(Public) Tamarack Valley

Editor’s Note: This article was first published to HFI Research main subscribers on Dec 22, 2023. Please note that the share price and various other figures in the article below are older data.

Note: Dollar references are to Canadian dollars unless otherwise specified.

Tamarack Valley Energy (TVE:CA) shares are the second-worst performer year-to-date among Canadian mid-cap and large-cap E&Ps. Only natural gas-weighted Birchcliff Energy (BIR:CA) shares have fared worse. Investor sentiment toward TVE has suffered as management under CEO Brian Schmidt repeatedly assured investors that increased capital returns were imminent, only to make a large acquisition that added debt and pushed back the capital return time horizon.

While management has failed to properly set investor expectations and has a penchant for acquisitions, it has outperformed from an operational perspective. The company holds some of the most economic acreage in North America. TVE's asset quality is evident in its drilling results. Since acquiring its Clearwater acreage, it has drilled some of the best wells in Canada.

Investor sentiment has pushed its shares far below our estimate of intrinsic value. While management hasn’t sworn off acquisitions, we don’t expect another major deal, at least until debt is paid down to less than $500 million. Meanwhile, operations should continue to perform well, and cash flow surges as WTI trades above US$80 per barrel.

We rate TVE shares as a Buy with a $5.00 price target. The shares offer 58.7% upside to our price target from their current price of $3.15.

Introduction

TVE operates in three regions in Alberta. It holds high-quality core acreage positions in the Clearwater heavy oil play, where it produces approximately 35,700 boe/d, as well as in the Charlie Lake light oil play, where it produces 16,200 boe/d. It also has a portfolio of enhanced oil recovery opportunities in southeast Alberta that produce approximately 14,800 boe/d.

Source: TVE December 2023 Investor Presentation.

TVE has spent the last few years high-grading its portfolio by increasing its presence first to Charlie Lake and, more recently, the Clearwater. It has also disposed of lower-quality, non-core assets. Management touts TVE’s asset quality, as well as its move away from the lower-quality Cardium play, in the slide below.

Source: TVE December 2023 Investor Presentation.

After several acquisitions in 2022, TVE has emerged as the largest producer in the Clearwater. In February 2022, it acquired Crestwynd Exploration, a privately owned Clearwater producer, for $184.7 million, paying $92.6 million in cash and 26.3 million TVE shares at $3.50. Crestwynd produced approximately 4,500 boe/d of 100% liquids. Then in June 2022, TVE acquired privately-owned Rolling Hills Energy for $93 million and other assets in the Peavine area of the Clearwater. Rolling Hills produced approximately 2,100 boe/d.

TVE’s biggest leap into the Clearwater came in October 2022, when it acquired privately owned Deltastream Energy for $1.425 billion. At the time, Deltastream was producing approximately 20,000 boe/d of 93% liquids. Its production accounted for 21.5% of the Clearwater’s 93,000 boe/d of total production. TVE financed the deal with $825 million of cash, $300 million in a deferred acquisition payment note, and $300 million of TVE shares at $3.75.

TVE Shares Remain in the Doghouse

TVE shares have been penalized ever since the Deltastream deal. The shares failed to get as much traction as peers as oil prices rose in mid-2023. When prices collapsed later in the year, they sold off even more.

While the long-term impact of TVE's Clearwater acquisitions is open to debate, the fact of the matter was that in 2022, the company had to do something to address its shrinking reserve life. TVE’s 2021 reserve report estimated its remaining proved and probable reserve life at 8.8 years—too short for shareholder comfort. The Clearwater deals in 2022 lengthened its reserve life to 11.3 years and gave TVE sufficient scale to improve its results. They also allowed the company to replace 118% of its produced reserves in 2022 through the drill bit.

The clear negative was that TVE chose to pay up for quality. Moreover, it did so in mid-2022, when WTI was trading above US$90 per barrel. TVE paid $66,261 per flowing barrel for Deltastream, one of the highest-priced acquisitions that year.

Admittedly, “per flowing barrel” is a flawed, back-of-the-envelope metric, but it can be useful in gauging what an acquirer gets relative to the consideration they give. Comparing the Deltastream deal with other recent deals illustrates its high price. For starters, TVE's Rolling Hills acquisition earlier in 2022 was made at a far more reasonable $44,285 per flowing barrel. Recent peer acquisition metrics were also much lower, as shown in the table below.

