Editor’s Note: This article was first published to HFI Research main subscribers on March 21, 2024. All market data used in this article will be dated as a result.

Summary

Permian Resources is one of the largest pure-play Permian E&Ps.

Its shares' attractiveness should be measured against our favorite independent Permian E&P, Diamondback Energy.

While PR shares can be attractive in their own right, they lose out to Diamondback on a relative basis.

Permian Resources (PR) is the successor entity to Centennial Resource Development. Centennial was founded in 2017 by Mark Papa, the former CEO of EOG (EOG). Papa was renowned for having executed a timely pivot away from pursuing natural gas leases and toward oil leases. In doing so, he established EOG as one of the premier shale E&Ps.

On September 1, 2022, Centennial closed on its acquisition of privately owned Colgate Energy Partners for $3.9 billion. The combined entity was renamed Permian Resources. To fund the acquisition, Centennial issued 269.3 million shares, paid $500 million in cash, and assumed $1.4 billion of Colgate’s debt. The deal roughly doubled PR’s operating footprint and production.

Then, on November 1, 2023, PR acquired Earthstone Energy in an all-stock deal valued at $4.5 billion. The deal made PR the largest pure-play E&P in the Delaware sub-basin of the Permian. The deal increased PR’s scale while its $175 million of synergies improved cash flow per boe.

At different times before 2020 we were owners of Centennial and Earthstone Energy shares. The former was built by a top-notch management team focused on aggressive, yet conservatively financed, growth with an eye toward capitalizing on higher oil prices over the long term.

The latter was founded by a team led by Frank Lodzinski, who had a proven track record of assembling assets during oil market downturns and selling to larger companies during upcycles.

The high-quality background of PR’s predecessors is important. We can say with confidence that the company was founded with a laser focus on attracting top-notch talent, owning high-quality assets, and operating with low costs. It’s no surprise that it has emerged as one of the main consolidators of the Permian.

PR’s efforts to consolidate the Delaware basin have continued even after its Earthstone purchase. The company acquired 14,000 net acres that were contiguous with its existing land position. It also sold legacy Earthstone’s Eagle Ford position, which had been producing 1,000 boe/d, for $67 million.

PR’s Attractive Land Position

Today, PR holds 400,000 net acres and 70,000 net royalty acres primarily in the Delaware sub-basin of the Permian. An overview is shown below.

Source: Permian Resources Q4 2023 Earnings Presentation, Feb. 28, 2024.

PR will focus development on the Delaware. In 2024, it plans to invest all its non-maintenance capex within the basin.

The question for PR investors is whether its stock is the most attractive Permian pure-play. In that comparison, it goes head to head against our current favorite, Diamondback Energy (FANG), which will be the largest Permian pure-play once Pioneer Natural Resources (PXD) is acquired by Exxon Mobil (XOM).

We found that despite PR’s attractiveness on an absolute basis, Diamondback’s exceptional performance in virtually every area makes its shares more attractive overall than PR’s.

The True “Low-Cost” Producer in the Permian

PR is fond of touting itself as a low-cost operator. While its costs are low for an independent shale E&P, all in all, they’re not quite on par with Diamondback.

PR’s “low-cost” claim holds for its operating costs. However, its cost leadership slips once corporate costs are included.

The company’s operating expenses totaled $9.38 per boe in the fourth quarter. We’ll assume operating costs remain flat after the Earthstone acquisition. In terms of operating costs alone, PR clearly runs the lower-cost operation, a desirable attribute in a commodity industry. Diamondback—no operational slouch in its own right—sports materially higher total operating costs that have averaged $11.60 per boe over the past few years.

Where PR loses out to Diamondback is in the corporate expense category. PR averages $6.00 per boe versus Diamondback’s ultra-low $2.75 per boe. Compared to Diamondback, PR has 50% higher cash G&A, nearly double the interest expense, and higher stock-based compensation than Diamondback on a per-unit basis.

