Wilson’s Thoughts: Whitecap is known to be one of the best oil operators in Canada. This acquisition gives Whitecap’s team a depth of inventory to execute for 2+ decades. If shareholders can overlook the short-term market volatility, I am a fan of this deal for the long term. While I agree with Jon’s analysis that Veren on a standalone provided more upside, you have to tip your hats off to the Whitecap team for pulling this off especially given the difference in trading multiple.

We also decided to make this article public. As always, thank you for reading.

By: Jon Costello

This morning, Whitecap Resources (WCP:CA) announced that it would acquire Veren (VRN) in an all-stock deal in which VRN shareholders will receive 1.05 shares of WCP. VRN shares ended the day 16.0% higher, while WCP shares sold off by 14.6%.

We’ve held VRN since October 31 of last year. I purchased the shares for the HFIR Energy Income Portfolio at an average price of $4.97, so the deal provides us with a return of ~14.69%.

But the timing of this deal is fortunate as it allows us to reinvest our VRN shares in other beaten-down stocks, with energy being our preferred alternative given the sector’s ridiculously underpriced equities vis-à-vis our longer-term oil and natural gas price outlooks.

Why I’m Not a Fan of This Deal

Despite the immediate benefits to our portfolio and investment returns, I’m not a big fan of this deal.

For one, it significantly undervalues VRN. This deal will reduce the long-term return prospects for VRN shareholders considerably, which is frustrating for investors who understand the economics resulting from VRN’s longer-term production growth.

The valuation discrepancy between the two is wide. As of Friday’s close, WCP traded at a multiple of 3.8-times EV to 2024 cash flow. As of today’s close, VRN trades at a far lower multiple of 2.6-times.

The deal’s timing is also frustrating for VRN shareholders. Management is no doubt aware that its reputation had been tarnished by the operating mishaps it committed last October. But its reputation was on the mend. Successful drilling results over the past few months demonstrated that the operational failure was attributable to management’s choice of completion methods and not to the company’s geology, as many had feared. Management was well on its way to proving that it was a strong operator.

But the job wasn’t done.

VRN’s stock price would have been the ultimate barometer of investor perceptions of the company’s management. I believe its continued successful execution over the next few quarters would have sent VRN shares comfortably above $6.00 at $70 per barrel WTI. VRN’s board and management should have held off in considering a sale until the shares traded at a higher price or management’s reputation was rehabilitated. After all, it doesn't appear that VRN’s board was under external pressure to sell. Nevertheless, they decided to sell the company while its shares were depressed by a reputational discount.

Various E&P commentators have suggested that the two companies tie up. I had been of the view that VRN’s management wouldn’t sell to WCP in an all-stock deal due to the valuation disparity between the two and the likelihood that WCP management would not want to pay up to acquire VRN. Clearly, I was wrong. WCP did manage to acquire VRN in an all-stock deal, though WCP’s management didn’t pay up for VRN’s assets.

Long-Term VRN Shareholders are Not Better Off

The deal will significantly reduce the long-term upside potential that VRN shareholders stood to realize if VRN remained a standalone entity. VRN’s operating and financial leverage, as well as its high percentage of crude oil production relative to WCP, provided it with superior cash flow torque to oil prices. Its increasing cash flow amid higher oil prices would have driven its shares significantly higher.

Moreover, VRN was slated to grow its production from today’s 192,000 boe/d to 250,000 boe/d in 2029. While VRN would spend significantly more than WCP on capex to accommodate this growth, its capex requirements were poised to decrease and level off after a few years.

