Note: This article was first published to HFI Research’s main subscribers on March 28, 2024. Please note that some of the market data used in this article will be dated.

There’s a lot to like about Parex Resources (PXT:CA) (OTCPK:PARXF). The company produces consistently good results. It possesses high-quality assets that have significant exploration upside. It’s likely to grow production over the coming years. Its balance sheet consistently boasts a net cash position. It also benefits from attractive product pricing.

So far, so good.

But here’s the rub: while PXT is domiciled in Canada, it operates in Colombia. We have experience investing in Colombia, namely in Gran Tierra (GTE:CA) before the 2020 downturn. The risks from operating in Colombia stem from two sources: shifting tax regimes and transportation disruptions, both of which pose clear and present danger to the company and its shareholders. Both of which also can surface with little warning.

Whether an investor chooses to buy PXT shares depends on their attitude toward the risks of doing business in Colombia’s oil and gas sector. If an investor can gain comfort with regard to the risks pertaining to asset seizures, tax regime changes, and the nation’s court system, PXT shares can be an attractive compliment to a North American-weighted energy portfolio.

PXT shares have been clobbered year-to-date on a relative basis. The shares are underperforming the broad Canadian energy index ETF (XEG) by 30.4% YTD.

As extreme as PXT’s underperformance has been, Colombia-related risks make the shares fairly valued at the moment. However, they could become attractive if they trade lower or if developments in Colombia take a positive turn for the company.

PXT’s Many Positives

PXT boasts a massive acreage position that spans some 5.2 million acres in Colombia. Granted, its leases involve greater risks and hurdles to development than PXT’s North American counterparts. Nevertheless, its land holdings possess significant value. The company considers its untapped exploration to be a cornerstone of its long-term investment prospects and intrinsic value, though any exploration upside isn’t reflected in PXT’s current stock price.

The company’s production averages more than 97% crude oil, one of the highest among North American-domiciled E&Ps. Even the highest-quality Canadian E&Ps have a production mix that includes at least 20% lower-value natural gas. PXT’s mix is highly attractive by comparison.

PXT’s financials are some of the strongest among Canadian E&Ps. It generates attractive cash margins. At $87.50 per barrel WTI, PXT’s corporate netback is $34 per boe.

The company operates with a conservative balance sheet. It maintains a large net cash position and has paid out all its free cash flow through dividends and share repurchases. PXT’s conservative balance sheet allows it to operate without hedges, so shareholders can fully participate in oil price upside.

PXT’s capital allocation over the past eight quarters is shown below.

PXT also generates a consistently high return on capital employed, which has averaged 35% over the past three years, including a high of 48% in 2022 and a low of 23% last year. Even the 2023 return on capital employed puts PXT near the top of its Canadian E&P peers. The high returns translate into robust long-term cash flow generation for shareholders.

The company receives Brent crude oil pricing and regional South American natural gas pricing, both of which trade at a premium to North American prices. The relatively high realized prices bolster PXT’s netback relative to its North American peers in a sustained manner.

Management has a strong track record of achieving growth through exploration, as shown by the following chart from PXT’s investor presentation.

Source: Parex Resources February 2024 Investor Presentation.

Equally important for shareholders, management has successfully converted growth into increasing value per share. Through regular programmatic repurchases, PXT has reduced its shares outstanding by 36% since 2018, as shown in the chart below.

Source: Parex Resources February 2024 Investor Presentation.

This is exactly the kind of capital allocation E&P shareholders want to see when the company is growing production, when it possesses significant growth prospects, and when its shares trade below intrinsic value.

In 2024, we estimate that PXT will generate approximately $710 million of funds from operations at $87.50 per barrel WTI. It plans to spend $410 million of capex and pay out $115 million as a base dividend. We expect management to allocate the remaining $185 million to share repurchases. With PXT shares trading at $21.30, this sum represents 8.4% of PXT’s current enterprise value. This amount would be repurchased while investors who buy at current prices also enjoy a low-risk and stable 7% dividend yield.

Investors can use PXT shares to diversify their North American E&P exposure. The risks to North American oil and gas production may not be front-and-center for many domestic investors, but they’re significant when looking out over a period of years.

For oil, North American producers face the risk that WTI production growth crowds out heavier global crude oil grades. If WTI production grows until it reaches the maximum processing capacity for light-oil refiners, WTI’s discount to heavier grades could grow materially larger, which would hold the cash flow generated by North American E&Ps, as well as their share prices.

On the natural gas front, if the gas produced as a byproduct of crude oil production increases to levels that keep North America glutted with gas, continued low North American gas prices would wreak significant damage to E&P cash flow and share prices.

In a portfolio heavily weighted toward North American E&Ps, investors can escape these risks by holding PXT shares, which are not subject to these risks. In fact, producers of heavier oil grades like PXT would benefit in scenarios that are bearish for North American producers.