Clearwater core acreage could fetch a higher price due to its nearly 100% liquids weighting, lower decline rate, breakeven costs than the Montney and Duvernay plays, and enhanced oil recovery opportunities. But there are negatives that offset these positives. For one, the play produces heavy oil that trades at a discount from lighter grades. Heavier grades are exposed to the volatility inherent in the WTI-WCS differential.

Adding insult to injury for TVE shareholders in the wake of the Deltastream deal, management proceeded to overpromise and underdeliver on the deal’s anticipated financial benefits. Its guidance of accelerated debt paydown shortly after the deal closed never materialized. The same can be said for its guidance of increased shareholder returns. While a large part of management’s underperformance was lower-than-expected prevailing commodity prices, it should have known better than to have promised so much on the basis of US$85 per barrel WTI.

Further complicating matters was that Deltastream’s largest shareholder, Arc Financial, became TVE’s largest shareholder after the deal, holding approximately 11.7% of TVE shares. Over the next few quarters, Arc dumped TVE shares onto the market, putting downward pressure on TVE’s share price and likely playing a role in the shares’ inability to rally despite surging oil prices.

TVE's Financial Picture is Improving

Despite management’s snafus, improvement is clearly underway, though you wouldn’t know if from looking at TVE’s stock price. By the end of the year, the company will have addressed its near-term debt maturities. It also will have reduced debt below management’s initial net debt target of $1.1 billion.

At the end of the third quarter, TVE’s debt consisted of $106.7 million in Deferred Acquisition Payment Notes (DAP) issued in conjunction with the Deltastream acquisition. As a large current liability, these most likely have been paid off with the proceeds of recent asset sales.

TVE has $200 million outstanding on its non-revolving two-year Term Loan Facility. After the DAP Notes, The Term Loan Facility is TVE’s next most likely candidate for repayment, as it is required to allocate 50% of annual excess cash flow to the notes.

The company also has $648.6 million drawn on its three-year $700 million Sustainability-Linked Lending Facility and $300 million of 7.25% senior unsecured Sustainability Linked Notes due May 2027. These will probably be paid off over time with free cash flow.

At the end of the third quarter, total debt stood at approximately 1.0-time cash flow at WTI in the mid-US$70s per barrel, higher than most peers but by no means onerous. Decommissioning obligations stood at a reasonable $166.9 million.

Unless WTI is sustained below US$65 per barrel, TVE should have no problem meeting its debt service obligations going forward. The recent asset sale proceeds go a long way toward minimizing near-term risk.

In early 2024, TVE is likely to begin to increase cash flow distributions to shareholders. By then, it should have paid down enough debt to achieve management’s capital return framework shown in the circled area below. As such, it will be allocating 75% of free cash flow to debt reduction and distributing 25% to shareholders until net debt falls below $900 million.

Source: TVE December 2023 Investor Presentation. Red-dotted line added by author.

If oil prices remain at current levels, we expect TVE to generate roughly $150 million of free cash flow, 25% of which we expect to be allocated to shareholders in the form of increased dividends. Given the shares’ discount to our estimated intrinsic value, repurchases will be accretive to intrinsic value per share.

The Positives from Deltastream

From a purely operational perspective, the move into the Clearwater has been a success. Operating metrics have improved, while TVE’s Clearwater well results are routinely listed among the best in Canada. Its Charlie Lake wells also rank as some of the best in Canada.

TVE’s Clearwater acquisition is likely to generate attractive returns with WTI above US$85 per barrel. At those prices, legacy Deltastream wells pay back their capital investment in less than six months, providing some of the most attractive drilling economics in North America.

But even if WTI trades below US$85, the Deltastream assets improve TVE’s overall financial performance. We believe the market is missing this fact. TVE’s recent results demonstrate the improvement.

While the market was preoccupied with the questionable financial aspects of the deal, TVE was executing various Clearwater infrastructure initiatives that would improve drilling results and, in turn, increase TVE’s operating netback, which is the cash flow left over after royalties, operating expenses, and transportation costs, but before corporate expenses such as G&A and interest.

Throughout 2023, management has described the year as a “tale of two halves,” in which stepped-up infrastructure investment in the Clearwater in the first half, gives way to an improved operating performance in the second. In this category, at least, management met its own guidance.

TVE’s first-half infrastructure investments are already paying off. Management’s two stated objectives were to increase price realizations and reduce operating costs. It met both in the third quarter. The charts below show the third-quarter improvement in price realizations.

While the top line improved, costs fell in the third quarter, as shown below.