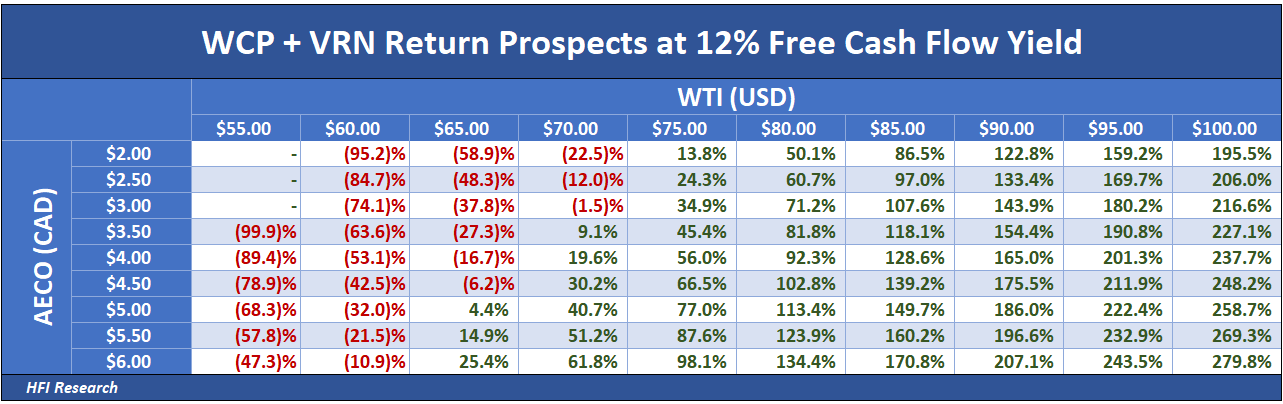

These factors would have increased VRN’s cash flow torque to higher oil prices well above my estimates below of VRN as a standalone entity, which are based on the company’s current production rate. My return estimates from VRN's closing price today are shown below.

WCP has far lower upside. WCP has less cash flow torque and has less growth planned. WCP’s five-year plan called for 5% average annual growth from today's 177,000 boe/d to 215,000 boe/d.

The combined entity will have improved growth prospects relative to standalone WCP but reduced growth prospects relative to standalone VRN. The combined entity’s cash flow sensitivity to commodity prices will look like the following.

Not bad, but not as strong as VRN would have been as a standalone entity.

Investors seeking to maximize long-term upside amid sustained higher oil prices may want to consider switching out of WCP/VRN—which will be weighted 65%-to-35% liquids to natural gas—and into either Strathcona Resources (SCR:CA), MEG Energy (MEG:CA), or the beleaguered Cenovus Energy (CVE:CA). From today’s prices, these alternatives offer long-term return prospects that are as good or better than WCP/VRN in an oil bull market.

What VRN Brings to the Table

VRN and WCP share similar financial profiles when considering netbacks per Boe. VRN’s operating expenses were similar to WCP’s at around $13.75 per boe. VRN’s royalties were lower than WCP’s, and its income is shielded by a $900 million Canadian net operating loss carryforward. It also had lower marketing expenses. WCP, by contrast, had lower G&A and transportation expenses.

The combined entity will achieve significant operating and financial synergies. Operating synergies will be driven by the overlapping nature of the two companies’ Montney and Saskatchewan acreage. Financially, net debt to funds flow will be 0.9-times, lower than VRN’s pre-deal ratio of 1.1-time.

WCP will continue to pay its $0.73 per share dividend after the deal. At $70 per barrel WTI, the combined entity will cover its dividend 130%, less than VRN’s pre-deal dividend coverage of approximately 200%.

VRN Shares are Now a Hold

Aside from portfolio management-related pruning, I plan on holding VRN shares, at least for the time being. WCP will do well over the long term. The company will be a large dividend payer, with dividend hikes and special dividends likely amid sustained high commodity prices.

As a light oil producer, the combined entity will be a go-to name for U.S. investors as they begin to appreciate the ramifications of declining shale oil production. The combined entity’s larger scale will also enable it to secure attractive natural gas marketing opportunities that feature improved price realizations versus Montney and Duvernay in-basin pricing.

Over the longer term, WCP’s management is clearly the best choice for operating VRN’s assets. WCP’s management has one of the best operating track records in North America.

