Editor’s Note: This article was first published to subscribers on July 2nd, 2025. Since then, HCC shares have appreciated 32.75%. All market information in the article is not updated. The original article is below.

By: Jon Costello

Metallurgical coal represents one of the most attractive long-term investment opportunities in the energy sector. I recently discussed the commodity’s long-term outlook here.

The constructive macro backdrop begs the question of how best to profit from higher coal prices, which I believe will prevail over the coming years.

The opportunities in the stock market have arisen in large part due to the negative public opinion toward coal, which has kept investors from buying coal names. This opinion is misguided.

Thermal coal will continue to be used to generate electricity. It will play a vital role in meeting the world’s growing electricity demand. Having coal as part of the energy mix increases a grid’s reliability and resiliency while reducing its cost in a manner that other energy sources cannot.

For met coal, there is no replacement for steel as the main structural component in buildings, infrastructure, automobiles, and other goods that make civilization possible.

To be sure, the pollution from burning coal is a problem that needs to be addressed. But calls for phasing out the industry entirely are misguided. Moreover, in light of the central role coal plays in sustaining modern life, its negatives should be regarded as manageable tradeoffs against the commodity’s virtues, rather than serving as a pretext for eliminating the commodity’s use entirely.

Investors who are comfortable with the prospect of coal remaining a viable energy source and input into steelmaking for decades to come can take advantage of the depressed valuations of coal stocks. The opportunity arises from three key factors: first, the discounted purchase price that an investor can obtain; second, the attractive business model possessed by certain met coal producers; and third, the long-term compounding nature of returns offered by the best-positioned met coal producers.

If I had to make one investment before being whisked away to a remote island with no internet access, it would be Warrior Met Coal (HCC). The risk/reward proposition it offers represents one of the best long-term investments in the energy space.

Warrior’s Assets

Warrior operates two large coal mines located in the Warrior Basin in Alabama. The company is also nearing the completion of a third mine in the same basin.

Warrior’s world-class economics are in large part attributable to its uniform, continuous coal seams for which the Warrior Basin is known. These geological features allow for consistently high-quality, low-cost coal production.

Warrior operates three coal mines. Its “Mine 7” produces premium Low-Vol met coal that can be sold for little to no discount from regional benchmark prices. “Vol” refers to the “volatile matter content,” or the gases other than carbon released during the coal’s combustion. Low Vol met coal is considered higher quality due to its greater carbon content. Low Vol coal produces more coke per ton of coal.

Mine 7 has capacity of 5.6 million short tons per year, which is equivalent to 5.1 million metric tons per year. The mine has a remaining life of 20 years.

Warrior’s “Mine 4” is an underground single longwall system that produces premium, High Vol A (HVA) met coal. The mine has a 35-year reserve life. The premium quality of the coal it produces receives a premium price to regional benchmarks. The mine’s capacity is 2.4 million short tons per year or 2.2 million metric tons per year.

Together, these two mines enable Warrior to produce one of the highest-quality product mixes of met coal in the U.S. Nearly all of its production is sold in seaborne markets.

