(Public) Mach Natural Resources Enters The Buy Zone

Please read our previous article on MNR for context.

By: Jon Costello

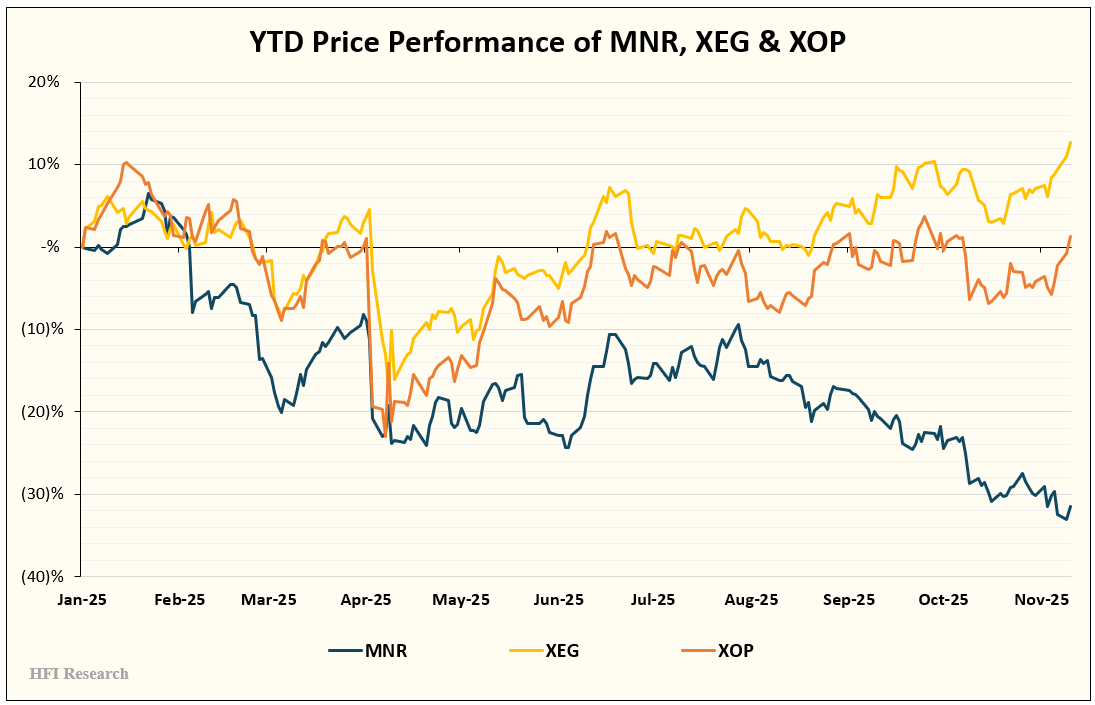

Mach Natural Resources LP (MNR) units have declined by 18% since I covered the name in August. Year-to-date, the units have severely underperformed their E&P peers. While the XEG has gained 13% and the XOP has remained roughly flat, MNR’s unit price has declined by more than 30%.

MNR’s selloff is unwarranted from a fundamentals perspective. Yet at the same time, the company’s third-quarter results illustrate its robust value proposition and management’s success in implementing its operating playbook.

In light of their discounted valuation and attractive prospects, MNR units offer an attractive long-term buying opportunity, particularly for income-oriented accounts.

Solid Q3 Results

MNR reported solid third-quarter results. The highlight was two transformative acquisitions that closed on September 16. Combined, MNR paid the $800 million for its IKAV and Sabinal acquisitions, which it financed by $525 million in cash and the issuance of 52.3 million common units.

The deals are expected to nearly double MNR’s production from around 84,000 boe/d to 153,000 boe/d. Both were made at a discount from PDP value and were accretive to distributions. They demonstrate management’s disciplined approach to executing its strategy of acquiring low-decline producing assets at a discount to PDP value, then reducing the costs of those assets to boost cash flow generation potential per unit.

