By: Jon Costello

It has been a while since I wrote an update on Cheniere Energy (LNG), which we’ve held in the HFIR Energy Income Portfolio since January 2021. The company recently reached an important milestone and has begun a new phase of growth. How it executes this next phase, as well as prevailing macro natural gas market conditions over the coming years, will have a significant bearing on its stock’s performance.

Cheniere’s track record of execution and strong financial position make it the conservative way to obtain exposure to LNG over the coming years. More than 95% of the company’s production volumes through the mid-2030s are under long-duration sale-and-purchase agreements (SPAs) with a 15-year weighted-average remaining life. Those contracts alone are expected to deliver more than $20 per share of run-rate distributable cash flow (DCF) regardless of where global LNG prices settle. Share repurchases and production growth are set to increase DCF from $20 per share to $30 per share.

Cheniere shares exceeded our published $180 price target in November 2023. DCF growth going forward places fair value at approximately $330.

With Cheniere shares trading at $272, investors who own the name should stay put as management’s execution builds value. They should consider trimming once the shares reach $300, at which point the stock would trade at roughly 90% of fair value.

Investors looking to buy or add to the name should wait for a pullback after the shares’ run from $190 to $272 over the past four months.

20/20 Vision Now Complete

On February 26, 2026, Cheniere completed its 20/20 Vision capital allocation plan. The plan had been announced in September 2022 and served as a framework for allocating the $20 billion in DCF management expected to be generated over the next five years.

Due to consistently outstanding execution, the company completed the plan ahead of schedule. Its forecasted $20 billion in DCF had been generated and allocated to debt repayment, share repurchases, dividends, and growth. It also achieved its targeted DCF run rate of $20 per share.

True to form, Cheniere didn’t rest on its laurels after completing its plan. It immediately launched a new five-year plan that featured an upsized repurchase authorization of $10 billion and a $30-per-share run-rate DCF target on a 175 million share count, implying a 17% lower share count due to repurchases.

I expect this new plan to be completed, and for its completion to drive Cheniere shares to my fair value estimate, which is 21.3% above the current share price.

The 2026-2030 Plan has Begun

Cheniere’s recent financial and operating performance speaks to its ability to achieve its 2030 plan, as it continued to execute superbly on all fronts.

In 2025 alone, the company repaid $652 million of consolidated long-term indebtedness. It repurchased 12.1 million shares for $2.7 billion, including 4.8 million at lower prices in the fourth quarter for $1.0 billion. During the year, it allocated 52% of DCF to share repurchases. Quarterly dividends of $0.555 per share—$2.22 per share annualized—came to $451 million, and growth capex reached $2.6 billion for CCL Stage 3 commissioning.

Looking ahead, the company’s 2026-2030 framework features more of the same capital allocation execution. The board’s $10 billion share repurchase authorization, which is comprised of the $1.2 billion remaining under the previous June 2024 authorization plus an additional $9 billion, represents a more than doubling of potential repurchases, with $9 billion of new capacity versus the prior $4 billion program.

Assuming an average share price of $280, $10 billion of repurchases will retire roughly 36 million shares, bringing the share count from approximately 210 million today to approximately 174 million by 2030. The repurchases increase DCF per share by 21%. Growth projects, namely Sabine Pass Liquefaction (SPL) Expansion and Corpus Christi Liquefaction (CCL) Expansion, would represent DCF upside if they proceed. I expect the repurchases, along with the cash flow generated by the growth projects, to enable the company to achieve its $30-per-share target.

SPAs Provide Cash Flow Stability

Cheniere’s contracted SPAs form the backbone of its investment thesis. According to the company’s latest investment presentation, approximately 95% of total anticipated production from the SPL and CCL projects is contracted through the mid-2030s.

These agreements lock in cash flow through the next decade. The contracted cash flow floor they create is set to deliver more than $20 per share of annual DCF today. The integrity of cash flow is underpinned by creditworthy counterparties, which include investment-grade global buyers such as Shell (SHEL), BP (BP), TotalEnergies (TTE), KOGAS, CPC Corporation, and others. These buyers pay Cheniere fixed take-or-pay fees regardless of whether they lift the cargo.