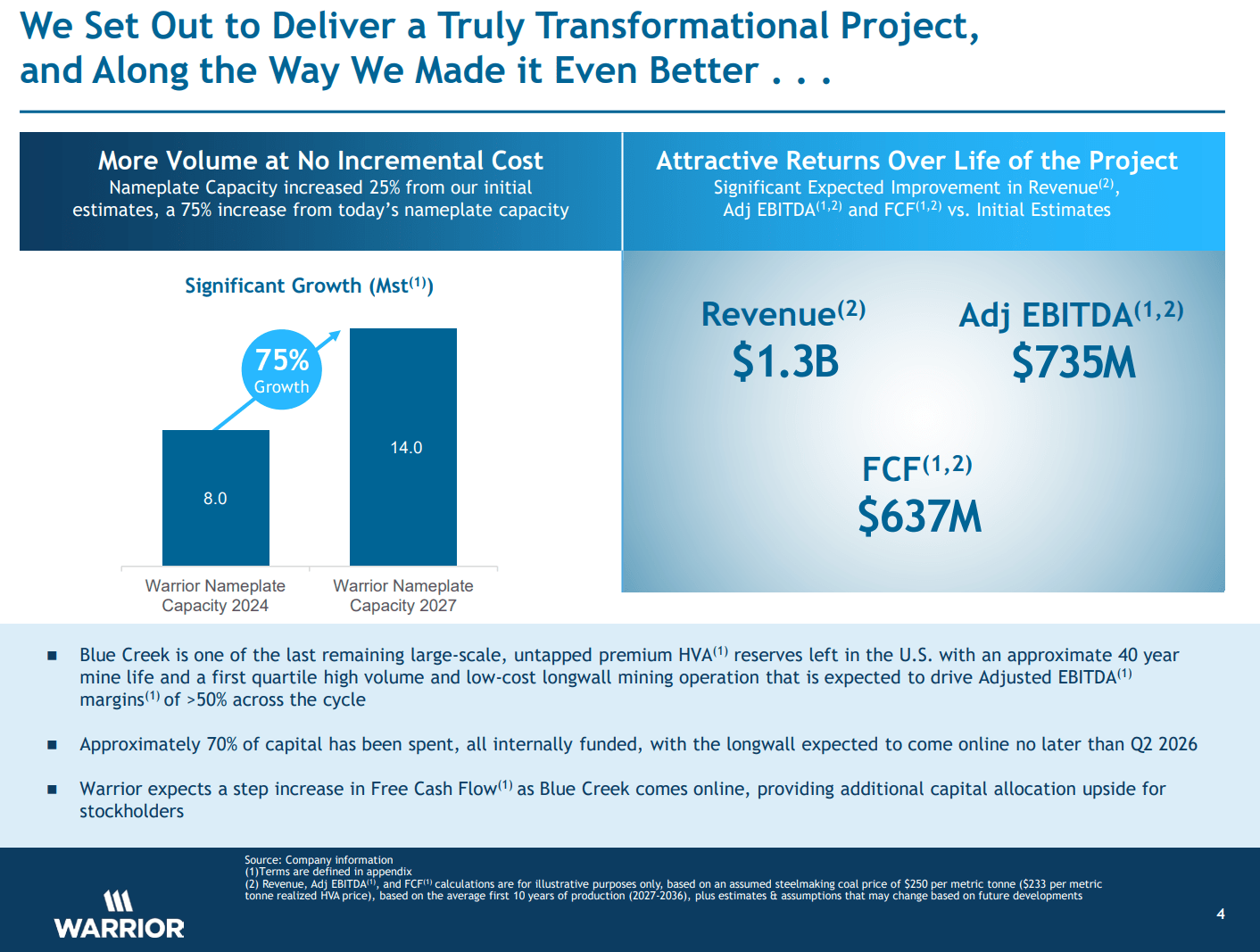

The company’s third mine, called Blue Creek, is under development. The company provides the following project overview.

Source: Warrior Met Coal Blue Creek Project Presentation, Feb. 21, 2025.

Blue Creek will have a 40-year reserve life. Like Mine 4, Blue Creek’s coal production is of the premium HVA variety. Its coal is produced from one of the last remaining HVA reserves in the U.S.

Also like Mine 4, Blue Creek’s is a longwall mine. There are several methods used to produce coal, such as room and pillar mining, bord and pillar mining, and high-wall mining in underground operations, as well as various methods of surface mining. Longwall mining is the most efficient method for the large-scale production of underground coal reserves. The method features relatively high productivity, low labor intensity, and consistent recovery rates. These advantages translate into lower operating costs per ton and improved economies of scale.

The downside of longwall mining is the large upfront cost involved in mine development. Warrior has financed Blue Creek’s development without external financing, so the project’s large capital costs might be thought to be financially burdensome for the company. However, given Blue Creek’s expected annual incremental free cash flow contribution of approximately $550 million at a PLV price per ton of $225, the project’s expected total $1.1 billion cost represents an attractive use of shareholder capital.

Furthermore, Warrior has kept a strong financial profile throughout Blue Creek’s development. The company has maintained a net cash position since commencing development in February 2020. As of March 31, 2025, Warrior’s $154 million of long-term debt was offset by $455 million of cash and $33 million of short-term investments.

Blue Creek is expected to begin commercial production by mid-2026. Once fully ramped, it will increase Warrior’s production capacity from its current 8.0 million short tons per year annual capacity to 14.0 million short tons per year, a 75% increase. The expansion’s capacity is equivalent to 12.7 million metric tons per year.

