(Public) Strathcona Resources - Our Favorite Name For The Incoming Multi-Year Oil Bull Market

Editor’s Note: This article was first published to HFI Research and Ideas From HFI Research subscribers on May 17, 2024. Please note that all market data in the article will differ. Following the Q2 earnings release and the dividend announcement, we will be publishing an update to subscribers by tomorrow. Please stay tuned for that.

Please read Strathcona Resources part 1 and part 2.

The outlook for oil prices is improving. Over the coming weeks, we expect prices to stabilize as refinery maintenance ends and the summer driving season begins. The third quarter will likely see a large supply deficit, which should draw down global oil inventories and push prices well into the $80s per barrel range.

Our Top Pick for the Oil Upcycle

Of all the stocks in our coverage universe, Strathcona Resources (SCR:CA) has the combination of attributes that make it our favorite way to play higher oil prices. We discuss the most important ones below.

Strong first-quarter results. SCR reported first-quarter earnings yesterday morning. Operating results were in line with analyst consensus expectations, as well as our own. Production came in at 185,122 boe/d and consisted of 32.5% bitumen, 28.0% heavy crude oil, 10.4% light oil and condensate, 6.3% NGLs, and 22.8% natural gas.

Financial results outperformed expectations. Funds from operation per share came in at $2.13, beating consensus expectations of $2.06.

Guidance remains intact, with production expected to increase and average 190,000 boe/d for full-year 2024.

The market greeted the results with an 11% rally that began yesterday and ran through today. We went long at $30.80. The shares currently trade at $34.

The quarter saw little by way of news. Operationally, approximately 4,400 boe/d of SCR’s Lloydminster heavy oil barrels were held in inventory as construction of a new rail terminal in the U.S. Gulf Coast was completed. The facility will allow SCR to obtain a premium to WCS Houston pricing on its heavy oil. Management expects to sell down the inventory at attractive prices over the next six months.

In terms of capital allocation, debt ended the quarter at $2.6 billion, and management expects to reach its debt target of $2.5 billion by mid-year. The company intends to announce its plans for distributing free cash flow to shareholders in its next earnings conference call. Management is considering initiating a small base dividend, which will be supplemented by variable dividends. Management also remains open to the possibility of repurchasing shares from existing shareholders who are seeking an exit.

Management’s interests are aligned with public shareholders. SCR’s management is highly incentivized to perform for shareholders. The company was built under the leadership of Adam Waterous, who controls the general partner of the Waterous Energy Fund (WEF). The limited partnerships that comprise the WEF collectively own 194.5 million of SCR’s 214.2 million shares outstanding, representing a 90.8% ownership interest.

WEF has been an outstanding steward of its limited partners’ funds. Year after year, it has steadily grown SCR’s cash flow generation potential and net asset value per share. We expect no less with regard to the newly-public SCR.

Management’s alignment with shareholders increases the likelihood that SCR allocates capital in a shareholder-friendly manner. We’re far less confident of such behavior in most other E&Ps, in which management isn’t a major shareholder.

One reason SCR came public in October last year was to enhance liquidity for WEF limited partners who sought an exit from the fund. Over time, as limited partners sell their shares through secondary offerings or by other means, SCR’s trading liquidity will increase. A larger float will increase the stock’s appeal to larger buy-and-hold fund managers, further supporting its share price.

Built for torque. Beginning in 2017, Adam Waterous cobbled together the assets that formed SCR for the express purpose of generating massive cash flow in a supply-constrained oil market with sustained high prices. Most of the company’s assets were acquired during years when oil prices were low and sentiment was gloomy.

We expect SCR and other companies with significant upside to higher oil prices to be increasingly viewed as the most desirable oil equity investments as global demand grows, supply growth is harder to come by, and oil prices trade at higher levels in the coming quarters and years.

