By: Jon Costello

I’ve been investing in the energy sector since 2009, and I’ve never witnessed the kind of divergence that exists in today’s market. In short, the historical relationship between oil prices and global inventory levels has broken down to an extent I’ve never seen.

Oil prices have always exhibited a strong inverse correlation with oil inventory levels. Steadily growing inventories indicate that supply outstrips demand. Higher inventories imply more slack in the market. The converse is also true. Inventory declines indicate that supply is lower than demand.

Charts that plot oil prices versus inventory levels over time show a price line and an inventory line that are essentially mirror images of one another. Today, the mirror image has disappeared as both inventories and prices head lower. We're now at the point where global inventories are far too low for current oil prices.

Global Inventory Levels are Low

In point of fact, inventories currently stand at their lowest levels going back to 2017, as shown in this chart:

Source: Eric Nuttall, X, Nov. 7, 2024.

Recall that under normal circumstances, lower inventories imply higher prices. Historical price behavior bears this out. The higher inventory levels shown one, two, and three years ago on November 8 of 2023, 2022, and 2021 coincided with oil prices of $77, $89, and $81, respectively. These figures aren’t adjusted for inflation.

In all three years, inventories were higher than today's. Given their inverse correlation with prices, their prices should be lower and today's prices should be higher.

The relationship isn’t perfect. For instance, on November 8, 2022, an oil price of $89 was higher than the level implied by inventories. However, prices corrected in short order, ending the year at $79, in line with the levels implied by inventories.

In the past, the relationship has tended to break down temporarily, but it reasserts itself, typically over the course of a few weeks. Before today’s divergence, the most recent instance was in April, when bullishness regarding Middle East tensions caused oil to trade above the price implied by inventories.

In hindsight, this was a selling signal. Wilson and I used the opportunity to sell down a portion of our E&P holdings in anticipation of a reversion. Over the subsequent weeks, prices corrected, dropping back down to more “normal” levels.

Today’s price/inventory divergence has been in effect since August. This is far longer than any other instance I can recall.

At least so far, it shows no signs of letting up.

What Is WTI’s “Fair Value” Today?

Today’s divergence is far greater, longer lasting, and more persistent than anything I’ve experienced.

To determine its magnitude, we can reference the work of various analysts who have developed regression models to estimate the current “fair value” of WTI or Brent. Michael Rothman at Cornerstone Analytics, for instance, has a particularly good one.

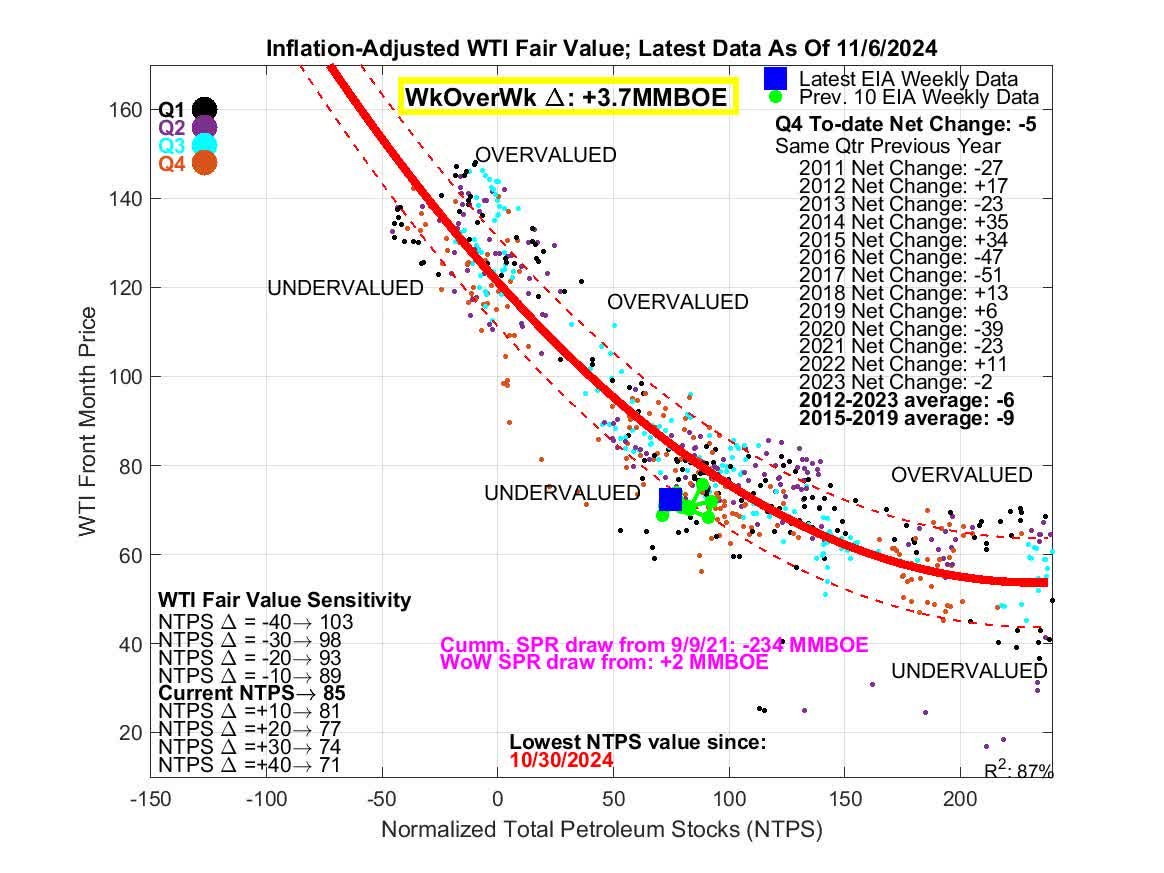

On X, the account handle @UndervaluedOnG publishes the results of a similar regression analysis after weekly U.S. inventory reports. The price-to-inventory data has an 87% fit. The theoretical maximum 100%, so this model does a good job correlating the two variables. Its output is typically in the ballpark with other models I’ve seen.