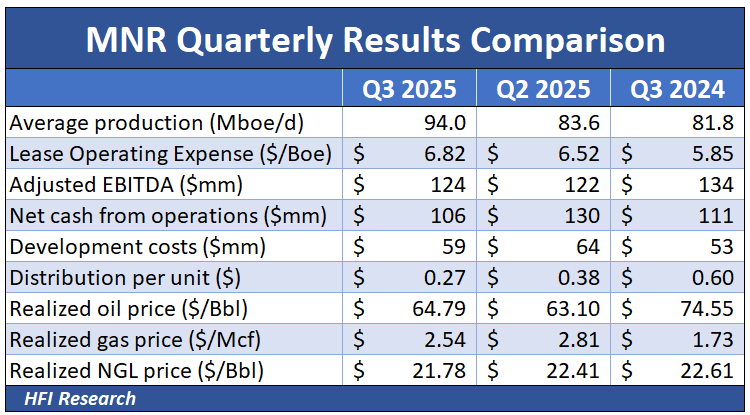

The acquisitions caused MNR’s production in the third quarter to jump to 94,043 Boe/d from 83,582 Boe/d in the previous quarter and 81,804 in the year-ago quarter. Third-quarter production was 21% oil, 23% NGLs, and 56% natural gas.

The chart below summarizes the quarter’s results.

MNR’s acquisitions during the quarter increased its leverage to 1.3-times Adjusted EBITDA, above management’s preferred target of 1.0-times. The company is likely to reduce debt to the targeted level over the coming quarters.

Meanwhile, liquidity is ample. At the end of the quarter, MNR had $295 million of borrowing availability on its revolver.

True to its operating principles, MNR reinvested slightly less than half of its operating cash flow back in the business. In doing so, production on its legacy acreage notched a modest gain. In the current period of low commodity prices, MNR’s low required reinvestment rate is serving it well. It should have no difficulty allocating its cash flow to keep production roughly flat while also paying large distributions and reducing debt.

Over the next few quarters, MNR will be focusing on its natural gas prospects. The company has stopped drilling its oil-weighted acreage in the Oswego Formation in Oklahoma and will instead target dry gas production from its Anadarko acreage.

The quarterly distribution of $0.27 yields 9.2% on the current unit price of $11.80. The distribution represents a reduction from the previous quarter’s $0.38 distribution, as the company wisely chooses to protect its balance sheet, which is more leveraged than it has been in the past.

Acquisitions Enhance Cash Flow Generation and Scale

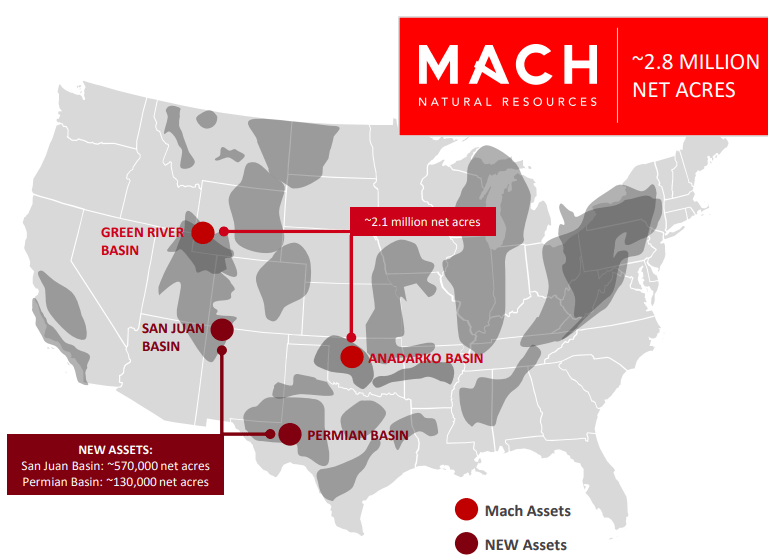

The third-quarter acquisitions fundamentally transformed MNR’s asset portfolio. The assets expanded the company’s operating footprint into two new basins, the San Juan and Permian, as shown below.

Source: MNR Natural Resources Q3 2025 Earnings Slide Presentation, Nov. 6, 2025.