The upshot of these financial improvements is a higher operating netback. This was management’s foremost goal after the Deltastream deal.

Consider that during the three quarters before the deal, WTI averaged US$98.08 per barrel, and TVE’s operating netback before hedges averaged $48.04 per barrel. In the three quarters since the deal closed, WTI averaged a significantly lower US$77.39 per barrel, but TVE’s operating netback before hedges averaged $42.74. The difference is attributable to better realizations and reduced operating expenses, and, to a lesser extent, lower royalties, slightly offset by higher interest expense and cash tax payments.

Bullish Factors Yet to Be Reflected in TVE Shares

TVE’s current market price implies that its improved results are not sustainable. It also indicates investors are afraid that management will make another acquisition. If either of these proves incorrect, TVE shares offer huge upside. In fact, TVE shares have gotten so cheap that they can do well even if management only executes on its most basic goals, such as paying down debt and increasing share repurchases.

In the fourth quarter, management has likely made significant progress on the debt reduction front. On October 19, TVE sold non-core Cardium acreage that was producing 4,500 boe/d in the third quarter for $123 million in cash and the assumption of $119 million of asset retirement obligations. The deal closed on November 3, when management reported that its cash proceeds were put toward debt reduction. TVE booked a $97.7 million loss on the assets when they were held for sale in the third quarter. While the asset sale will reduce TVE’s production by approximately 6,000 boe/d, it will increase the company’s oil weighting and further improve its operating netback.

Then on December 13, TVE announced an agreement with 12 indigenous groups, in which it would transfer assets valued at $172 million of infrastructure assets into an entity in which it would acquire an 85% non-operated working interest. It would receive consideration of $146.2 million in cash and a 15% operated working interest in the entity. The deal closed on December 15.

This was clearly a good deal for TVE shareholders. It came at an attractive 8.3-times cash flow, multiple times TVE’s valuation. It also includes a taxpayer-funded loan guarantee through the Alberta Indigenous Opportunities Corporation (AIOC). Management plans to allocate $100 million of the proceeds toward debt reduction, which it expects to bring debt below the $1 billion mark. TVE can allocate cash flow generated by the assets in the future to fund its Clearwater development.

The recent debt reduction will decrease interest expense and thereby boost free cash flow.

Other developments that could benefit free cash flow in the near term include the completion of the Trans Mountain Pipeline Expansion. If this project ever gets completed, it will increase regional takeaway capacity, thereby improving market access and realized pricing for TVE’s Clearwater oil production, which comprises 55% of its total production.

Furthermore, the company is spending approximately $45 million on a new sour gas processing plant. After the plant enters service, which is currently expected in the first quarter of 2025, it will allow for an additional 2,000 boe/d of production, which bodes well for TVE’s cash flow that year and beyond.

Aside from these operational features of TVE’s business, its asset base appears to be more than meets the eye. Management believes its Clearwater reserves are dramatically understated because the play is conventional—requiring conventional reserve accounting—but the heavy oil resource it contains is more akin to unconventional production. These claims are supported by other companies that saw their Clearwater reserve estimates increase after their reserves auditors recognized waterflood acreage in their reserves.

Management estimates a massive 8.7 billion barrels of oil-weighted resources in its Clearwater acreage, of which only 0.9% has been booked in TVE’s total proved plus probable reserves. Management believes its waterflood design improvements will enhance recoveries, which could deliver a significant boost to production volumes. Its waterflood design will also lower TVE’s total production decline rate by 2%. Each 1% improvement is expected to save the company $12 to $15 million per year in capex aimed at maintaining production.

An independent reserve audit commissioned by the AIOC also supports management’s claim that TVE’s reserves are understated. The audit was conducted to gauge the quality of assets backing the loan used by the indigenous groups to fund their recent deal to acquire TVE’s Clearwater infrastructure assets. It put the assets’ reserve life in the range of 25-30 years of primary drilling. The audit estimated the acreage had 1,785 drilling locations, significantly more than the 1,150 locations that TVE carries in its own reserve accounting. When enhanced oil recovery potential is included, management estimates TVE’s Clearwater production could span 50 years. Clearly, this puts the company in a better position vis-à-vis its reserves than most of its conventional E&P peers.

Valuation

TVE’s stock seems to gravitate toward a valuation of around 2.0-times forward cash flow, among the lowest for a public North American E&P.

At current oil prices, TVE shares offer only slightly lower free cash flow yield than BTE and CPG at current oil prices, but TVE benefits from a longer reserve life and higher liquids weighting.