Meanwhile, non-contracted cargoes capture spot price spreads between global JKM and TTF LNG pricing and domestic U.S. Henry Hub natural gas pricing. Spot exposure adds upside in tight LNG markets and removes upside in weaker markets, but it doesn’t impact the cash flow floor provided by long-term SPAs. If macro conditions in the LNG market push prices higher, spot exposure could accelerate Cheniere’s path toward its $30-per-share DCF target.

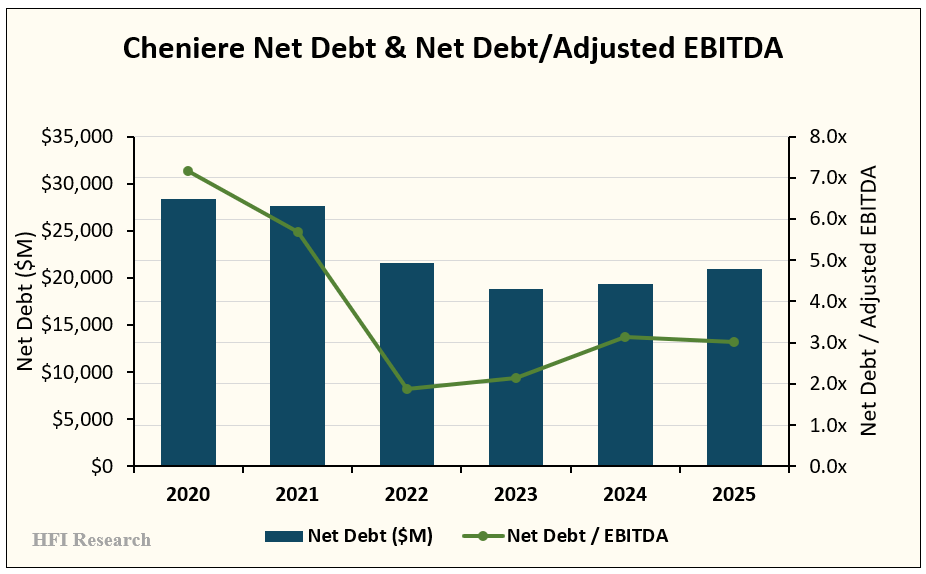

Balance Sheet Strength Adds Safety

Liquidity at year-end 2025 was ample, totaling $8.8 billion, including $1.1 billion in cash, $485 million in restricted cash, and $7.2 billion in credit facility availability. Long-term debt stood at $22.5 billion. Sabine Pass Liquefaction retired the full $500 million of its 5.875% 2026 Senior Notes between December 2025 and February 2026.

Net debt increased by roughly $1.5 billion in 2025 as Cheniere drew down cash to fund $2.7 billion in buybacks and $2.6 billion of growth capex. Leverage remained conservative throughout the year. With full-year 2025 Adjusted EBITDA at $6.9 billion versus $6.2 billion in 2024, its net-debt to EBITDA ratio fell modestly, from 3.1x in 2024 to 3.0x in 2025.

The credit rating agencies have a favorable view of Cheniere’s balance sheet. S&P Global Ratings upgraded Cheniere Energy, Inc. and Cheniere Energy Partners (CQP) from BBB to BBB+ with stable outlooks in November 2025. Cheniere Corpus Christi Holdings was upgraded from BBB to BBB+ with a positive outlook in October 2025. The upgrades reflect the company’s enhanced operating quality following the commissioning of CCL Stage 3 and improved cash flow visibility.

