finite logistical adjustment. The other reflects commercial and policy decisions that can reverse as inventories normalize and refinery utilization recovers.

These temporary factors help explain today’s prices. They do not explain the medium-term physical balance.

The Medium-Term Outlook Remains Constructive

If the short-term bears are right, the next question becomes obvious: why haven’t prices responded the way inventories imply they would?

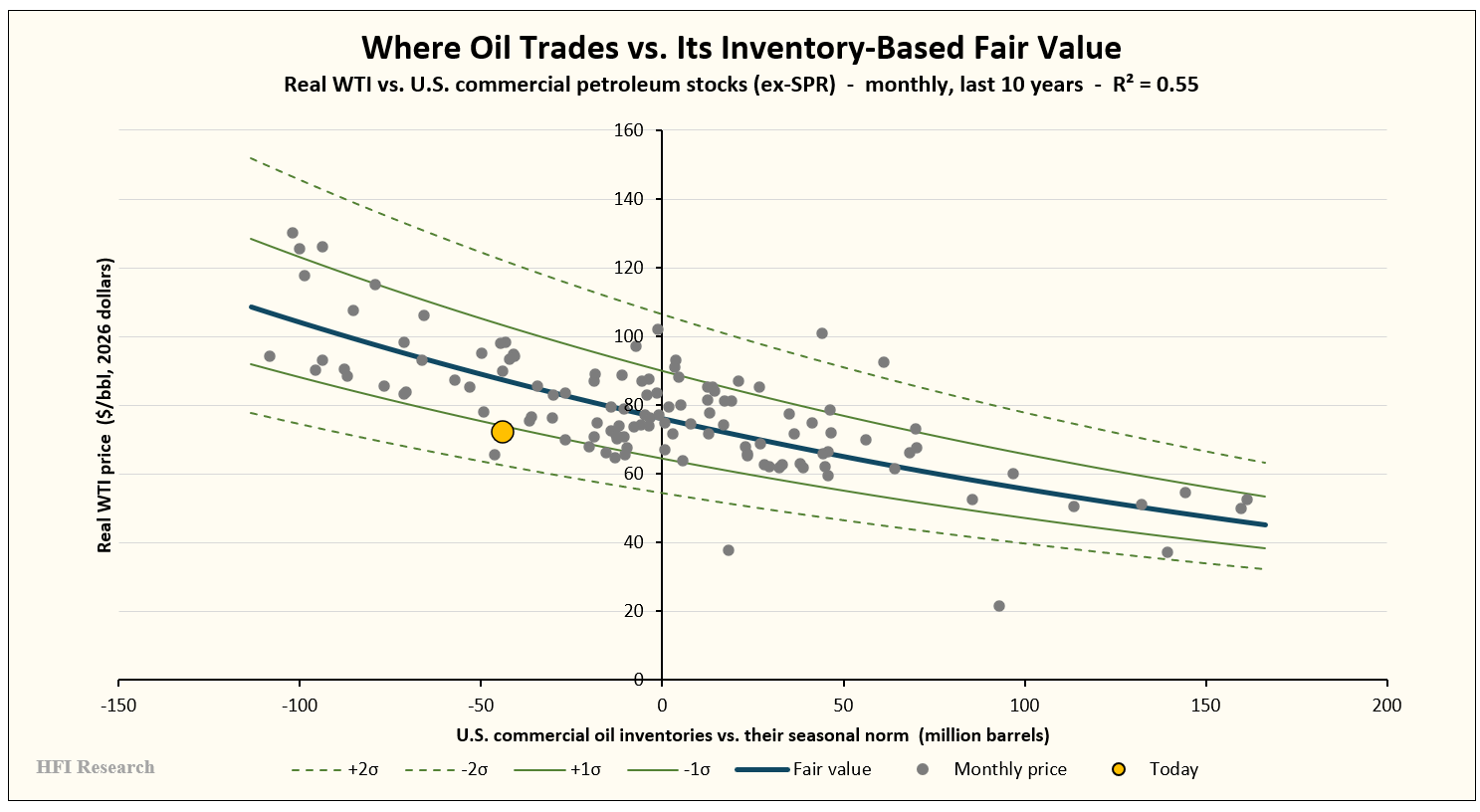

Historically, inventories have been among the most reliable indicators of medium-term oil prices because they reflect the cumulative effect of countless individual supply and demand decisions. Production, refinery activity, imports, exports, logistics, and demand all eventually affect inventory levels. For that reason, inventories often provide one of the clearest summaries of the medium-term physical balance.