PXT’s Significant Risks

Colombian E&Ps face the risk of domestic social unrest that impacts infrastructure. Gran Tierra would encounter transportation blockages and would transport its production by truck when pipeline infrastructure wasn’t available. PXT’s production is spread throughout the country and could face similar risks.

Even greater risk stems from PXT’s tax situation. While tax pools shield PXT’s income from taxation in Canada, its tax status in Colombia is another matter entirely.

Colombia’s president, Gustavo Petro—an avowed leftist—took office on August 7, 2022. Petro campaigned to end domestic oil and gas exploration, ban hydraulic fracturing, and end the employment of foreign contractors in Colombia’s oil and gas industry.

In November 2022, the Colombian government passed a law that increased the maximum surtax on oil and gas company income. The law went into effect in 2023. It imposes a surtax equal to 5%, 10%, and 15% of income when Brent oil prices trade at or above $68.58, $76.03, and $81.27 per barrel, respectively.

The law also disallowed the deduction of royalty payments in how taxable income is calculated for oil and gas companies. As such, it would increase PXT’s taxable income by the amount it paid in royalties, which ranged from 16.5% to 23.0% over the past eight quarters, as shown below.

The inclusion of royalties into taxable income threatens to increase PXT’s effective tax rate by approximately 4%.

However, Colombia’s Constitutional Court overturned the tax reform. The court’s ruling is now being appealed. A ruling is expected in the next few months.

At the moment, PXT assumes that the appeal will fail and that the Constitutional Court will uphold the deductibility of royalties in calculating the company’s 2023 taxes.

If PXT is wrong and the government wins its appeal, the company would have to make additional payments toward its 2023 taxes. Future net income available to shareholders would also be lower than PXT’s management currently assumes in its forecasts and presentations.

We don’t have an opinion on the outcome of the case.

We do have conviction that these latest tax issues won’t be the last for Colombian oil and gas producers. The Petro administration is openly hostile toward oil and gas companies. Going forward, PXT will remain at risk of adverse tax changes that its shareholders would consider arbitrary and capricious. Such changes are a fact of life in Colombia, and at times they’re unforeseeable. Any PXT shareholder must manage their position with care to account for this ever-present unknown.

While the future may look bleak when it comes to E&P taxation in Colombia, there are economic realities at play that augur for tax leniency toward Colombian oil and gas producers. Their consequences to Colombia’s tax base could end up tipping balance in favor of E&Ps when it comes to the taxes they pay.

The fact of the matter is that Colombia’s national oil reserves are depleting at a rapid rate. Without significant investment in oil and gas production, Colombia could find itself without a domestic oil and gas industry in fifteen years. Exxon Mobil (XOM) underscored the risks to Colombia’s oil and gas industry after it pulled out of the country in the wake of Petro’s election.

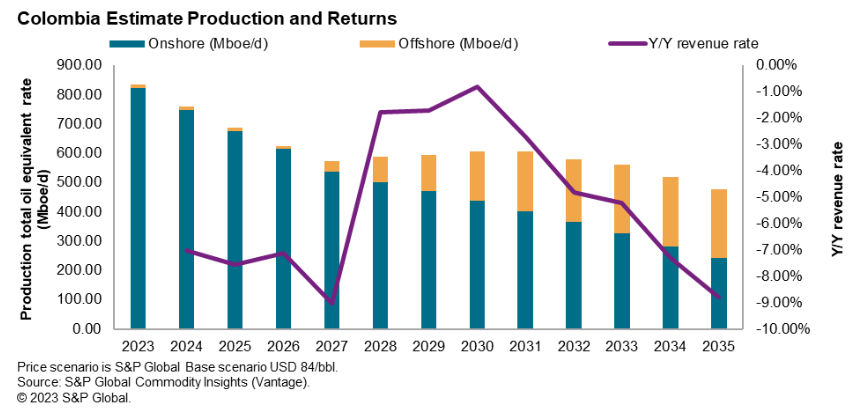

In addition to reserve depletion, Colombia faces declining oil and gas production over the coming years, particularly in its onshore production. Lower production will decrease the income derived from taxing E&Ps such as PXT. The situation is shown by the declining bars in the chart below.

Source: S&P Global Platts, Dec. 11, 2023.

Lower oil and gas production will strain Colombia’s budget. It risks exacerbating inflation and necessitating increases in LNG imports to meet domestic energy needs.

These realities provide an incentive to Colombia’s government to reduce tax rates on oil and gas producers. If it did so, it could increase the country’s oil and gas production and reserve growth prospects while simultaneously raising more income for the national government.

In a scenario that features lower E&P taxation, PXT shares would likely soar due to the positive free cash flow impact for shareholders.

We have no opinion on the future course of Colombia’s taxation and politics. We simply present the facts and assume the future will remain volatile, at least until a new political party gains power.

Commodity Price Sensitivity and Valuation

Over the next three years, PXT plans to grow its production by 5% per year. If we assume its exploration efforts over that timeframe are successful and that they enable PXT to grow production by 5% annually over the next five years with 2024 levels of capex, the company would generate $1.54 billion of free cash flow, pay $575 million in dividends, and repurchase $968 million of shares.