PR’s elevated corporate costs actually reduce its netback to levels below that of Diamondback despite PR’s operating cost advantage.

Based on 2024 guidance, we expect PR to generate a corporate netback of approximately $27.80 per barrel exclusive of realized hedges, versus Diamondback’s $34.50. If Diamondback acquired PR, it could eliminate roughly 80% of PR’s higher-cost corporate expenses while reducing its average operating expenses in the near term, at least.

PR has not yet reported a full quarter of results after combining with Earthstone, so G&A may come down on a per-unit basis. Corporate costs will also come down as debt gets paid down. Even so, we don’t expect PR’s netback to exceed Diamondback’s over the long term.

PR’s Higher Leverage

PR’s debt is on the high side. Its operating cash flow is approximately 3.2-times operating cash flow at $82.50 WTI and $2.25 natural gas. By contrast, Diamondback’s debt is slightly more than one-time operating cash flow at the same commodity prices, even after accounting for its acquisition of Endeavor Energy Resources.

PR’s debt maturiries are spread over the next few years. On March 6, PR redeemed its 6.875% Senior Notes Due 2027. We don’t expect PR to have any problem refinancing debt when it comes due. Its debt maturities are shown in the table below.

Source: Permian Resources 2023 10-K.

PR’s $170 million of 3.25% notes due 2028 are convertible into common shares. Since the conversion price is around $6 per share, we assume the notes will be converted to shares rather than redeemed. Management has not publicly disclosed any plans with regard to the convertible notes.

PR’s debt situation requires that it hedge its production to ensure it can service its debt. For 2024, approximately 25% of PR’s oil production is hedged in the mid-$70s per barrel. The company’s hedges will protect its cash flow during an oil market downturn, though they will also limit its upside torque to higher oil prices. Until debt is paid down to conservative levels, PR will have to hedge a significant portion of its production.

Diamondback, meanwhile, maintains exposure to higher oil prices than PR because it is less hedged.

The Primary Risk to PR Shareholders

All shale E&Ps are at risk of an increasing proportion of gas in their production mix. Gassier production means more “dry” natural gas and NGLs, both of which fetch a significantly lower price than crude oil.

Even high-quality shale E&Ps aren’t exempt from gassier production over time. For example, the mighty EOG signaled in its fourth-quarter earnings conference call that it was increasing drilling activity in areas like its “Combo” play, which has higher NGL weighting than its legacy oil production.

In 2023, PR realized an average price per barrel of $22.83 for its NGLs versus $78.85 for its crude. Its crude price realization was just shy of the WTI benchmark, which averaged $77.62 per barrel. The company realized only $1.60 per mcf on its 2023 natural gas production versus the average Henry Hub benchmark price of $2.70.

If PR’s production grows gassier, it will struggle to grow free cash flow unless total production growth can outpace its increasing gas-to-oil ratio.

Like most of its peers, PR is more likely to maintain flat production than grow production so as to maximize free cash flow generation, pay down debt, and distribute capital to shareholders. Longer term, in the absence of significant production growth, PR’s free cash flow and share price could be at the mercy of natural gas prices unless demand for Permian natural gas and egress options allow for higher natural gas prices, which we consider unlikely over the long term.

Recent trends for PR’s production mix aren’t encouraging. The following chart depicts the mix over the past eight quarters. It shows the migration away from legacy Centennial’s high-quality oil-weighted acreage after subsequent acquisitions as PR. We suspect it also reflects gassier organic production, though to a lesser extent.

In the fourth quarter, which included two months of Earthstone operations, crude oil represented 48% of PR’s total production. For 2024, management is guiding to 47% crude oil, continuing the unfavorable trend toward greater NGLs and natural gas production at the expense of crude oil production. PR’s natural gas production will be around 31%, and its NGLs will comprise 21% of total production on a per-boe basis.