While prices may overreact to geopolitical headlines, financial positioning, or temporary logistical disruptions, inventories ultimately reveal whether the physical market is tightening or loosening.

By that measure, today’s oil market appears considerably tighter than current prices suggest.

One approach I use to estimate fair value is a regression that relates oil prices to commercial inventory levels. Like any model, it is imperfect, and it should never be relied upon in isolation. But over long periods, it has proven useful because inventories sit at the center of the medium-term pricing model. They absorb the cumulative effects of production, consumption, imports, exports, refinery activity, and logistics.

Today, my regression indicates a fair value for WTI of approximately $87 per barrel, 26% above the current market price.

Moreover, inventories are trending lower. If continued, it will exert further upward pressure on prices.

This model is not the only evidence illustrating that the market is tighter than current prices imply.

Several independent inventory-based approaches reach broadly similar conclusions. Whether the analysis focuses on OECD inventories, global days of forward demand, or deviations from long-term inventory norms, the message is largely the same: the physical market remains considerably tighter than today’s outright price would suggest.

The implication is that prices have significantly more upside than downside. Barring a rapid normalization of flows through the Strait to pre-war levels, prices are likely to remain above $80 per barrel, and well above that, as the market tightens further.

This conclusion is also consistent with what we observe outside of inventory statistics. Refining margins remain at historic highs, indicating that refiners continue to compete aggressively for crude despite weakness in outright futures prices. Physical crude differentials remain firm across many regions, indicating that nearby barrels continue to command a premium despite weakness in outright futures prices.

None of this proves that prices must immediately move higher. As any long-term energy investor knows, markets can remain disconnected from medium-term fundamentals for longer than expected, particularly when temporary logistical adjustments dominate near-term trading.

But it does suggest that today’s weakness should not automatically be interpreted as evidence that the underlying supply deficit has disappeared.

The Strait Still Matters

In my view, the answer depends less on today’s supply levels than on tomorrow’s deliverability.

That distinction matters because oil markets are ultimately constrained not by how much crude exists underground, but by how much can be delivered to refiners when and where it is needed.

This is where I believe many analyses become overly optimistic about the medium term. Many investors view the Iran conflict as a done deal. Almost every morning, I hear CNBC commentators state this view and use it as a reason to argue for lower interest rates or for clear sailing for the economy and the stock market.

In my view, the market is making a subtle but important mistake. It is treating the recent release of deferred cargoes and China’s temporary restraint in demand as though they have permanently resolved the underlying supply deficit.

I believe they have merely postponed its effects.

Investors extrapolate the current price into the future. However, the assumption that today’s price will hold implies that barrels will continue to move to market without meaningful disruption. Recent events suggest that the assumption warrants considerably more caution than the market currently assigns it.

Iran has demonstrated its ability to interfere with one of the world’s most important energy chokepoints.

On Thursday, Iran reinforced its capability when Iranian forces reportedly attacked another commercial cargo vessel transiting the region. Then today, after a U.S. response that attracted Iranian military sites, Iranian drones were reported to have attacked Bahrain and another ship.

While two or three incidents do not determine the market’s long-term direction, they serve as a reminder that the threat to Gulf shipping remains active, not merely theoretical. Moreover, they suggest that consensus is moving too quickly to treat the conflict as resolved for oil pricing purposes.

Even if tensions continue to ease, the events of the past several months have highlighted how quickly logistical disruptions can tighten the physical market. Not because production disappears, but because deliverability changes.

Consider that a barrel of oil has little economic value if it cannot reach the refinery that needs it. Recent events in the Strait of Hormuz serve as a reminder that production and deliverability are not interchangeable concepts. The market may temporarily appear better supplied as deferred cargoes finally reach their destinations, but those logistical adjustments do not eliminate the underlying vulnerability of one of the world’s most important energy corridors.

Deliverability will remain a key issue in the oil market as long as Iran exercises control over transit through the Strait. At the moment, it is attempting to limit transit on the Strait’s southern lane, which is controlled by Oman, in coordination with the U.S military. For the moment, given the current lack of traffic through this lane according to satellite trackers we follow, it is doing so successfully.