Converting these figures to per-share amounts at today’s share count results in $14.84 per share of free cash flow, $5.53 per share in dividends, and $9.32 per share of repurchases. Altogether, this amount is equivalent to 70% of PXT’s current enterprise value per share. This capital distribution profile puts PXT near the top for all Canadian E&Ps over the coming years.

PXT shares currently trade at an 8.0% free cash flow yield assuming the current $80 per barrel WTI and $2.25 Henry Hub natural gas. The free cash flow yield increases to 11.3% at $87.50 per barrel WTI.

Calculating PXT’s free cash flow yield is complicated by the fact that the tax regime has a significant impact on free cash flow.

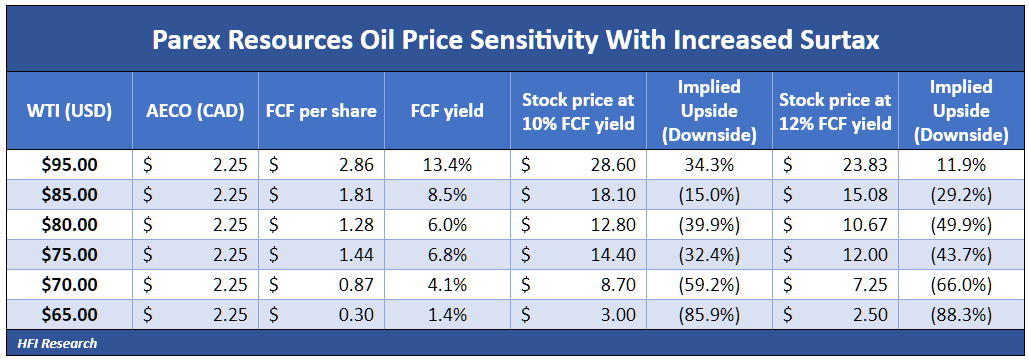

The following table shows our estimates of PXT’s free cash flow sensitivity assuming the new surtax law is overturned by Colombia’s Constitutional Court, and that lower tax rates apply instead. PXT’s own financial disclosures make this assumption. It shows that PXT shares currently discount WTI of slightly less than $85 per barrel, assuming they trade at a 12% free cash flow yield.

The next table assumes that the higher tax rates are imposed. PXT shares appear overvalued in such a scenario. If the new rates go into effect, PXT shares could decline by more than 17% to trade at the same 8.0% yield at which they trade today.

However, one-third of PXT’s capex is aimed at exploration. This capex is more discretionary and is not necessary for maintaining flat production. If we reduce capex by the exploration component, PXT shares look more attractive, even if we account for the new surtax regime.

These valuations imply that PXT’s current share price assumes some capex is discretionary, as it should. The valuations indicate that if the higher tax regime doesn’t go into effect, PXT shares are significantly undervalued when the free cash flow calculation only subtracts maintenance capex from operating cash flow.

This valuation implies that management should allocate free cash flow aggressively toward share repurchases.

If we assume only maintenance capex and no exploration capex, PXT’s shares yield 13.5% at $80.00 per barrel WTI and 17.4% at $87.50 per barrel WTI. As such, their value is roughly in line with Canadian peers from the perspective of free cash flow yield.

Our valuations do not incorporate discounts to reflect the operational or financial risks involved in operating in Colombia.

Turning to reserves, PXT’s management has successfully increased net asset value per share based on PDP over the past five years through successful exploration efforts, a conservative balance sheet that features a net cash position, and by repurchasing shares.

Net asset value per share based on proved reserves exceeds PXT’s enterprise value.

Its shares possess 64.6% upside to trade at proved reserve value at $87.50 WTI. The main takeaway from these figures is that PXT’s stock currently reflects none of its vast exploration potential.

Conclusion

PXT shareholders have a lot riding on the outcome of Colombia’s tax law. If the government wins its appeal and PXT cannot deduct royalty payments from taxable income, its shares could sell off and trade lower over a sustained period. Production growth and share repurchases would offset the impact, but only partially. Amid an adverse tax ruling, PXT would need a change in government or significant exploration success to boost its shares’ prospects over the next few years.

In light of the risks involved, we recommend taking a cautious approach to PXT. The shares are conservative and undervalued in the absence of Colombia-related risks. But the Colombia-related risks are real, albeit unquantifiable.

A small position in PXT may be appropriate, but we wouldn’t concentrate heavily in these shares. After all, there are plenty of other opportunities currently available among North American E&Ps. We believe PXT shares are best used as a diversification tool for portfolios heavily weighted in North American E&Ps.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

Hi HFIR, question about PXT's reserve life. I read on other sources that PXT's reserve life is rapidly dwindling as the company has not been able to extend its reserve life due to drilling limitations in Columbia. Last I checked, their reserve life was well below 10 years based on their current drilling rates. Have you taken this into consideration as well beyond just the PDP value?

Thanks!