Blue Creek’s significant size relative to Warrior’s existing assets and its low cost of production relative to its two existing mines will materially reduce Warrior’s cost of production once the mine begins to ramp up production next year. The addition of Blue Creek will lower Warrior’s already low cost of production and significantly increase its free cash flow generation capacity.

Importantly for Warrior’s shareholders, Blue Creek has been financially de-risked. The project has approximately $250 million of remaining development costs. Warrior’s $334 million in net cash is more than sufficient to complete the project. To date, management’s execution in developing the project has been stellar. While its overall cost has risen relative to management’s initial expectation of $550 to $600 million, costs increased because management was able to achieve efficiencies that expanded the project’s production capacity while lowering its ultimate unit production cost.

Warrior’s Attractive Investment Attributes

Like any commodity producer, the coal production business model has positives and negatives.

On the downside, met coal producers are price takers. These producers aren’t afforded the luxury (or curse?) of being able to hedge, as met coal lacks a developed futures market that is typically found among more heavily traded commodities. Unlike thermal coal producers, many met coal producers don’t enter into long-term sales contracts for their production. They therefore are at the mercy of spot prices. As such, a low-cost production base and strong balance sheet are paramount for surviving the industry’s recurring ups and downs.

Fortunately for met coal producers, several positive factors offset the price-taking negative. In many ways, they make the met coal producer business model superior to that of oil and gas production.

For one, large public U.S. coal producers aren’t saddled with long-term debt. These companies sought bankruptcy protection after a downturn in the 2010s and emerged with clean balance sheets. Coal is a global business due to the ease of transporting by sea, and U.S. met coal producers export most of their production to foreign markets. Even factoring in higher transportation costs borne by U.S. producers, their lack of leverage puts them at an advantage relative to their international competitors. Warrior, as the lowest-cost major U.S. met coal producer, will be the last company standing if prices remain depressed.

Met coal assets tend to be more capital-efficient than oil and gas assets, as maintenance capex consumes a relatively low proportion of operating cash flow relatively low. For example, Warrior’s Blue Creek project is expected to consume only $20 million per year of maintenance capex annually over the initial ten years of the mine’s life. For context, on a BTU-equivalent basis, Blue Creek’s production represents roughly 61,000 barrels per day of oil production. That amount of production would typically require well over $100 million to sustain on a conventional oil production base, which is multiple times more than what Warrior will spend to maintain Blue Creek’s production. Of course, lower capex per unit of output increases free cash flow.

Given the perception among many that coal will be phased out as a “sunsetting” industry, Warrior’s business model is surprisingly capital-light and sustainable. The success of its shares as an investment will hinge on management’s ability to stick to its knitting and not do anything dumb in allocating free cash flow. In recent years, Warrior’s peers returned significantly greater amounts of cash flow to shareholders while it spent capex to develop Blue Creek. I expect Blue Creek’s completion and the cash flow inflection triggered by lower capex and higher revenues to prompt a rapid and significant increase in Warrior’s dividends and share repurchases.

Warrior’s assets are competitively advantaged vis-à-vis transportation. Transportation is one of the greatest costs for a coal producer. Warrior benefits from having access to waterways that allow for transport to the port of Mobile, Alabama, where the company has a long-term agreement with the McDuffie terminal. The terminal has export capacity of 27 million metric tons per year, significantly greater than Warrior’s ultimate maximum capacity of 12.7 million metric tons per year. Warrior is one of the only coal companies using the Mobile port for export, so I assume it will continue to make attractive deals for access to McDuffie or other terminals. Warrior’s mines are 300 miles from port. Its peers are 350 miles or more from their nearest port. It is also serviced by several rail carriers offering competitive rates. Warrior can also transport its production by truck. Warrior’s domestic peers lack transportation flexibility and low cost, which pushes their cost of production per ton materially higher.

Warrior also benefits by operating two—going on three—large mines within a 50-mile radius. The lack of numerous far-flung mines allows Warrior to keep its costs lower than its domestic peers. The proximity of its assets to one another furthers its unit cost advantage.

Warrior is the lowest-cost met coal producer in the U.S. from an operating cost perspective, as shown in the following chart.