TVE’s cash flow breakeven is around US$63 per barrel WTI, on the higher side among peers. However, TVE’s interest costs run in excess of $4 per barrel. As those come down, so will its breakeven cost per barrel. If oil prices fall further, it can also reduce the $45 million budgeted for infrastructure-related capex in 2024 and still keep production flat.

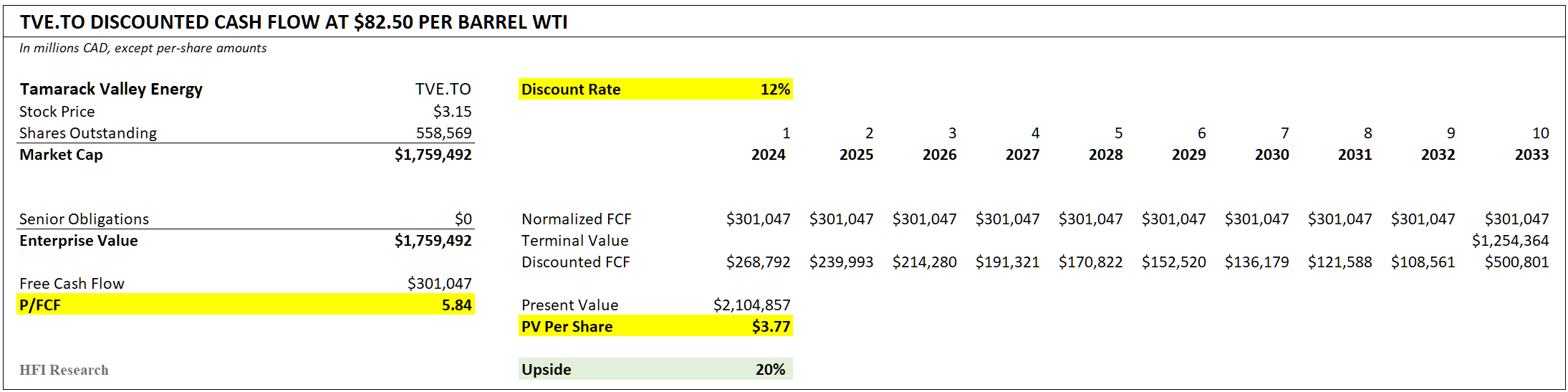

Our conservative discounted cash flow scenario, which discounts constant free cash flow at US$82.50 per barrel WTI, uses a 12% discount rate, and cuts the terminal value in half, values the shares at $3.74, implying 19% appreciation.

Valuing the shares instead using a 10% discount rate and not cutting the terminal rate implies the shares are worth $5.39, for 71% upside.

These valuations fail to account for the company’s significant torque to higher oil prices. For instance, undiscounted free cash flow surges higher as prices rise above $85 per barrel. The shares offer the prospect of more than a double to trade at a 12% free cash flow yield at US$90 per barrel WTI.

To put TVE’s cash flow generation into perspective, the table below illustrates the potential for increased dividends and buybacks once TVE has reduced debt to low levels.

The company could afford to pay out $0.80 per share above its current dividend at US$90 per barrel WTI.

Conclusion

TVE’s improving operational performance, long asset life, cash flow torque to oil prices, highly economic assets, falling debt balance, and imminent share repurchases make its shares attractive at their current depressed price of $3.15. These positives offset the primary negative of management’s failure to communicate realistic capital allocation targets.

Investors who can look to the long-term and stomach volatility should consider TVE shares in the same class as BTE and CPG. All three are high-torque names still working to reduce leverage. All these stocks offer the prospect of multi-bagger returns if oil prices are sustained at high levels.

While we understand the market’s reluctance to believe in management, we expect management to acknowledge its poor reputation among investors as the source of the shares’ discount and attempt to correct it. After all, CEO Brian Schmidt is on record stating that most of his net worth resides in TVE shares, so he’s incentivized to increase the share price. In our view, all it would take for management to improve its standing with investors is to publicly swear off doing big deals and then stay true to its word for another 12 to 18 months. In the meantime, TVE’s operating performance will likely remain strong, which bodes well for its financial performance if oil prices increase as we expect in 2024.

For these reasons, we’re much more positive about TVE’s prospects than the stock market. We rate the shares Buy with a $5.00 price target. With the shares trading at $3.15 and oil market fundamentals set to improve over the coming months, investors should begin buying TVE shares now.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.