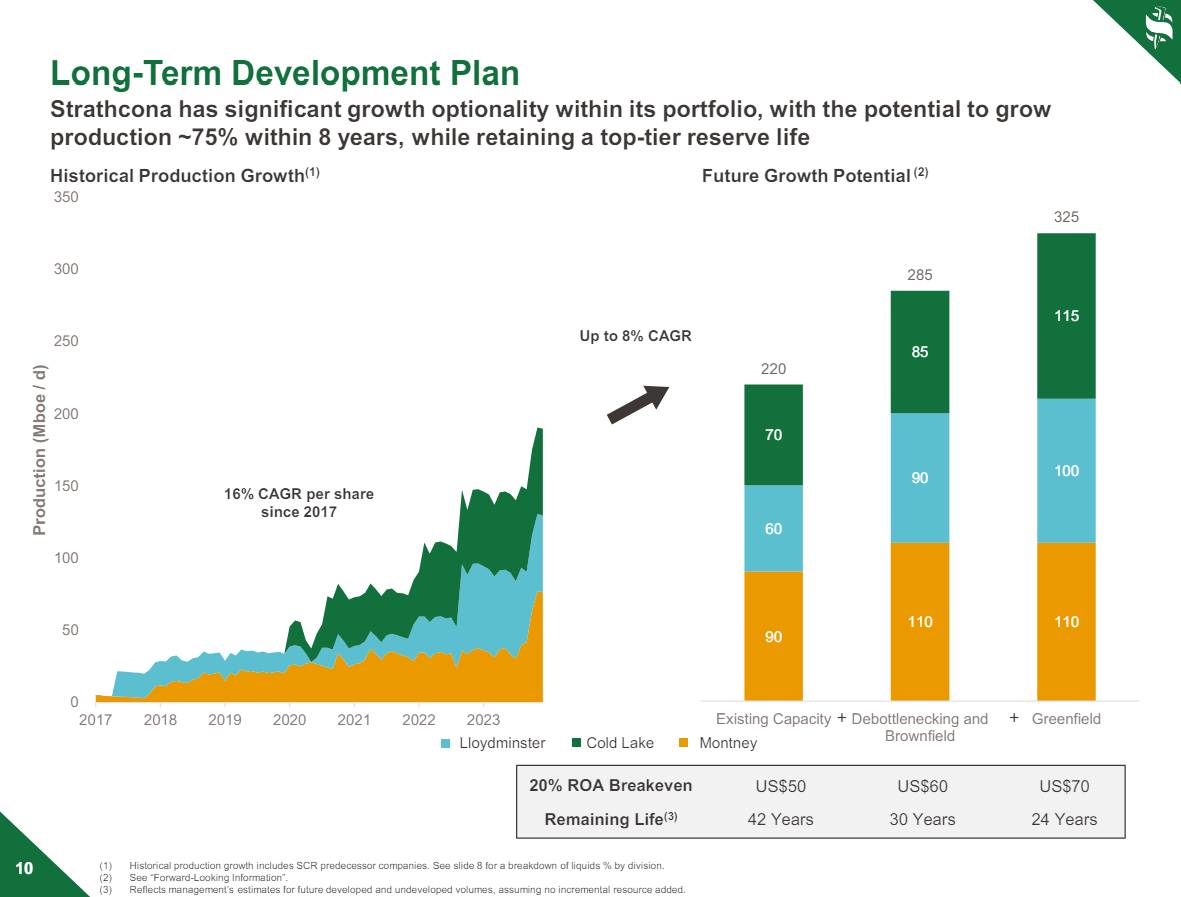

Production growth. Consistent with management’s goal to compound value per share over the long term, SCR expects to grow production by 75% over the next eight years, representing an 8% compound annualized growth rate. The graphic below shows SCR’s expected growth trajectory.

Source: SCR May 2024 Investor Presentation.

Production growth will be driven by expansion projects that the company expects will add another 25,000 boe/d of production by year-end 2026. Management expects the projects to lower SCR’s capex requirements.

