(Public) Buy Quality If Tariffs Cause A Panic In Canadian Energy Equities

By: Jon Costello

At a press conference on Thursday and again earlier today, President Trump announced that he would decide whether to place tariffs on Canadian crude imports. Tariffs on oil are not our expected case due to their impact on the U.S. energy industry and the energy prices paid by consumers. Nevertheless, we have to acknowledge that they’re a possibility and respect the fact that betting markets and stock markets are discounting some degree of tariffs.

There is some confusion about whether tariffs will be implemented on February 1 or March 1, as reported by Reuters. However, the CBC reported more recently that the deadline remains February 1 and that oil and refined products won’t be exempt. Either way, we’re on the lookout for buying opportunities if and when tariffs come to pass.

Tariffs Would Harm the U.S.

Our basis for doubting the imposition of tariffs is simply to recognize that Trump may be wily and come across as crazy at times, but he isn’t stupid. Tariffs on Canadian oil imports would be a stupid move on many levels.

A scenario in which 25% tariffs are implemented on Canadian oil imports is a frightening one for U.S. consumers and the U.S. economy. The impact would deliver a blow to US refines, particularly those in the land-locked Midwest that were built to process Canadian heavy crude. To avoid paying up for Canadian heavy oil feedstock and producing refined product output at an uncompetitive price, U.S. refiners would attempt to meet their heavy oil requirements through foreign imports, straining the import capacity at the U.S. Gulf Coast and making the U.S. more reliant on countries that the Trump administration has in its crosshairs, such as Mexico and Venezuela. Canadian inventories could fill up. In response, the Albertan government could mandate supply curtailments, which would push heavy oil prices higher by reducing supply and narrowing the WCS-WTI spread.

Refineries would max out their throughput of lighter barrels, which could push WTI higher because inventories at the Cushing hub are extremely low. Eventually, increasing WTI prices would feed through to higher gasoline and diesel prices, angering voters. Depending on how high gasoline prices go, the surge could raise concerns about a recession, as past recessions tended to be preceded by a spike in oil and gasoline prices.

Politically, tariffs’ negative impact on the U.S. would make Trump look silly on the global stage. It would hurt his favorability rankings in the polls and cause voters to question his commitment to maintaining low energy prices and a strong economy. It would also damage the electoral prospects of incumbent Republicans.

If a lesser tariff of, say, 10%, were imposed, it would take longer to work its way through the system, but it would still have the negative impact described above.

The tariffs would hit the Canadian economy hard, forcing the lame-duck and currently ineffective Canadian government to act on Trump’s peeves about illegal border crossings and fentanyl smuggling.

We wouldn’t expect tariffs to last long. Once they are repealed, all Canadian E&Ps would be hit, followed by a snap-back. Even the highest-quality names would sell off. Opportunities to buy the highest-quality energy stocks at a discount don’t arise often, so this tariff imbroglio presents an outstanding long-term buying opportunity.

A Rare Opportunity to Buy Quality

One of the juiciest opportunities will be shares in companies whose stocks tend to be relatively insulated from macro-related downside due to the high quality of their business. In an environment of heightened fear, even these stocks would be sold by skittish shareholders and others who will sell the shares short.

My first high-quality pick would be Canadian Natural Resources (CNQ). Among the larger North American independent oil and gas producers, CNQ has the best acreage, longest reserve life, and best economics. Its stock trades at a nearly 10% free cash flow yield, which will grow with higher oil prices and production growth. CNQ has minimal debt and the lowest operational and financial risk in the sector.

Source: CNQ 2025 Budget Presentation, Jan. 9, 2025.

CNQ shares would suffer under a harsh tariff regime but would emerge unscathed.

CNQ’s latest big move was to buy Chevron’s (CVX) 20% interest in the Athabasca Oil Sands Project, bringing CNQ’s working interest in the project to 90%. The deal also included Chevron’s 70% interest in Duvernay acreage.

Chevron was motivated to make the deal to simplify its operations and help it fund its purchase of Hess Corp. (HES). It was also following the herd of major oil companies, as BP (BP), Shell (SHEL), ConocoPhillips (COP), Equinor (EQIX), and Devon Energy (DVN), have all sold their oil sands assets at what turned out to be discounted valuations to Canadian operators who have benefitted tremendously from owning and operating the assets.

In January, CNQ swapped its 10% interest in the Scotford synthetic oil upgrader and certain carbon capture facilities for Shell’s (SHEL) 10% interest in the Athabasca Oil Sands Project. This increased CNQ’s working interest in the project to 100% and added 31,000 bbl/d of synthetic crude oil production at a low cost. CNQ will still operate and own an 80% interest in the Scotford upgrader. We wouldn’t be surprised to see CNQ make additional deals to increase its stake in the upgrader.

This is another example of CNQ’s savvy moves to add high-quality oil production on the cheap.

In October, CNQ also increased its quarterly dividend by 7% to $0.5625. At its current stock price of $43.34, CNQ pays a safe 4.8% yield.

Tariffs that temporarily push CNQ shares lower would present a no-brainer buying opportunity. For investors concerned about the economic or oil price outlook on a longer-term basis, CNQ is an excellent ballast position in an energy stock portfolio. If an oil market or macroeconomic downturn were to arrive, CNQ could be sold to buy stocks trading at steep discounts with big upside in a recovery.