Three DCF Scenarios

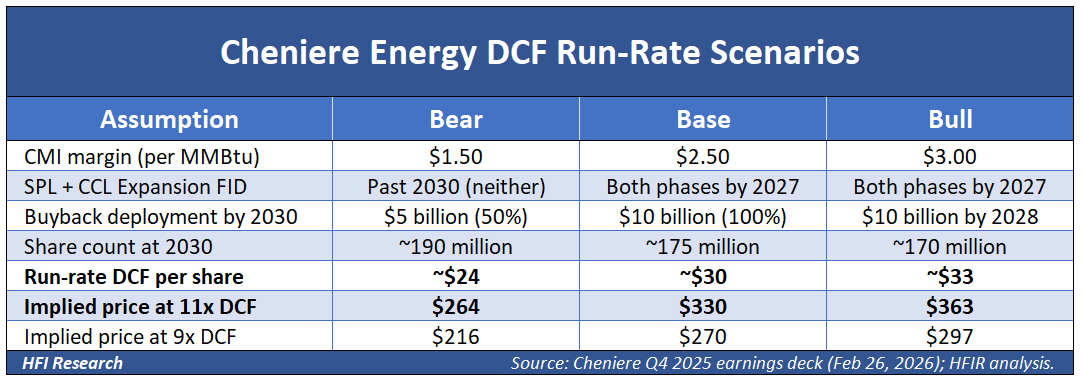

Cheniere’s 2026-2030 capital plan has clear implications for its stock. The following three scenarios illustrate the potential upside and downside. Each features assumptions pertaining to management’s execution, the macro backdrop, and the company’s financial performance.

The contracted long-term SPAs provide a cash flow base. Changes from the base depend to a significant degree on marketing activities conducted by Cheniere Marketing International (CMI), Cheniere’s in-house marketing and trading arm. CMI sells uncontracted LNG volumes into the spot and short-term markets, capturing the spread between Henry Hub feedstock prices and international LNG prices.

My base scenario follows management’s guidance, with CMI’s margin at $2.50 per MMBtu, both SPL and CCL Expansion final investment decisions (FIDs) by 2027, and full deployment of $10 billion. The bear scenario shrinks CMI’s margin to $1.50 per MMBtu, defers both Expansion FIDs past 2030, and deploys only $5 billion of the $10 billion buyback. The bull scenario maintains the same FID assumption, increases CMI’s margin to $3.00 per MMBtu, and accelerates repurchases to 2028.

The base scenario, at an 11x DCF multiple, supports a share price of $330. I expect such a scenario to provide long-term holders of the name an opportunity to exit at a higher price.

The bull scenario at an 11x DCF multiple implies a price of $363, for 33.5% upside. A more conservative bull scenario using a 9x multiple implies a price of $297, 9.2% above the current price and just below my planned trim level.

A bear scenario at an 11x DCF multiple supports $264, 3% below the current price. However, a more severe bear scenario using a 9x multiple supports a $216 share price, representing 20.6% downside. The stock price declines in this scenario due to multiple compression, as DCF per share is roughly flat with 2026.

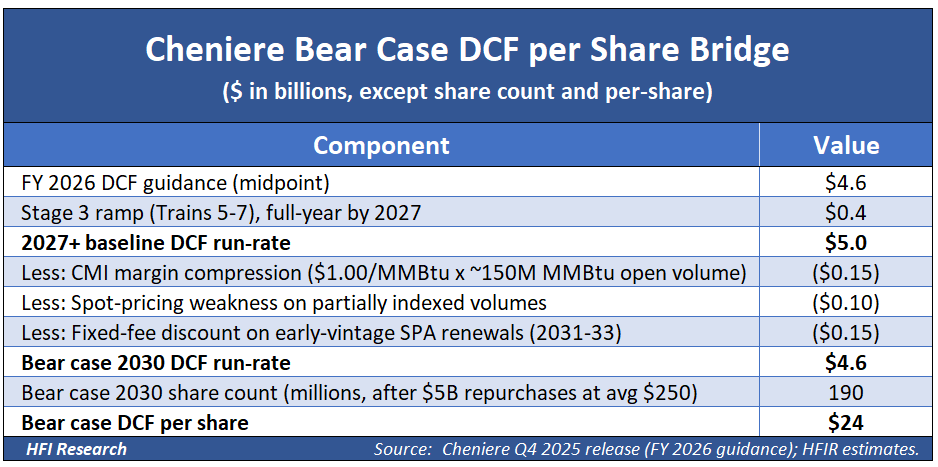

The table below walks through the bear scenario math, the most adverse of the three scenarios.