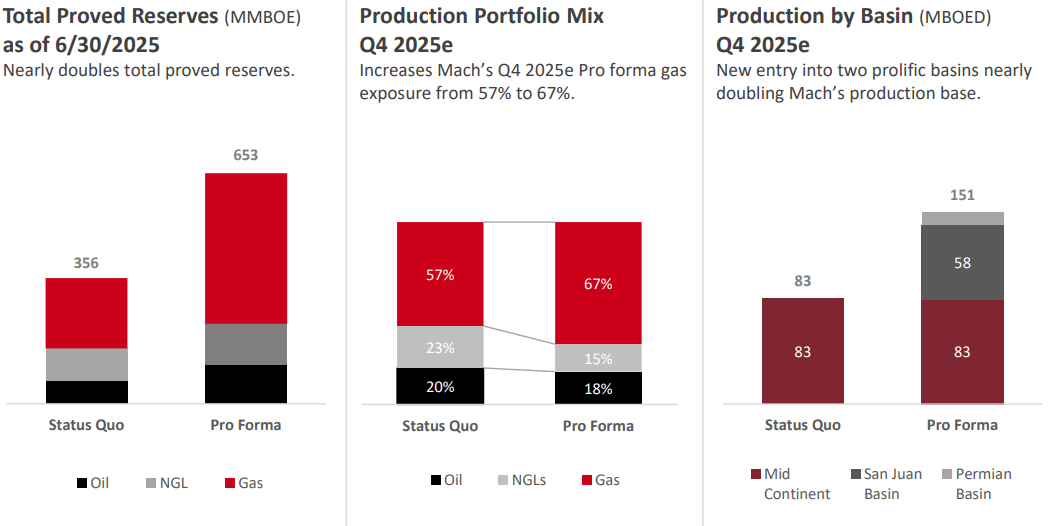

The company’s reserves and production have emerged from the deals with a higher gas content. Natural gas now accounts for 67% of PDP, up from 54%. Production in 2026 is expected to be 71% natural gas, up from 53%. The chart below shows MNR’s heavier natural gas weighting of its assets.

Source: MNR Natural Resources Q3 2025 Earnings Slide Presentation, Nov. 6, 2025.

MNR’s reserves are low risk, as 87% of proved reserves are comprised of PDP. This is exactly what an investor interested in generating income from an E&P equity should want to see.

The remaining 13% of proved reserves are undeveloped. The acquisitions extend MNR’s reserve life from 11 years to 12 years.

The acquired Permian asset’s PDP reserves are 99% liquids—and 96% oil—while the San Juan’s reserves are 8% liquids, providing development optionality depending on the outlook for commodity prices.

The acquisitions also enhance MNR’s earning power. Inclusive of the acquisitions, management’s disclosures point to an annual Adjusted EBITDA run-rate of $825 million, or $4.88 per MNR unit. This is up from a legacy Adjusted EBITDA run-rate of approximately $500 million, or $4.24 per unit.

The acquisitions will be accretive to MNR’s distribution. They reduce well costs as the company standardizes completions, part of its playbook of buying producing assets at a discount to PDP and then driving down costs. The gas-weighted nature of the assets will also help drive down costs. Management expects MNR’s drilling and completion capital to decrease by 18% in 2026 while maintaining stable production volumes.

Hedges Bolster Cash Flow, Facilitate Acquisitions & Protect Balance Sheet

The company has approximately 30% of its guided 2026 oil production hedged at WTI in the high-$60s per barrel range. It has approximately 25% of its 2026 natural gas production hedged in the high-$3.00s per mcf.

Hedges will provide cash flow to support the distribution over the next few quarters. They also reduce potential pressure from MNR’s bank group. Cash flow generated from hedges played an important role in enabling MNR to fund the $641 million it paid during the quarter in connection with the acquisitions while also paying $198 million in distributions to unitholders year-to-date.

On the downside, MNR’s hedge book will be a drag on cash flow if a natural gas bull market sends prices above $5 per mcf. However, overall, management is being prudent in forgoing some upside for cash flow and distribution stability.