Source: Warrior Met Coal Blue Creek Project Presentation, Feb. 21, 2025.

Warrior’s low operating costs offset the higher transportation costs involved in exporting its production to foreign markets to make it competitive versus its U.S. peers.

Warrior has a multi-decade reserve life. Its more than 35 years of reserves is double that of its met coal peer Alpha Metallurgical Resources (AMR). Oil and gas producers are lucky if their proved reserves extend beyond 10 or 12 years. This may be a negative from a long-term macro perspective, as oil will enter periods in which supply is constrained and prices surge. Coal prices aren’t likely to spike due to supply constraints, but the fact that a coal producer can maintain production at a given rate for multiple decades relieves some of the pressure to make risky capital acquisition moves, such as overpriced acquisitions, which are far too common in oil and gas.

Last—but certainly not least—among Warrior’s competitive advantages is its top-notch management team. Management has kept the company conservatively capitalized since its exit from bankruptcy in 2016. It has maintained the company’s low-cost position and executed a transformative growth project. Since exiting bankruptcy, management has allocated capital superbly and generated an impressive total return for Warrior’s shareholders. I expect the outstanding performance to continue in future years.

Valuation

I expect Warrior’s free cash flow to range from a low of $300 million to a high of $1.3 billion over the next ten years. I can’t offer insight into the cadence of free cash flow in future years because I don’t know the future course of coal prices. However, I can assert with high confidence that the company will generate multiples of its current market capitalization in free cash flow over the next ten years.

Due to the negative stigma toward all things coal, all coal stocks are likely to continue trading at a discount to their intrinsic value. Given the magnitude of free cash flow that met coal companies like Warrior will generate over the coming years, they will be able to repurchase copious volumes of discounted shares.

If Warrior’s management can remain disciplined, sustain the company’s low-cost advantage, generate free cash flow, and repurchase shares, Warrior’s intrinsic value per share is likely to compound at a high rate even if the share price remains depressed on a current valuation basis. The key for an investor is to hold the shares long enough for the compounding to work in their favor. This is why Warrior is my favorite stock investment for long-term holding. It is likely to survive almost any bearish steel or coal market and will deliver tremendous value in more bullish markets. I expect all that value to be distributed to Warrior’s shareholders one way or another.

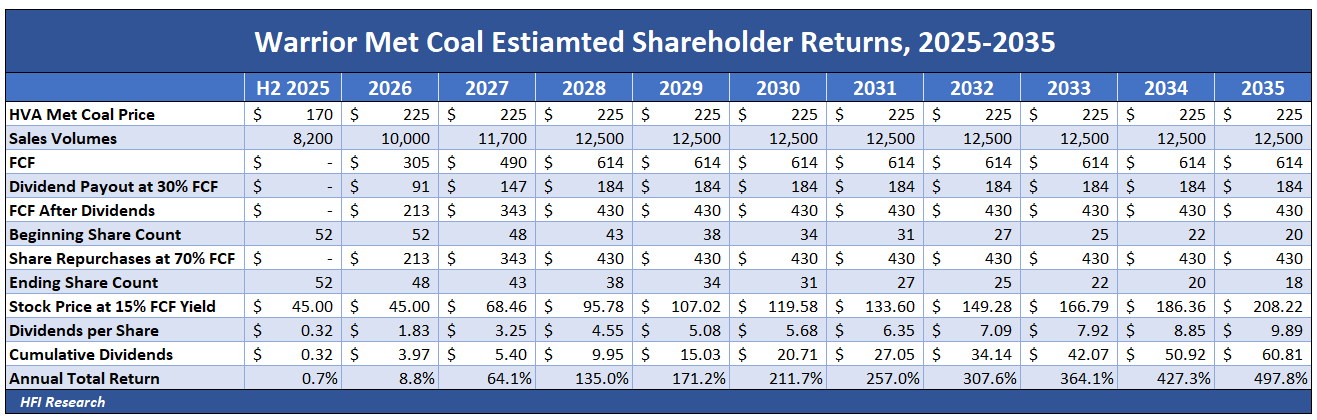

The compounding nature of Warrior’s value is demonstrated in the following table, which shows the company’s free cash flow generation at average normalized U.S. met coal prices over the next ten years.