The chart below shows the data.

Source: @UndervaluedOnG, X, Nov. 6, 2024.

Now, there’s a lot going on in this chart, but suffice it to say that it estimates WTI’s “fair value” to be approximately $85 per barrel as of November 6.

WTI closed today’s trading session at $70.41 per barrel. Based on the modeled “fair value” estimate, WTI has nearly 21% upside from its current price.

Implications for the Oil Market

Trying to tease out the reasons why prices are so disconnected from inventories is so complicated as to be an exercise in futility. But we know enough to be highly confident that prices are seriously out of whack with fundamentals.

There are several implications of this fact.

First, we can state with confidence that there is no geopolitical premium in the oil price. In fact, one can argue that there exists a massive geopolitical discount.” Of course, this makes no sense given the hostilities underway in the Middle East and the non-zero chance that a mistake made by, say, the Houthis or some other aggressor group disrupts supply.

Another implication is that the current pricing is acting as a de facto price control. It’s an established principle of economics that when prices are kept too low, shortages emerge. Severe shortages create the potential for a price spike. With regard to today’s oil market, we can infer that if prices remain too low, inventories will be drawn down to the minimum levels at which refineries can operate. At that point, prices will surge higher.

If oil prices are held down for too long, a price spike is only a matter of time, though the comeuppance could be a long time coming. However, we’re seeing a key step in the process, namely, surging refinery margins, which occurred again today despite the ugly price action.

Another implication is that the lack of price response to supply and demand developments creates havoc for fundamental-based traders. Consequently, many—if not most—of significant size have exited the oil market.

In their absence, momentum-based algorithmic programs now dominate oil futures trading. A market increasingly dominated by momentum traders distorts the price discovery process. A distorted price discovery process forces even more fundamental-based traders out of the market, which causes more severe distortions, and so on. Prices are left to drift higher or lower with little fundamental justification.

This is not how markets are “supposed” to work. In the end, it’s bad for capital allocation and the long-term health of the market.

Implications for E&P Stocks

There are several implications for energy investing. I’m currently conducting my own energy investing program under the following assumptions.

Commodity economics dictate that, one way or another, oil prices will eventually reflect fundamentals.

E&P stock prices are highly correlated with oil prices.

When oil prices revert to their normal relationship with fundamentals, so will E&P stocks.

I don’t know when that reversion will occur.

The upside in E&Ps is enough to justify the wait.

My own interpretation of the price/inventory relationship is that it represents a margin of safety in the event that the demand reduction that so many investors fear does, in fact, arrive. In that scenario, supply can overshoot demand and cause inventories to build massively before fundamentals reflect today’s price.

This view of the situation gives me greater conviction to buy well-positioned E&Ps. Since I don’t know when the situation will resolve, I’m sticking with long-term investments that I estimate possess enough upside to justify waiting through stretches of volatility.

My favorite high-quality names are MEG Energy (MEG:CA), Cenovus Energy (CVE), and Suncor (SU). These stocks have all but eliminated debt as an existential risk. They’re safe in the face of the negative investor sentiment surrounding a potentially loose 2025 oil market supply/demand balances and lingering concerns about global oil demand.

Investors who are comfortable embracing more risk but also greater potential returns should favor E&Ps with more cash flow torque to commodity prices. Those with the biggest appreciation potential relative to their risk include Veren (VRN) and Strathcona Resources (SCR:CA). I hold both in the HFIR Energy Income Portfolio and in accounts I manage. Both names possess cash flow torque that I estimate could send their shares up more than 100% if oil prices rise above $85 per barrel, as I suspect they will over the next two to three years.

Prospective investors of Veren and Strathcona should keep in mind that cash flow torque works both ways. These stocks could underperform if commodity prices decline. Still, both will make it through nearly any realistic downturn scenario and prosper on the other side.

Risky micro-cap E&Ps will also outperform amid a reversion to historical norms, though these also entail a risk of permanent loss if oil prices are sustained at current commodity price levels or if prices fall lower. I’d avoid them for the time being.

Investor Sentiment is Playing a Role

Investor sentiment matters. Sentiment tends to follow price, so today’s low prices lead to dismal sentiment that deters investors from buying, thereby creating even lower prices. This dynamic has created bargain prices among many E&Ps. It’s what great energy stock buying opportunities are made of.

In the opposite fashion, an upswing in prices can beget even higher prices when fundamentals are supportive and sentiment begins to improve.

Even without a price rally, sentiment itself may be the spark that causes prices to rally. For instance, even the slightest improvement in the consensus view of 2025 supply/demand balances can dash many investors’ fears and send oil prices significantly higher.

Conclusion

Oil prices are too low. They currently discount a scenario in which severe demand weakness causes massive inventory builds. If these builds don’t occur, oil prices will increase significantly.

I’m actively buying E&Ps in this environment. I recommend that investors keep it simple and stay safe. MEG, CVE, and SU are no-brainers over a three-year holding period. Investors can buy with confidence that substantial gains are in store over that timeframe.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of CVE, SU, SCR:CA, VRN either through stock ownership, options, or other derivatives.

How does this account for the ever decreasing marginal cost of production?

Jon, thanks for the writeup. It makes a lot of sense. My question is how you see the prices of the companies you suggest for investing relative to current and "expected" oil prices going forward (based on the futures strip). If they are cheap to market implied prices then investing in the stocks of those companies makes sense. However, if the companies look expensive then I would be better off taking a position directly in the oil market. How do you see things?