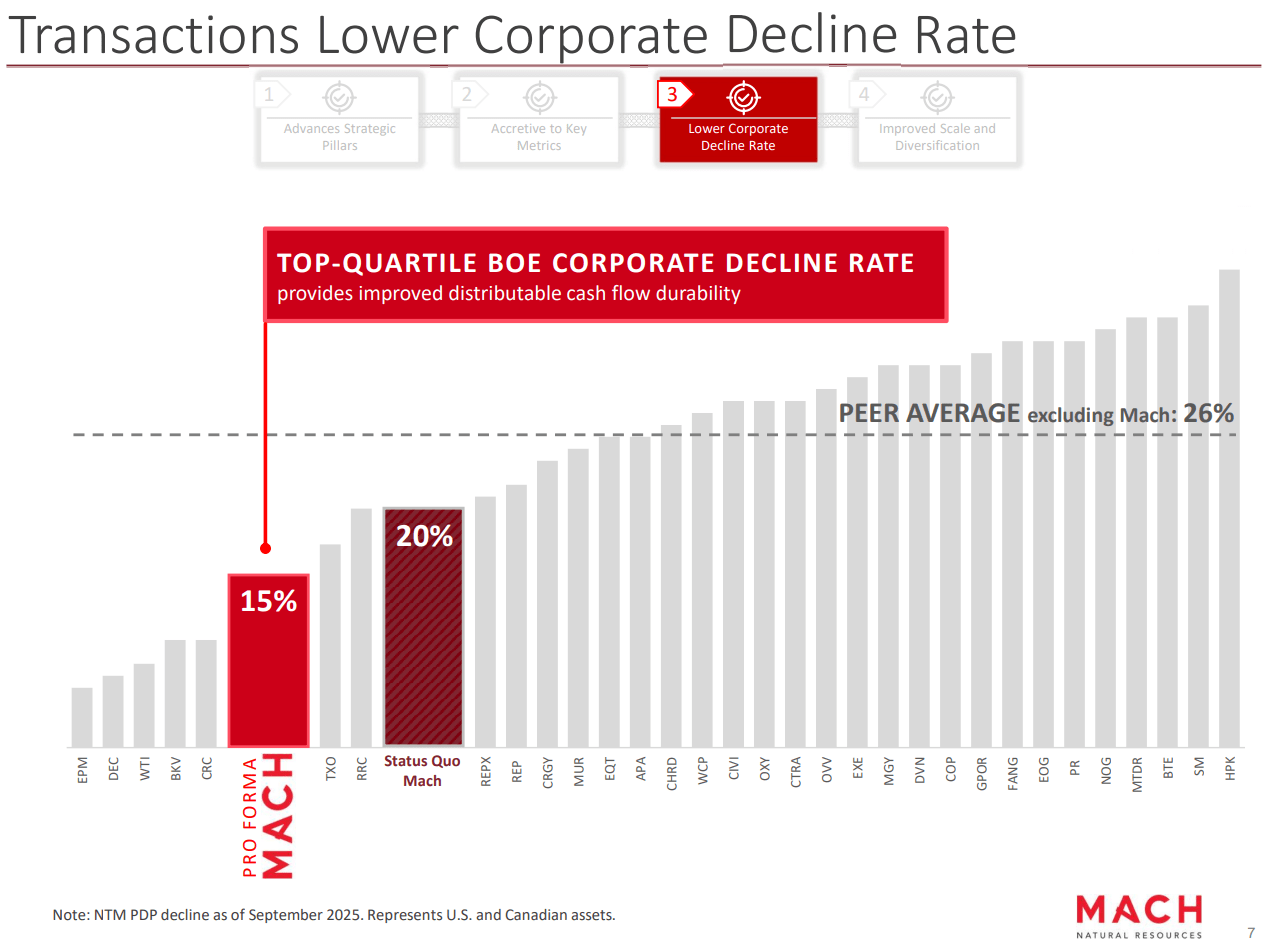

MNR’s Low Decline Rate Remains Intact

Cynical E&P industry observers may take issue with the timing and impact of the company’s recent acquisitions. The assets boosted production significantly late in the quarter, thereby flattering third-quarter results. Lower-quality E&Ps have used such tactics in the past to paper over production declines that exceed management’s guidance.

This is clearly not the case with regard to MNR’s September acquisitions. In fact, the company discloses in its 10-Q that the acquisitions added 1,034 Boe to third-quarter production, implying legacy production volumes of 7,620 Mboe, or 83,700 Boe/d. These volumes were above the prior quarter and year-ago quarter, in which production was 83,600 boe/d and 81,800 boe/d, respectively. Legacy production was therefore held roughly flat. This is an impressive achievement, given that only 49% of operating cash flow was reinvested into production.

The upshot of MNR’s legacy production is that the underlying trends are consistent with management’s guidance for a PDP decline rate in the mid-teens percent.

MNR’s low decline rate is a key part of its investment thesis. The rate is well below that of most peers, as shown below.

Source: MNR Natural Resources September 2025 Investor Presentation.

MNR’s low-decline rate enhances its operational and financial flexibility while allowing it to pay out significant cash to its unitholders.

A low-decline strategy has been used to good effect by other E&Ps in which I own shares. Cardinal Energy (CJ:CA) is a good example. Cardinal has allocated cash flow from its low-decline base to both paying dividends and investing in building out SAGD projects over the past year, despite low prevailing commodity prices. MNR is likely to continue to prioritize distributions, and its low decline rate provides assurance that it can do so.