Cash Flow Sensitivity & Valuation

Turning PR’s stock price to intrinsic value per share versus Diamondback, consider that despite PR’s higher debt balance, greater risk, lower gross margin, shorter reserve life, and lack of long-term track record as a combined entity, its shares trade at a price that yields 9.33% assuming full dilution of the convertibles. Diamondback’s stock yields around 10%, even after its recent run-up from $160 to $190 per share. At current prices, Diamondback’s stock is clearly more attractively priced.

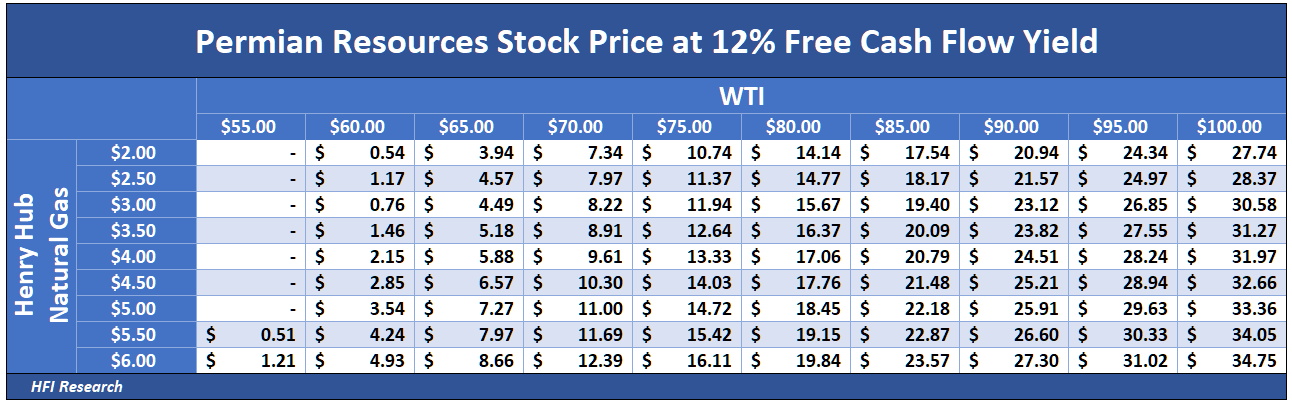

However, PR’s lower gross margins and higher corporate expenses relative to Diamondback give it an edge in terms of upside cash flow torque to higher commodity prices. The following table shows PR’s stock price at different commodity prices assuming it trades at a 12% free cash flow yield, which, we should add, is greater than its current free cash flow yield.

The next table illustrates the implied upside from PR’s current $16.30 stock price.