Long-lived reserves. E&Ps are ultimately valued based on how much free cash flow they generate over their lives, but reserve composition and longevity determine the extent of the free cash flow they can generate.

SCR is in a rare group of E&Ps with reserves that span multiple decades at current production rates. Its PDP reserves span six years, but proved reserves extend out 26 years.

SCR’s peers with long reserve lives tend to be of higher quality. They include Canadian Natural Resources (CNQ:CA), Tourmaline Oil (TOU:CA), and Athabasca Oil (ATH:CA). SCR is clearly an asset-rich company, which opens up opportunities for bolt-on acquisitions and selective asset dispositions aimed at maximizing value for shareholders.

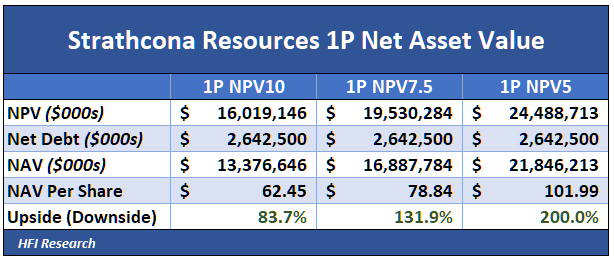

Based on proved reserve values at $87.50 per barrel WTI and $2.25 AECO natural gas, we estimate that SCR’s net asset value is $62.45 per share using a 10% discount rate. This equates to 83.7% upside from its current $34 share price.

SCR’s large net asset value also benefits shareholders by removing the inevitable pressure that falls on management to make an acquisition once reserve life falls into the single digits.

Vertical integration that increases profitability. Heavy oil producers dilute their heavy crude by adding lighter condensate in order to transport via pipeline. SCR’s significant production and reserves of super-light condensate save it substantial sums on diluent costs while serving as a hedge to rising diluent costs. This puts the company at an advantage relative to heavy oil peers with high diluent costs.

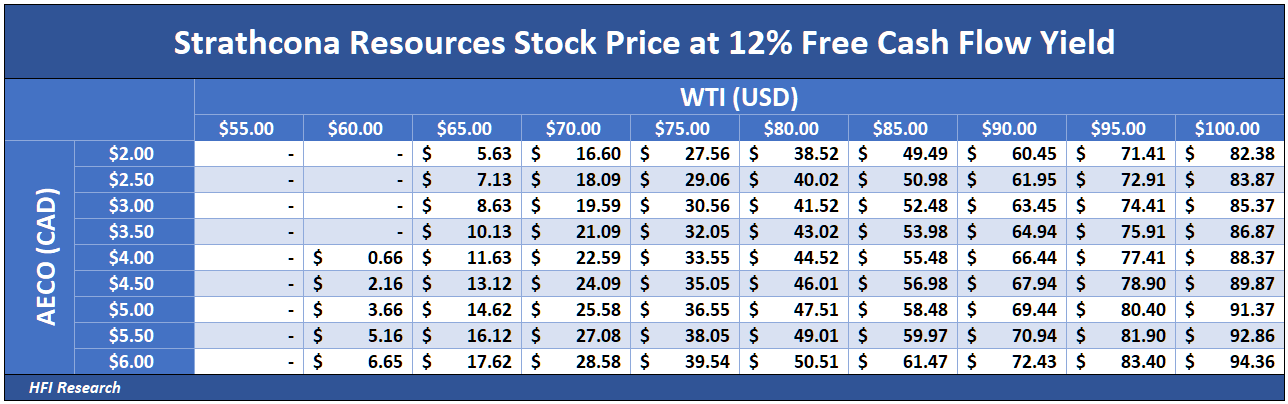

Free cash flow that grows significantly at higher oil prices. At $80 per barrel WTI and $2.25 AECO—around current prices—we estimate that SCR generates $4.71 per share of free cash flow, equivalent to a 13.7% free cash flow yield. At our full-year 2024 commodity price estimates of $87.50 per barrel WTI and $2.25 AECO, its free cash flow yield increases to 19.7%. If the shares were to trade at a 12% free cash flow yield, their price would rise by 63.9%, to $55.72. This is greater upside than either Cenovus Energy (CVE) or Suncor Energy (SU) have at the same commodity prices.