Risks

An obvious risk for MNR’s unitholders is execution risk in the newly-acquired Anadarko and San Juan acreage, as the company’s distribution growth prospects hinge to some extent on its ability to drive cost efficiencies in these basins. Fortunately, management reported positive drilling results in its third-quarter conference call.

The second risk stems from management’s ability to maintain a cash flow reinvestment rate of 50% or below while sustaining a high distribution yield. I expect management to maintain capex at levels sufficient to keep production flat. It should have no problem doing so. However, the distributions could decline as long as commodity prices remain low. Nevertheless, I estimate that the company can sustain its current 9% distribution yield at current commodity prices if it allocates all of its free cash flow to distributions. Since debt reduction is now also a priority, unitholders should expect a 5% to 7% yield on the current unit price, which is more than reasonable relative to available alternatives, and given the tremendous income and appreciation upside in the units amid higher commodity prices.

Unitholders are also at risk from MNR’s leverage and the terms of its debt. The company’s revolving credit facility is secured by its assets. Since asset values are determined with reference to commodity prices, equity holders may face the risk of permanent losses if oil or natural gas prices plunge to low levels. This is exactly what we saw in 2020. Offsetting this risk, however, are MNR’s hedges and its low reinvestment rate required to keep production stable even at low commodity prices.

Further mitigating the risk posed by MNR’s leverage are recently negotiated amendments to its credit agreement. The amendments reduced the company’s interest cost, exempted up to $750 million of debt issued in 2025 from the amount MNR is allowed to borrow under the agreement, and increased the amount the company is able to borrow under the agreement by $700 million. MNR’s revolving credit line was increased to $1.0 billion.

All these measures substantially mitigate the risks stemming from MNR’s leverage. The amendments to the credit agreement, in particular, were well executed for unitholders. Despite the low risk, I still expect MNR’s management and board of directors to prioritize leverage reduction alongside distributions in the company’s capital allocation policy.

MNR will need to continue making accretive acquisitions to sustain its operating plan over the next three to five years. Consequently, its unitholders may be at risk if the company’s deal pipeline dries up. Over a period of years, this outcome could impair the company’s ability to sustain its production volumes and grow value for unitholders.

Fortunately, MNR’s expansion into other basins should allow it to find attractively priced acreage in its preferred price range of $100 to $150 million. After all, there aren’t many operators that have adopted MNR’s business model of pursuing similar-sized deals. The deal runway appears ample, and continued accretive tuck-in acquisitions are likely to be positive for cash generation potential and unitholder value growth.

Aside from the deal pipeline drying up, unitholders are at risk from the company overpaying for future acquisitions. This risk is largely mitigated first, by management’s disciplined long-term acquisition track record and second, by today’s low-price commodity environment. Assets bought at current prices aren’t as likely to be overpriced as they would be at higher commodity prices. Over time, I believe MNR’s recent acquisitions will be viewed as bargain purchases if oil and natural gas prices rise to the levels we expect in 2027 and beyond. In the meantime, I expect management to avoid deals that don’t meet its return parameters.

Reasons for MNR’s Valuation Discount

MNR’s units are cheap. An investor who expects higher natural gas prices and prefers to receive a substantial portion of their return delivered via cash should consider purchasing them as a long-term holding.

The company’s 3.8-times EV/EBITDA valuation is low compared to its E&P peers. The low valuation is likely due to numerous factors. For one, it is partly attributable to the market’s continued uneasiness about MNR’s strategy to expand through acquisitions, while it is also discounting the company’s heavy weighting in natural gas. Its status as an MLP and its policy of paying variable distributions are also factors.

None of these is a good reason for such a severe discount to be applied to MNR units. Management’s track record has been outstanding in executing the company’s strategy. It has adhered to the operating principles articulated at the top of every earnings conference call, and there is no reason to suspect that will change.

As for the MLP stigma, longtime readers know that I view the MLP discount as ridiculous and believe some of the most attractive bargains in the energy space lie in this space.

MNR’s valuation discount also flies in the face of the natural gas bull thesis. It should be considered a top vehicle for natural gas commodity exposure, though its pricing implies it is being overlooked.

Another cause of negative sentiment surrounding MNR is the possibility that its distribution will be reduced. However, as long as unitholders believe that current commodity prices are unsustainable over the long term—as we do—the most logical investment thesis for owning MNR is to assume the units pay a 5% to 7% distribution yield and that distributions will grow significantly over the coming years.