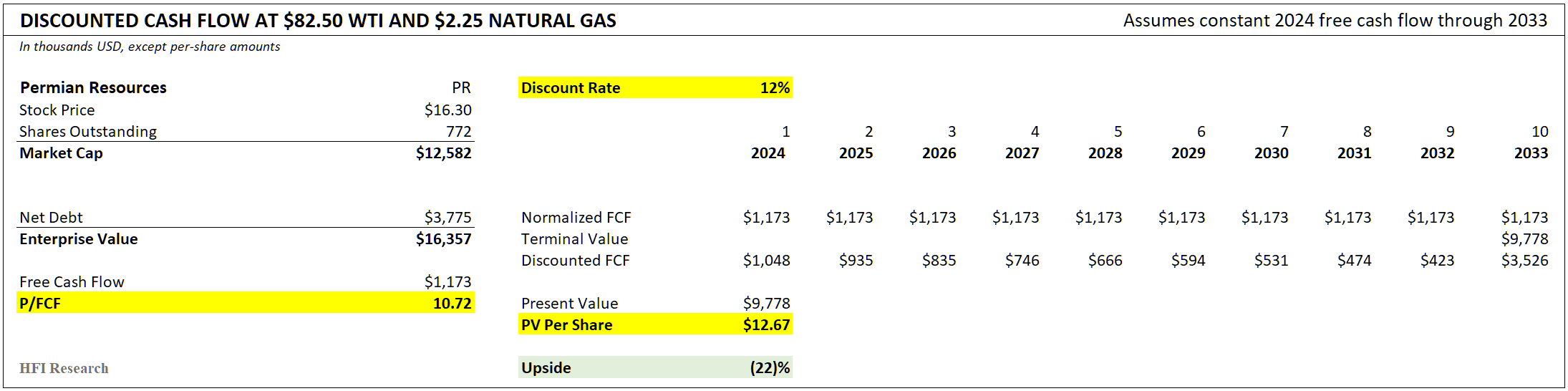

If we discount PR’s free cash flow by 12% annually over the next ten years, PR shares imply 22% downside from their current price.

Diamondback’s shares trade more closely in line with fair value.

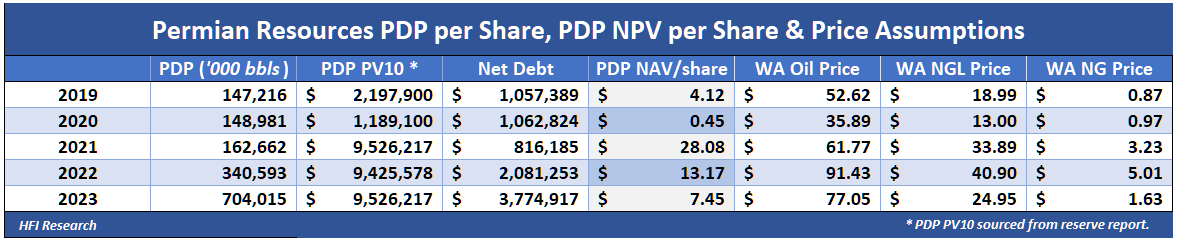

PR’s net asset value per share took a beating after the significant share issuance that funded its Earthstone acquisition. NAV per share will improve as the company pays down its debt over the coming quarters.

Diamondback also wins out in the return-of-capital category. Its base dividend yields 1.9% on its current stock price, higher than PR’s 1.2% yield. Diamondback also enjoys the distinction of having grown its base dividend at a 39% compound annual growth rate since 2018.

Diamondback reverted from 75% to 50% free cash flow return to shareholders after it acquired Endeavor Energy Resources in February. As a result, it’s less likely to increase its base dividend in the near term.

PR has returned significant capital to shareholders after its Earthstone deal closed. On March 4, it announced a secondary sale of 48.5 million shares of common stock in connection with certain shareholders opting to exit their stake after the Earthstone transaction. In the transaction, PR purchased 2 million shares at the offering price of $15.76 per share.

We also expect PR to increase its annual base dividend from $0.20 to $0.24 later this year. After the increase, we expect PR to focus free cash flow on debt reduction over dividend increases.

Looking out beyond 2024, we expect Diamondback to deleverage and reach management’s balance sheet target more rapidly than PR. When it does, it is likely to go back to paying out 75% of free cash flow to shareholders.

Conclusion

Over its entire life as a public company, Diamondback has excelled in capital allocation, and we don’t expect that to change. We expect it to distribute more capital on a percentage per share basis to its shareholders owing to its stronger balance sheet and greater cash flow torque to higher oil prices. Overall, we have greater confidence in Diamondback management’s ability to take capital allocation action to extend its reserves than we do for PR.

Longer-term, Diamondback’s proved reserve life extends several years longer than PR’s, which is approximately ten years. The longer runway should stave off the onset of a materially higher gas-to-oil ratio, which reduces risk for its shareholders.

For these reasons, we're more comfortable investing in Diamondback for the long term.

That said, we don't view PR as a low-quality E&P. It only loses out in comparison with Diamondback, which is arguably the highest-quality independent shale E&P in North America. If PR can successfully deleverage and improve the prospects for its net asset value and free cash flow on a per-share basis—particularly at higher commodity prices—then its stock will be worth considering. Until then, we’d stick with Diamondback as our preferred long-term E&P holding.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

Any updated thoughts now on PR? Thanks