Market participants are behaving as though the Strait of Hormuz has returned to being a solved logistical problem. Recent events suggest it has not. That distinction matters because if deliverability remains uncertain, today’s apparent easing in physical conditions may prove considerably more temporary than current prices imply

Deliverability Has Become the Critical Constraint

Other temporary supply cushions are also beginning to disappear. At current release rates, Strategic Petroleum Reserve (SPR) drawdowns have only another three to six weeks of supply remaining. Likewise, commercial inventory drawdowns outside of the SPR cannot continue indefinitely without eventually requiring replenishment. These measures can delay the market’s adjustment, but they cannot eliminate it. The common thread is that each of these developments buys time. None creates new long-term supply.

Oil is unusual among major commodities because new supply cannot be created quickly. Developing large conventional fields takes years. Expanding offshore production often takes even longer.

Even the U.S. shale industry—by far the world’s most responsive source of significant incremental supply—has become more disciplined than it was during the previous decade. Producers now prioritize shareholder returns over rapid production growth, limiting the industry’s ability to offset global supply shortfalls through sheer drilling activity.

This reality means the market’s longer-term balance depends less on today’s production than on tomorrow’s production capacity, which is why deliverability is especially important.

The implications extend beyond the immediate disruption itself.

For decades, the oil market has viewed OPEC’s spare production capacity as an important buffer against unexpected supply shocks. This view assumes that those additional barrels could be delivered to market in short order, as needed, on a scale sufficient to satisfy demand and keep prices stable. In fact, the technical definition of “spare capacity” is the ability of a producer to rapidly surge supply significantly above its current level and maintain that elevated level for at least 90 days.

Iran has demonstrated that it possesses sufficient influence over traffic through the Strait that the market can no longer assume OPEC’s spare capacity is fully available precisely when it is most needed.

If Iran can meaningfully disrupt tanker traffic through the Strait of Hormuz, then a significant portion of OPEC’s spare capacity may be less immediately available than headline production figures suggest. In other words, spare capacity and deliverable capacity are no longer synonymous. Spare capacity is only valuable if it is deliverable.

This, I believe, helps explain an important difference in perspective between oil specialists and the broader investment community. This distinction is more familiar to participants who focus on the physical oil market than to investors who primarily encounter oil through futures prices or macroeconomic commentary. Energy market participants tend to think in terms of physical flows and deliverability. Much of the broader investment community understandably focuses on reported production capacity. Under normal conditions, those concepts are nearly identical.

Other important implications flow from the emerging order oil market order. For example, spare capacity becomes far less relevant if it can’t be delivered to market in a timely manner. By rendering OPEC’s spare capacity less relevant to the market, Iran can weaken Saudi Arabia’s position as the most powerful force in the oil market, given Saudi Arabia’s control over export volumes and flows.

Conclusion

The recent selloff in oil is real. In my view, however, it reflects a series of temporary adjustments rather than a lasting improvement in the oil market’s underlying balance. Deferred Gulf cargoes have returned to market, China’s crude imports have declined, and strategic and commercial inventories have provided a temporary cushion to supply. Those developments explain why prompt crude prices have weakened. They do not, in my view, explain the medium-term outlook.

The broader evidence continues to point in a different direction. Inventories remain historically tight, and refining margins and physical differentials continue to indicate robust competition for crude. Recent events in the Strait of Hormuz have highlighted the growing importance of deliverability alongside production. Temporary adjustments have eased near-term conditions, but they have not created new productive capacity or eliminated the underlying supply deficit.

Could I be early? Absolutely. Markets often remain focused on temporary developments longer than fundamentals alone might suggest, and a sustained return to normal shipping conditions through the Strait would reduce many of the risks discussed here. But that uncertainty has not altered my outlook. I continue to believe the medium-term fundamentals remain considerably stronger than today’s market price implies, and I expect significantly higher average oil prices through the balance of the year, and likely well beyond that.

For investors with time horizons measured in quarters rather than weeks, I believe the appropriate response is to stay the course and allow the underlying fundamentals sufficient time to make their weight felt in prices.

Ultimately, my view has not changed.

The market is reading the wrong clock.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of the HFIR Energy Income Portfolio either through stock ownership, options, or other derivatives.