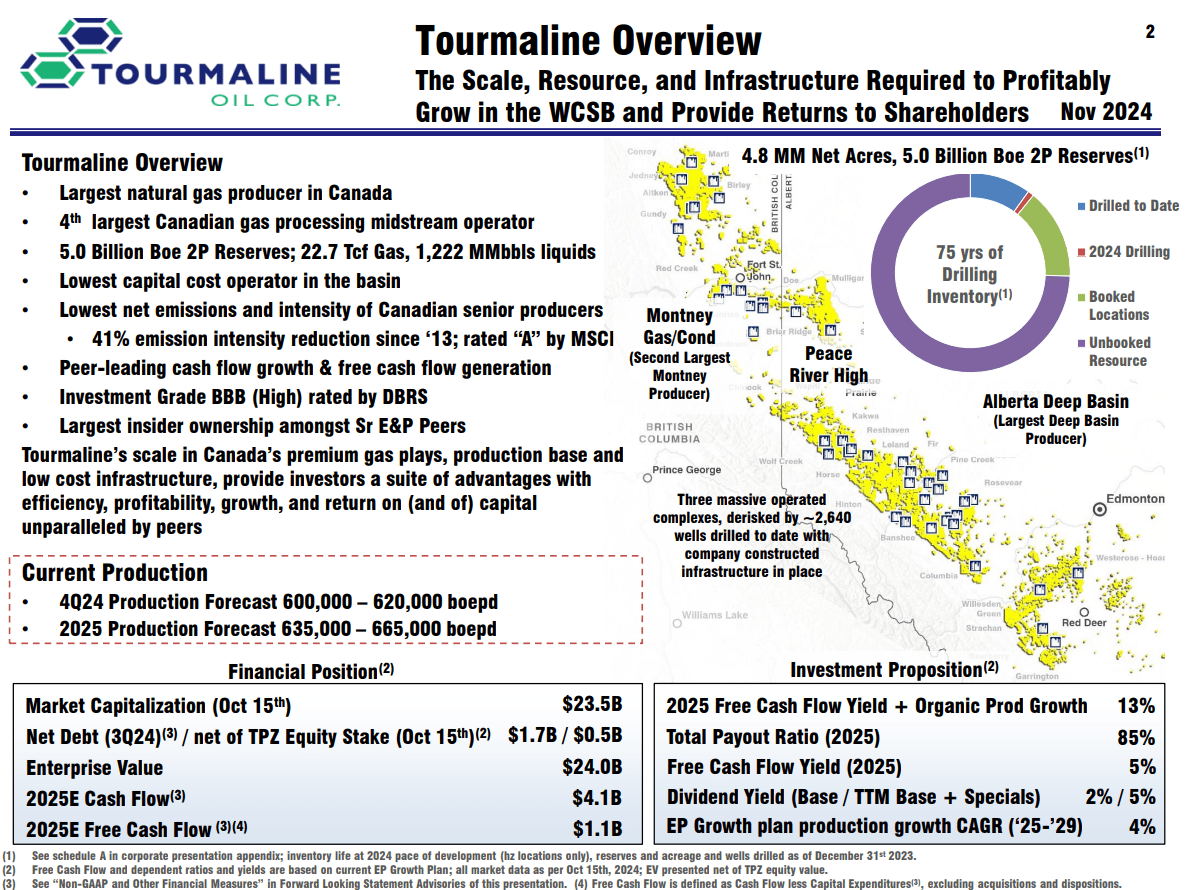

My top high-qualtiy natural gas pick would be Tourmaline Oil (TOU:CA). Despite its “oily” name, Tourmaline is the CNQ of North American natural gas. Surprisingly, its shares have not significantly benefited from the speculative frenzy surrounding data center natural gas demand, which has pushed many of its peers’ stocks higher. TOU shares would be pulled down with the rest of the Canadian oil and gas sector, creating an attractive entry point for the stock.

Source: Tourmaline Oil November 2025 Investor Presentation.

TOU benefits from its world-class asset base and marketing operation. Its size and operational prowess allow it to capture higher natural gas prices available at the US Gulf Coast. The company is led by Mike Rose, one of the best executives in North American business. Rose has seemingly miraculously created a company in which the top talent in the industry feels at home, cementing a long-term competitive advantage that peers can’t touch.

Like CNQ, TOU has a multi-decade drilling inventory and high-returning assets. We expect the company to continue consolidating the most strategic natural gas producing properties in the western region of the WCSB. It will continue to do so on attractive terms for its shareholders, building value over time and increasing free cash flow, which will be distributed as dividends. TOU is an outstanding income play, and we own it in our HFIR energy income portfolio.

TOU is a big dividend payer. Consider that it paid out a total of $3.32 in base and special dividends in 2024 despite operating in one of the lowest natural gas pricing environments in history. TOU’s dividends in 2024 represent a 5.0% yield on its current share price of $66.81. Its dividends will be significantly larger if natural gas prices increase, as we expect.

On the income side, my favorite high-quality name is TC Energy (TRP). The company owns a massive natural gas midstream infrastructure footprint that is dominant in Canada, as shown below.

Source: TC Energy Investor Day Presentation, Nov. 19, 2024.

We’ve owned TC Energy shares in our HFIR Energy Income Portfolio since they sold off in late July 2023. We intend to hold onto the shares for many years.

TC Energy will benefit from the nascent LNG buildout and the growth of data centers. Large capital projects will grow its free cash flow for years, allowing the company to deliver and create additional value for shareholders. We prefer TC Energy shares over those of Enbridge due to the ladders, lack of exposure to natural gas supply, and demand growth in North America. TC Energy offers a safe 5.1% dividend yield on its current stock price of $65.66, which is likely to grow as its free cash flow increases over the coming years.

Conclusion

Conservative investors who wish to sleep well with their energy stock holdings should consider buying all three high-quality names listed above. While they won’t earn the biggest upside amid a recovery, they will own names they can buy and forget about, allowing management to compound value and deliver free cash flow to shareholders. Investors who can buy at least a few percentage points below current prices are likely to be very pleased with the returns generated from these names over the next few years.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of TRP:CA either through stock ownership, options, or other derivatives.