Risk-reward at $272 features 21.3% upside, with downside ranging from negligible at flat multiple to material at full margin compression.

Applying analogous bridges for the base and bull scenarios produces the DCF per-share figures shown in the scenario table below.

At $272, the call is to hold. My base scenario puts fair value at $330, implying roughly 21% of upside that share buybacks should help deliver over the next 18 to 24 months. Current holders of the shares should consider trimming at $300, or at roughly 90% of fair value, taking, say, 20% to 30% of their position off the table, and accelerate trimming above $325, where the stock would already reflect near-perfect operational and financial performance. However, I wouldn’t be likely to exit the shares completely at any level, as Cheniere’s contracted cash flows and ongoing buybacks should continue to grow per-share value over a five-year period, and perhaps beyond.

For investors looking to add to their position, consider entering around $240. At that level, Cheniere trades at approximately 11x current run-rate DCF and 8x the $30 DCF target. This multiple would be at the low end of the historical range for high-quality contracted midstream operators. The $216 price in the bear scenario at a 9x multiple is 10% below $240, while the $330 price in the base scenario is 37% above. That 4-to-1 upside-to-downside is the kind of setup that I believe justifies adding in size rather than nibbling.

Downside Risk

Given all the operational and macro-level risks in the outlook, it is important to consider the various ways my fair value estimate can fall short. Four bearish variables, in particular, could cause Cheniere shares to undershoot my estimates in the scenarios above.

The first variable is multiple compression. At $272 per share, Cheniere trades at roughly 12.5x its full-year 2026 guidance midpoint DCF of approximately $21.90 per share ($4.6 billion ÷ 210 million shares). High-quality, contract-protected midstream peers trade at DCF and EBITDA multiples in the 8x to 11x range. Cheniere’s 15-year weighted-average remaining life on its SPAs and its relatively high return on capital support a multiple at the high end of the range. Still, company-specific or sector-wide multiple compression would provide a headwind for the share price.

The second bearish variable relates to Cheniere’s post-2030 SPA roll-off schedule. The company does not disclose details other than the 15-year weighted-average life of its contracts. However, this statistic suggests the company is exposed to repricing risk as contracts renew after 2030. If contracts roll off in a softer global LNG market, both fixed-fee renewals and CMI margins are at risk of repricing downward.

A subtle disclosure trend in the 2025 10-K reinforces roll-off risk. Cheniere states in its 2025 10-K that approximately 90% of total anticipated production from the SPL and CCL projects is contracted through the mid-2030s. This is down from 95% in the 2024 10-K. The likely explanation for the decline is that the 10-K denominator reflects in-construction CCL Stage 3 capacity for which long-term SPAs have not yet been signed. As growth capex delivers new production volumes, this percentage could drift lower until expansion-related SPAs catch up. The bull scenario on Cheniere therefore depends in part on management’s ability to commercialize SPL Expansion and CCL Expansion volumes ahead of the early-2030s roll-off, execution that has been strong but cannot be guaranteed.

However, I’m not overly concerned about roll-offs in Cheniere’s case. For one, recent contract signings point to upside, not downside, on the pricing front. Cheniere’s long-term deals with Galp (GLPEY), Equinor (EQNR), Foran Energy, and others, signed between 2022 and 2025, locked in higher fixed fees than the older contracts they replaced. As a result, the portfolio’s average pricing is increasing, not declining. The bearish premise assumes a deterioration that these contract wins appear to contradict.

Furthermore, Cheniere’s main competitor is potentially in trouble. Venture Global (VG) is in arbitration with BP, Shell, and other major customers over cargoes VG diverted to spot markets instead of delivering to its customers under contract. The damages claimed run into the billions, and the situation poses financial risks for VG while also diminishing its standing as a reliable supplier. After VG’s actions, I suspect LNG buyers looking to lock in post-2030 volumes will be willing to pay a premium for proven operating and delivery records. Cheniere has an impeccable track record in both areas, which should result in higher fixed fees in new SPAs.