The last potential cause of MNR’s discount is its policy of paying variable distributions. However, this is arguably the most sensible policy for a distribution-focused E&P to distribute cash flow to its unitholders, particularly given the tax-advantaged status of MLP common distributions.

Valuation

MNR’s unit value is underpinned by management’s excellent capital allocation track record. The capital allocation watchword has been discipline, whether in acquisition criteria, capital reinvestment, or balance sheet protection.

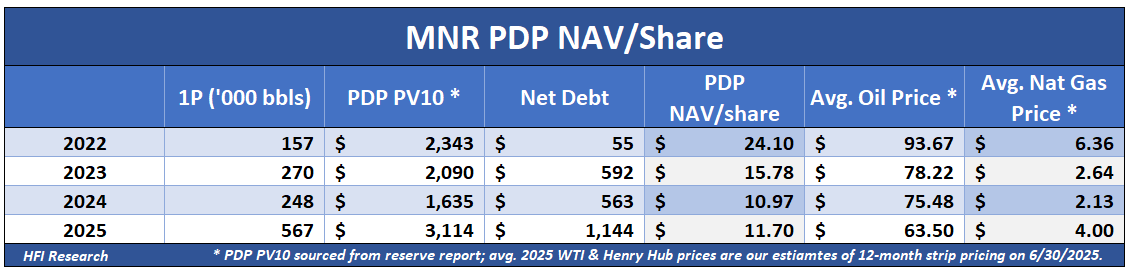

At their current price, the units sport a margin of safety between the company’s market cap and PDP net asset value (NAV). PDP NAV per unit stands at $11.70 using today’s depressed commodity prices. This value is in the ballpark of the company’s current unit price. However, PDP NAV per unit increases to approximately $13.70 assuming the company reduces net long-term debt to $800 million, which I expect will occur over the next 18 months.

Moreover, if we assume more realistic long-term commodity prices than today’s depressed prices, the margin of safety grows larger.

The PDP NAV in the table above also fails to account for the substantial value in MNR’s proved undeveloped reserves. That value represents an additional margin of safety, and another reason why I believe MNR’s units are attractively priced.

The units could benefit from cash flow upside in the event the company takes on a partner to fund drilling on its vast undeveloped acreage. Assuming MNR limits its own capital outlays, such an arrangement would further boost the company’s operating leverage amid higher commodity prices. At the same time, its cash flow could receive an additional boost from continued drilling cost reductions on its own acreage.