Our discounted cash flow valuation using 10% discount rate and assuming $87.50 per barrel WTI and $2.25 AECO implies the shares are worth $66.86 per share, representing 97% upside.

The table below shows our estimates of SCR’s share price if it traded at a 12% free cash flow yield amid different commodity prices.

The shares offer 100% upside at $92.50 per barrel WTI and $3.00 per mcf natural gas. SCR’s return profile at different commodity prices is shown below.

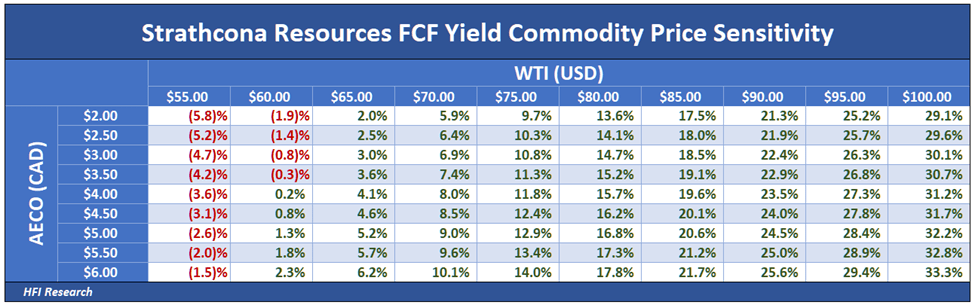

Once SCR hits management's debt target around mid-year, we expect the company to dividend out excess free cash flow. The following table shows SCR's free cash flow yield on the current share price at different commodity prices. Its prospective dividend yield quickly rises into the double digits at higher commodity prices.

The potential free cash flow payout amid higher commodity prices makes SCR an attractive equity alternative for income-seeking investors.

Risks are Low

Like any E&P, SCR shares entail risk, though they’re low in SCR’s case. The company’s cash flow breakeven at its 2024 capex rate is in the $60-to-$65 per barrel range, which is higher than its large E&P peers. However, approximately $500 million of SCR’s $1.3 billion capital budget is being allocated to growth projects. If oil prices decline and the company was to cut its growth capex to zero, its cash flow breakeven would fall to the mid-$50 per barrel range. Shareholder value would likely remain intact in such a scenario, though near-term growth prospects would diminish.

SCR plans to operate with $2.5 billion in debt, which we don’t believe puts shareholders at risk. An economic downturn that severely reduces oil prices could be a risk in the presence of debt, but all E&Ps would suffer in a low-price environment. We believe SCR would come through nearly any realistically conceivable oil market downturn with its value intact.

Another risk stems from the stock’s thin trading liquidity. Coupled with the large remaining number of former Pipestone shareholders who may look to sell their shares, the thin liquidity could cause SCR to underperform if oil market sentiment turns negative. However, the stock’s price behavior isn’t likely to impact the company’s value, so the shares would recover from a bout of underperformance, particularly if they traded at a discount to value as they do today.

Conclusion

We’re adding SCR to the top spot of our stable of attractive E&Ps. We’re long the name and could add to our position on a pullback. At current commodity prices, we estimate the shares are worth $41.50, so they offer 22.1% upside from today’s $34. And if oil prices rise over the coming months as we expect, the upside grows significantly. Investors should buy SCR shares now before oil market sentiment turns even more bullish.

Analyst's Disclosure: I/we have a beneficial long position in the shares of SCR.TO either through stock ownership, options, or other derivatives.

Confusing publishing today on old price of shares