Lastly, the math holds in the moderate bear scenario. Even after applying the bear adjustments shown in the bridge above—CMI margin compression, spot-pricing weakness, and a fixed-fee discount on early-vintage SPA renewals—DCF lands at $24 per share. At a 9x multiple, which is low for contracted infrastructure operators, the shares would trade at $216, or 21% below today’s $272. Meanwhile, the base scenario produces $330 at 11x, or 21% above the current price.

That said, Cheniere investors should know that the moderate bear scenario detailed above isn’t the potentially deepest downside. An extremely bearish scenario, in which the CMI margin declines to $1.00 per MMBtu in a structurally oversupplied 2027-2028 market, $5 to $7 billion of repurchase capacity is redirected to growth capex, the CCL Stage 3 ramp is delayed by six to nine months, and SPAs are renegotiated at, say, 15% below current fees, reduces DCF to $18 to $20 per share. At an 8x multiple, the implied price is $144 to $160, or a 41% to 47% decline.

While I think it’s highly unlikely that all these stressors occur simultaneously, it’s not entirely implausible, particularly amid severe global economic deterioration. Still, the moderate bear remains my central downside scenario and is part of the reason why I’ll consider trimming above $300.

The third variable that would cause Cheniere shares to undershoot my fair value estimate is the timing of the SPL Expansion FID. The project’s FERC application and DOE non-FTA application remain pending. A 12- to 24-month completion slip puts $4 to $6 per share of DCF at risk, which is the mid-decade catalyst for a bullish outcome.

A fourth bearish variable is a sustained rise in U.S. natural gas prices. Cheniere is largely insulated on its long-term contracts because customers pay the gas cost as a pass-through, but sustainably higher Henry Hub prices, which natural gas bulls believe will be driven by data center demand, home heating recovery, and LNG export growth, could reduce earnings on spot-market sales by $50 to $150 million annually and, more importantly, make new U.S. LNG contracts less competitive against lower-cost global supply, such as that produced by Qatar. Those new contracts are what the bull case depends on to fund expansion.

Beyond the four bearish variables above, four specific developments would cause me to consider trimming or selling Cheniere shares more aggressively. If the company were to repurchase less than $2 billion of stock in 2026, the path to a 175-million-share count would extend longer, and management’s commitment to its buyback pace would come into question. If Cheniere signs a new long-term SPA at $2.00 per MMBtu or below—which would be roughly 25% below current pricing—it would signal that the prices the company can lock in for contracts rolling off after 2030 are lower than the bull case assumes. If the completion date of CCL Stage 3 Trains 5-7 slips past March 2027, the company’s 2027 EBITDA would be at risk of declining below my estimate. And if regulators delay an authorization of the next major expansion past year-end 2027, 20 MTPA of growth gets pushed into the early-to-mid 2030s. Any one of these outcomes alone would dim my view of the company’s prospects. Two or more would prompt me to consider selling.

Conclusion

Cheniere is the conservative way to own LNG. The contracted floor delivers more than $20 per share of run-rate DCF today, and the buyback math drives DCF per share to roughly $30 by 2030. At $272, investors should consider holding and potentially trimming above $300.

We entered Cheniere on January 25, 2021, at $63.82 in our HFIR Energy Income Portfolio. Our position has generated a 334.6% total return and now stands at a 6.0% weighting in the portfolio. Outstanding execution in operations, deleveraging, distributing capital to shareholders, and a strong contracted cash flow floor drove our gains. I expect the same factors to continue sending the shares to $300. At that point, depending on the macro backdrop, I’ll consider trimming my position and holding the rest as the framework continues to work.

Link to HFIR Energy Income Portfolio on RunPlutus.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of LNG either through stock ownership, options, or other derivatives.