(Idea) Western Midstream Partners Is A Buy After Its Deal With Occidental Petroleum

By: Jon Costello

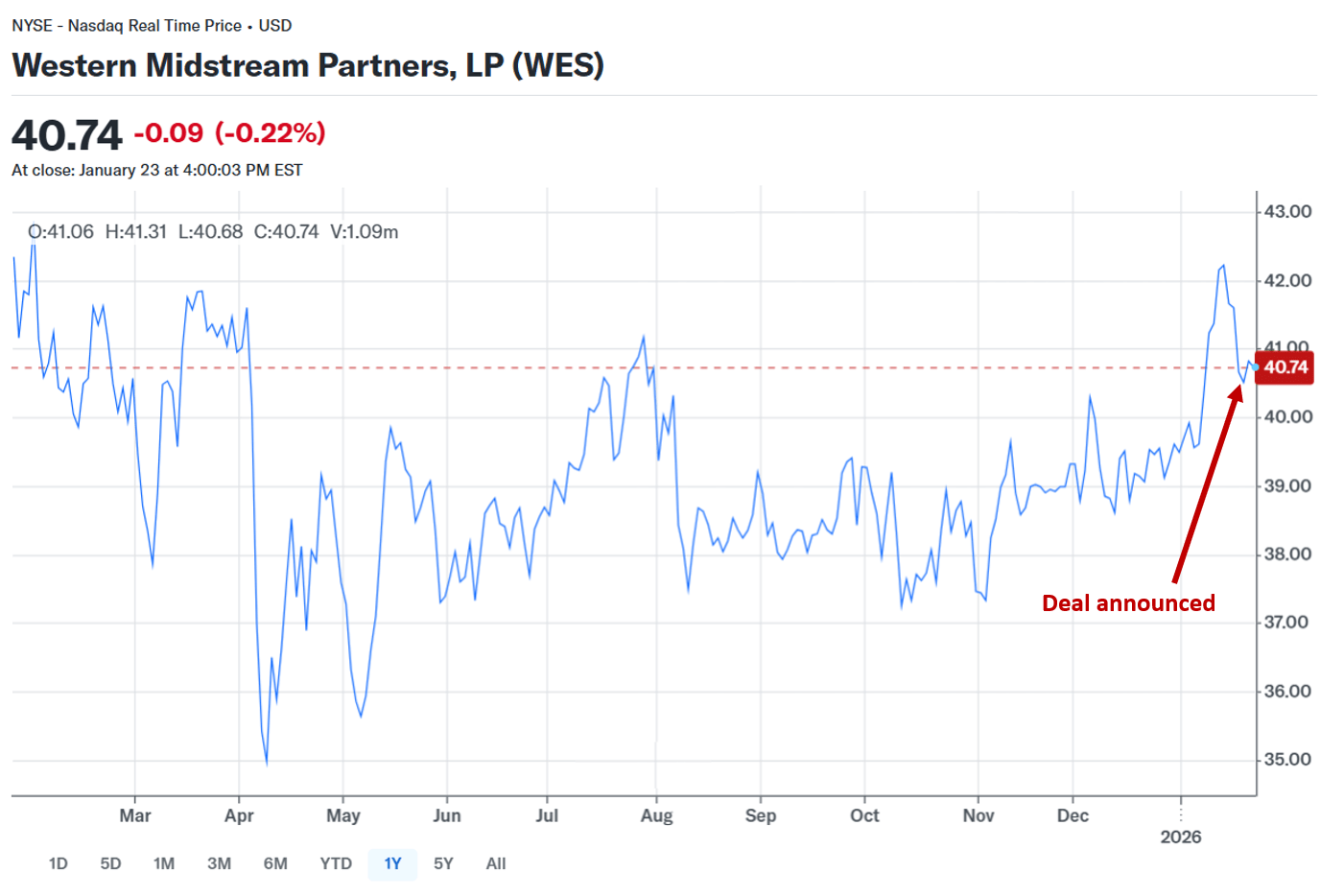

Western Midstream Partners, LP (WES) units have been depressed in recent months due to concerns about the company’s midstream services contract reset with its former sponsor, Occidental Petroleum (OXY). Investors had been concerned that OXY would tip the scales heavily in its favor, potentially dealing a blow to WES’s long-term cash flow outlook. These concerns weighed on WES’s unit price, which traded at an EV/EBITDA multiple below what its high-quality management, operations, and growth prospects would support.

The overhang was caused by uncertainty over whether the economics of WES’s Delaware Basin midstream agreements with OXY, its sponsor, would change adversely for WES, dealing a blow to its cash flow. WES’s old cost-of-service contract for OXY’s Delaware Basin acreage was structured at above-market rates. The contract’s expiration introduced the risk to WES unitholders that rates would be set lower when they came up for renewal, which, of course, would presumably be bad for WES units.