The scenario assumes a constant met coal price of $225 per ton, which represents an average mid-cycle price. The scenario assumes Warrior’s production increases to a maximum of 12.5 million tons per year. The company allocates 30% of its free cash flow to dividends and 70% to share repurchases, while its shares trade at a 15% free cash flow yield.

The 497.8% return over ten years implies a 20.7% compound annual growth rate from Warrior’s current stock price of $45. Not too shabby for an old-economy company in a smokestack industry that traces its roots back to the 1940s.

In the immediate term, trade frictions are another factor pushing down Warrior’s stock price. The company exports almost all of its production to foreign markets, so its pricing is adversely impacted by tariffs. China’s 15% retaliatory tariffs against U.S. met coal producers hit its results worse than its peers. Despite the near-term headwind, any macro bearishness that creates a lower entry price for buying Warrior shares is bullish for today's buyers over the long term.

Due to Warrior’s status as a potential compounder, I believe its shares should not be sold unless they get ridiculously overpriced, which is unlikely to happen for a coal producer.

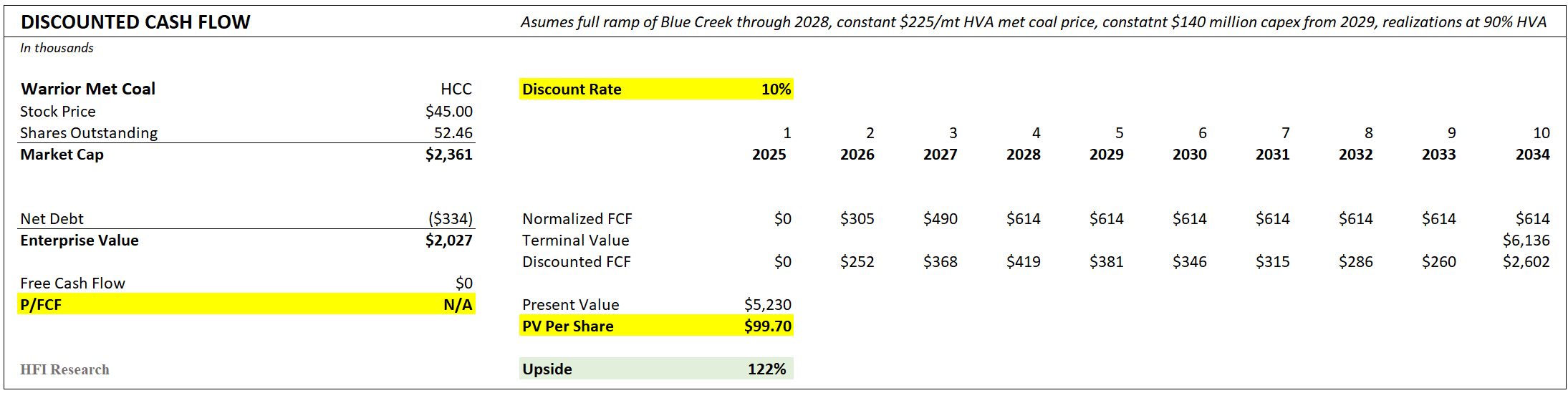

And for investors looking to buy cheap and sell amid a shorter-term pop, I estimate the shares are currently worth nearly $100, as illustrated in the following discounted cash flow valuation.

The scenario depicted in the table shows Warrior’s free cash flow amid average normalized U.S. met coal prices and Warrior’s production ramp over the next few years. The value implies 122% upside from the current price. Due to coal’s stigma in the investment community, I doubt Warrior’s shares—or those of any coal company, for that matter—will trade to the price implied by discounted cash flows under mid-cycle assumptions. Nevertheless, the massive discount leaves ample room for attractive returns from the current price, even if it is far below intrinsic value.

Conclusion

Warrior Met Coal should make intuitive investment sense to any bona fide value investor. If the investor can overcome the fact that their investment resides in an industry that is truly hated by the general public, prospects for outperformance over the long term are outstanding from current prices. The trick will be not to get shaken out of the shares. Warrior is one of the true set-it-and-forget-it investments. Long-term value hunters should consider buying the shares now at $45 or below.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of HCC, AMR either through stock ownership, options, or other derivatives.