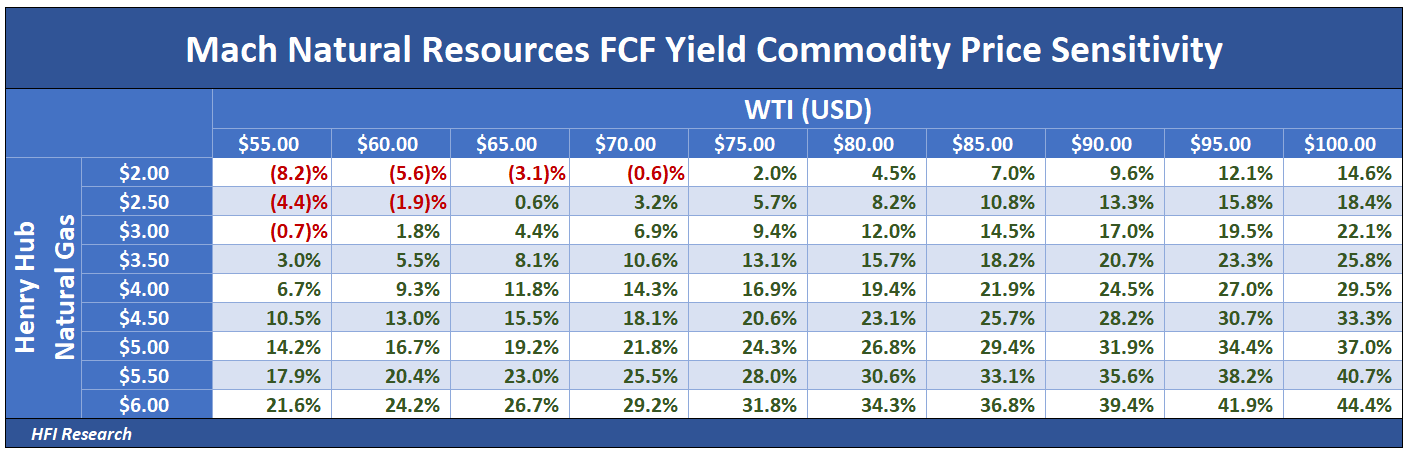

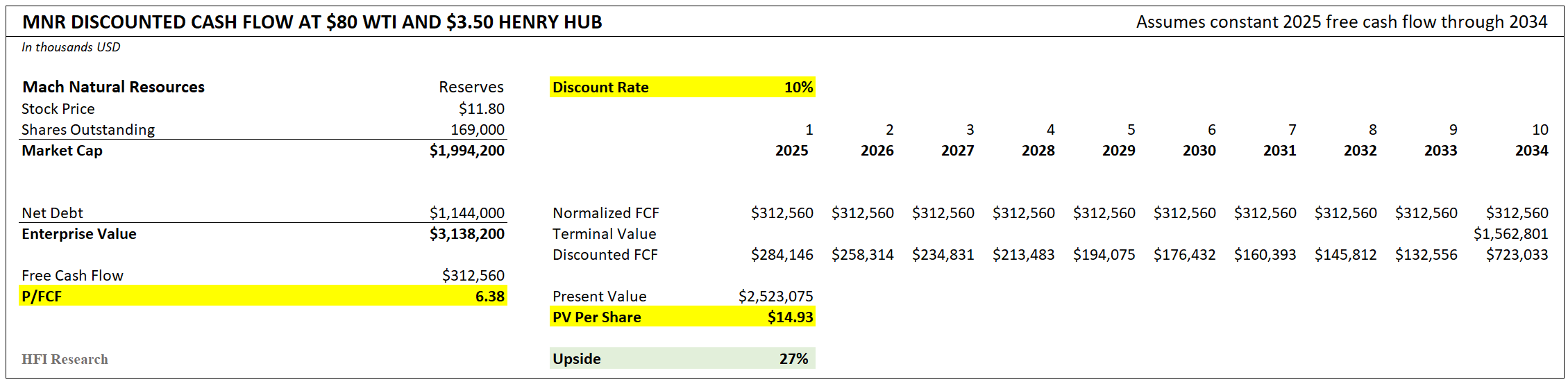

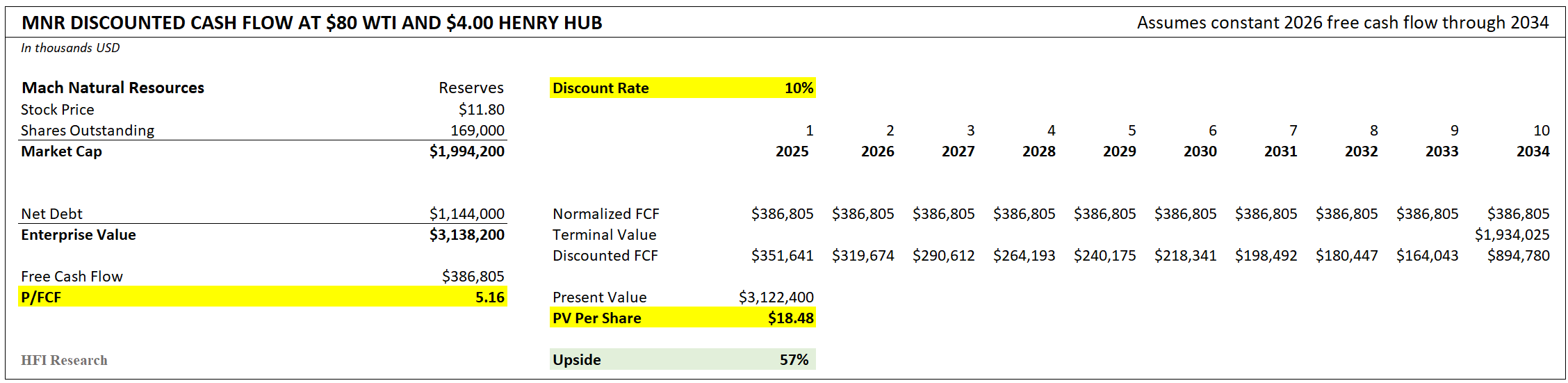

The table below illustrates the approximate unhedged free cash flow yield that MNR units can achieve at different commodity prices. Since the company intends to distribute cash flow via variable distributions, much of the cash flow yield will represent a cash return. The return becomes very attractive from the current unit price when Henry Hub Prices are sustained above $4.00 per mcf and WTI heads back toward $80.