On January 20, WES announced that it had reached a deal with WES pertaining to its Delaware Basin midstream services agreement. The deal resets WES’s contract structure and cash flow prospects, while keeping its per-unit metrics intact. Importantly, it removes the uncertainty overhang that caused WES units to trade at a discount. We view the deal as a net positive for WES unitholders.

The agreement is effective through the mid-to-late 2030s. It also includes minimum-volume commitments (MVCs) and natural gas processing commitments that protect WES’s volumes through 2035.

We bought WES units on weakness late last year. We did not know when this contract would be renegotiated, but we were confident that any negotiation would put WES on solid footing, setting it up for throughput growth and, potentially, growth through accretive acquisitions. We believe WES units are well positioned for multiple expansion due to the company’s high-quality assets and management.

In my experience covering the midstream sector, midstream service contracts between a sponsor and its midstream affiliate are typically resolved in a way that supports the midstream entity. For example, in 2022, MPLX (MPLX) achieved a favorable outcome for its master services agreement, which covered major long-haul pipelines with its sponsor, Marathon Petroleum Corp. (MPC). Like WES’s Delaware Basin gathering and processing assets, MPLX’s pipelines subject to this contract accounted for a substantial portion of its Adjusted EBITDA. The favorable outcome de-risked its cash flow, spurred credit upgrades and more favorable borrowing terms, and eventually cleared the way for a higher unit price.

Alternatively, in situations where the sponsor seeks to extract greater value from the midstream entity without offering corresponding value in return, the sponsor typically acquires the midstream entity. This has been an ongoing trend for years, and it is the course I eventually expect Chevron (CVX) to pursue with Hess Midstream (HESM).

WES units have not reacted positively to the announcement, creating a buying opportunity for long-term accounts.

Source: Yahoo! Finance, Jan. 24, 2026.

At their current price, WES units offer a safe 9% distribution yield, long-term distribution growth prospects, and attractive capital appreciation potential from their current price of $40.74.

The Deal

Under WES’s previous cost-of-service contract, its fee was set by reference to the cost of its services plus a specified return. Such cost-of-service midstream contracts entail risk for an E&P operator, as its midstream rates can drift higher as costs increase or volumes decline. An E&P that controls its midstream can mitigate this risk by shifting future value from the midstream entity to itself, hence investors’ concerns regarding WES. OXY’s Delaware Basin agreement with WES was its largest cost-of-service midstream agreement, so it had a strong incentive to renegotiate rates downward.

In fact, WES’s latest deal does convert value to OXY by switching the contract’s Delaware Basin cost-of-service rates to a fixed-fee structure. In its press release announcing the deal, WES states that “The cost-of-service model was instrumental in safeguarding cash flows during our substantial investment in building WES’s Delaware Basin gathering system. As the basin has matured, transitioning to a simplified, fixed-fee structure is both logical and timely.”

However, negative impacts to WES unitholders are mitigated by the consideration paid by OXY. That consideration takes the form of 15.3 million WES units to be transferred to WES, representing approximately $610 million. The transfer effectively offsets the negative impact of the change from cost-of-service to fixed-fee contract structure on WES’s free cash flow per unit. The company expects the change in the contract structure to have a minimal impact on Adjusted EBITDA.

Simultaneously with its deal with OXY, WES also announced an agreement with ConocoPhillips (COP) to provide gathering and processing of a portion of COP’s Delaware Basin natural gas production. The deal is also fixed-fee with acreage dedication extending through the early 2030s. This deal will also help mitigate the change in contract structure while diversifying WES’s related-party business.

A Win-Win Deal

This deal is a win-win for both WES and OXY.

Clearly, the new contract terms aren’t a game changer for OXY. But the new contract is a net positive for the company, as it marginally increases its free cash flow generation prospects and, by extension, its intrinsic value. While the news won’t be material for moving OXY’s stock, it does offer subtle benefits that move the needle in a positive direction for OXY shareholders.

Under the deal, OXY secures lower midstream costs in the Delaware Basin, thereby enhancing the economics of its production in the basin. OXY’s margins and returns receive an incremental boost from improved well economics. The higher return translates into a higher net present value for OXY’s Delaware operation. Since OXY exchanged WES units as compensation, the deal will be accretive to OXY as long as its reinvestment returns exceed the cash distribution yield on WES units at the $39.86 per unit sale price, or 9.2%. Returns to OXY should exceed that rate, particularly at the higher oil prices we expect will prevail in 2027 and beyond.

OXY will also benefit from paying a fixed midstream fee, making its cash flow more predictable relative to its previous cost-of-service contract.

The main negative for OXY in the deal is the MVCs it provided WES. If OXY ever wants to reduce drilling activity or shift its development plans, MVCs could become a constraint. Offsetting this negative is that the MVC bolsters the value of WES units, supporting OXY’s 41% ownership of WES units after the deal.

For WES, the deal keeps per-unit cash flow and Adjusted EBITDA prospects stable, while removing the uncertainty overhang from WES units. As such, it makes WES’s future cash flows more predictable, setting the stage for WES units to trade at a higher multiple.