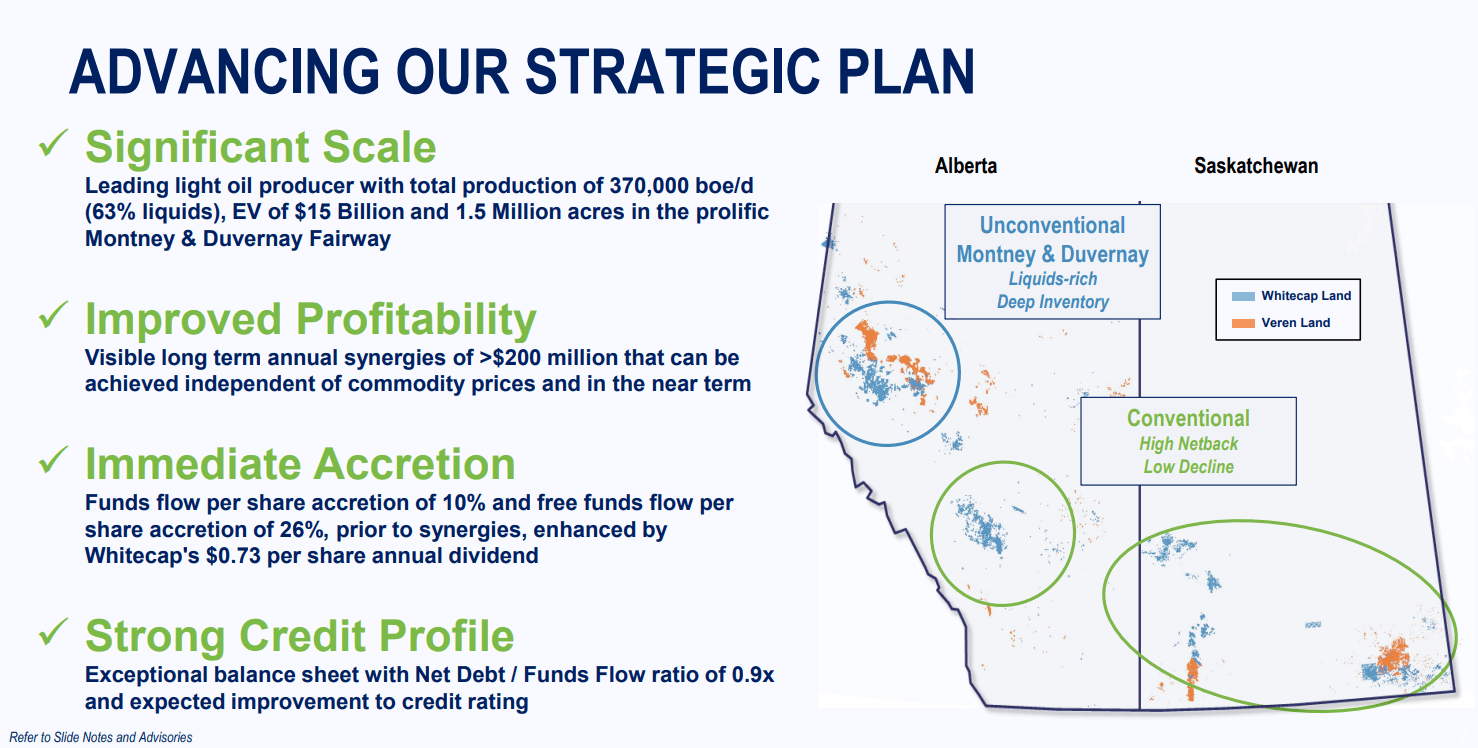

The operational fit between the two is a no-brainer, as this slide from WCP’s merger presentation demonstrates.

Source: Whitecap Resources, “Strategic Combination with Veren,” slide presentation, March 10, 2025.

WCP will emerge from the deal with improved oil-weighing in the Alberta Montney and a new attractive footprint in the Duvernay. VRN has been drilling some of the best wells in the Montney, and WCP’s shareholders will benefit from the company’s deep inventory of oily acreage.

A Competing Bid is Unlikely

Given how cheap VRN shares are—even after this deal announcement—VRN shareholders may hope for a competing bid. However, I expect this deal to go through. There are simply too few potential buyers with sufficient scale to consider a competing bid.

WCP management should get credit for the strategic timing of this purchase. It is pursuing the deal when its shares have held up better than its peers, giving it a better platform to go on offense during this downturn.

I’d speculate that Strathcona (SCR:CA) would prefer to remain focused on high-return condensate and heavy oil assets rather than expanding into Montney and Duvernay light oil. The other large oil sands players are also likely to confine their operational focus to bitumen and SAGD assets.

VRN’s assets don’t share strong synergies with those of Canadian Natural Resources (CNQ). ARC Resources (ARX:CA) is one of the only Canadian light oil producers with land and economics that are arguably superior to VRN's. ARX would probably consider a VRN acquisition to be dilutive of the quality of its business.

Outside of these names, Canadian E&Ps are too small to take a run at VRN. U.S. E&Ps are more likely to be acquirers as long as they trade at a premium to their Canadian peers and recognize that their days of doing so are numbered as their drilling inventory gets whittled down. Apparently, for the second point, we aren't quite there yet.

Conclusion

This wasn’t the result I was hoping for when I bought VRN shares. Fortunately, however, it occurred during a time when the Canadian oil patch trades at a massive discount to intrinsic value. I may ultimately decide to switch out of VRN if something else is more attractive, particularly if other high-quality E&Ps underperform WCP/VRN from here. As always, I’ll be sure to update subscribers if and when I do.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of ARX:CA, CVE, SCR:CA, VRN either through stock ownership, options, or other derivatives.