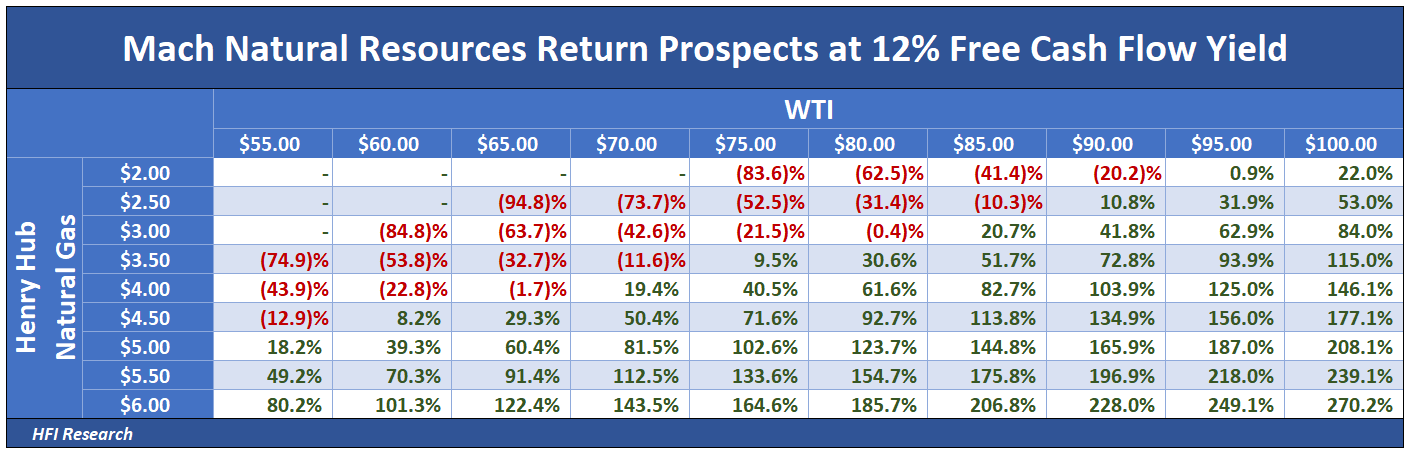

The following table illustrates the returns available to MNR unitholders assuming a 12% free cash flow yield at different commodity prices. The unit value really takes off once Henry Hub natural gas prices are sustained above $4.00 per mcf and WTI heads above $80 per barrel.

Assuming average long-term pricing of $3.50 per mcf natural gas and $80 per barrel WTI, the units are worth $14.93, implying 27% upside. This valuation cuts MNR’s terminal value in half to be conservative.

Given the new gas-weighted production mix, MNR’s valuation is sensitive to natural gas prices. Assuming a long-term natural gas price of $4.00 and WTI at $80 per barrel, the units’ value increases to $18.48, implying 57% upside.

Conclusion

Over the past five years, I’ve analyzed and follow virtually every publicly listed MLP in the energy sector. MNR clearly offers the most upside as oil and natural gas prices rise. Midstream MLPs tend not to have direct commodity exposure, so MNR represents an attractive alternative for MLP investors seeking cash flow torque from higher commodity prices. In fact, MNR would be my go-to name for income at its current price up to $12.50 per unit.

Ideally, long-term investors should purchase publicly-listed E&P equities the same way MNR pursues its own acquisitions: by buying low-decline assets below PDP NAV when commodity prices are depressed, then harvesting cash flow when prices are high. This is what buyers of MNR units are getting by buying today and holding for the long term. MNR unitholders can be confident that surging cash flow at higher commodity prices will be paid out as distributions. The discipline management has exercised so far indicates that the company’s cash flow will not be squandered by acquisitions that fail to meet management’s criteria.

Given our expectations for higher oil and natural gas prices, combined with MNR’s long inventory runway, its measured approach toward reinvestment and development, its reasonable leverage profile, and additional upside from developing currently undeveloped acreage, I expect MNR’s distributions alone to generate highly attractive returns over the next three to five years. Add in capital appreciation prospects, and a 100% total return is in the cards. With a high potential return and low risk, investors should consider buying MNR units now.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MNR either through stock ownership, options, or other derivatives.