(Ideas) California Resources

Editor’s Note: CRC is not in the HFI Portfolio. Ideas from HFI Research is a separate paid subscription from HFI Research.

By: Jon Costello

California Resources Corp. (CRC) emerged from bankruptcy in October 2020 as a conservatively financed E&P with the same portfolio of attractive conventional assets. During the bankruptcy process, the company’s lenders exchanged $4.4 billion in debt for equity and provided $1.4 billion in exit financing. Fresh-start accounting revalued its assets and liabilities.

Since then, CRC has been well-managed for its shareholders. It has increased production to a level where future growth is unlikely, but the larger scale allows for profitable operations even at relatively low oil prices.

CRC expects to produce 136,000 boe/d of oil and natural gas in the second half of the year. About 79% of the company's production is expected to be crude oil, 14% natural gas, and 7% NGLs.

One of CRC’s key features is its low decline rate. Without extra investment, its production would decrease by 10%-13% each year. With investment, management says they have lowered the company’s annual decline to about 6%.

The standout feature for CRC shareholders has been the company’s capital allocation. Since the company launched its share repurchase program in May 2021, it has repurchased 24.0 million shares, representing 28.8% of the 83.3 million shares outstanding as of December 31, 2021, following its exit from bankruptcy. CRC purchased the shares at an attractive average price of $43.37 per share. In addition to share repurchases, it also paid $323 million in common dividends over the same period.

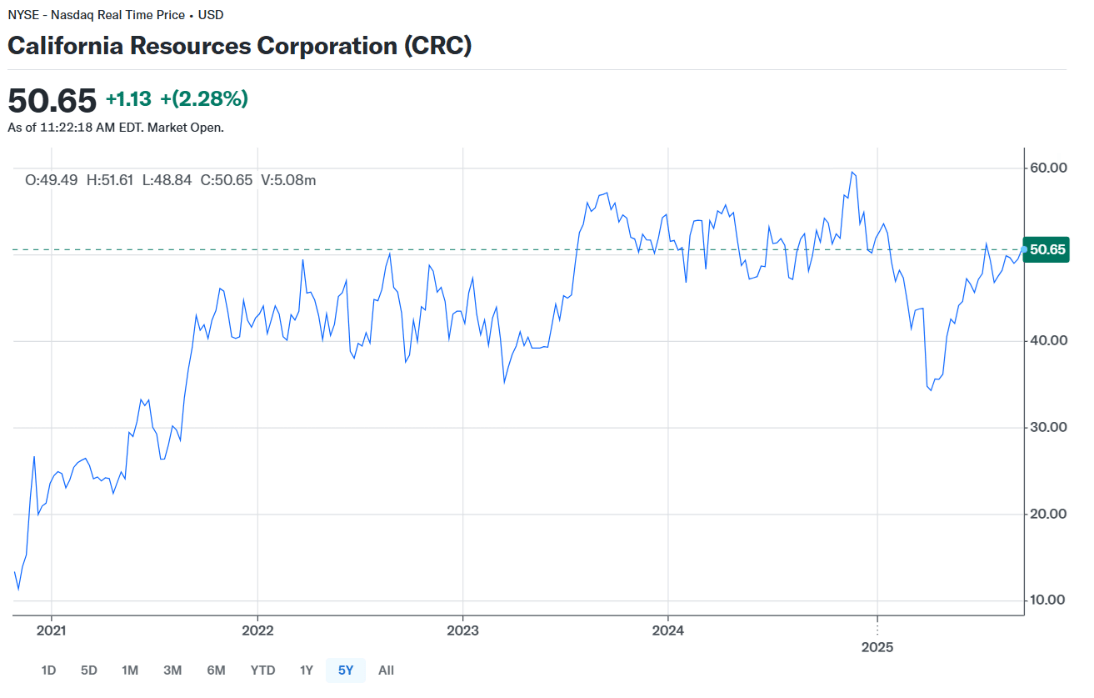

CRC’s share price has remained stable over the past few years, despite trading through both low and high commodity price regimes.

Source: Yahoo! Finance, Sept. 9, 2025.

The company has maintained a one-rig drilling program and recently added a second rig in Kern County in late June. If regulatory and permitting issues are resolved, it can expand to as many as eight rigs in the county.

CRC benefits from pricing its oil off the Brent benchmark, which trades at a premium to WTI. CRC realizes approximately 97% of Brent on its crude oil production.

CRC’s NGLs and natural gas production also benefit from premium pricing. Its realized NGL prices are in the mid-60% range relative to Brent compared to the mid-40% range for other North American producers. Natural gas realizations typically range from 100% to 110% of Henry Hub prices. The company’s premium pricing is due to California’s status as an energy island, with limited transportation to domestic supply hubs.