(Idea) Venture Global

By: Jon Costello

Venture Global VG 0.00%↑ is one of three large publicly-traded U.S. LNG companies. Its peers are Cheniere Energy LNG 0.00%↑ , the operator of Sabine Pass and Corpus Christi export facilities, and NextDecade NEXT 0.00%↑, a development-phase company set to begin exports in 2027 from its Rio Grande LNG facility. Among U.S. LNG exporters, only Cheniere and VG currently produce at commercial scale.

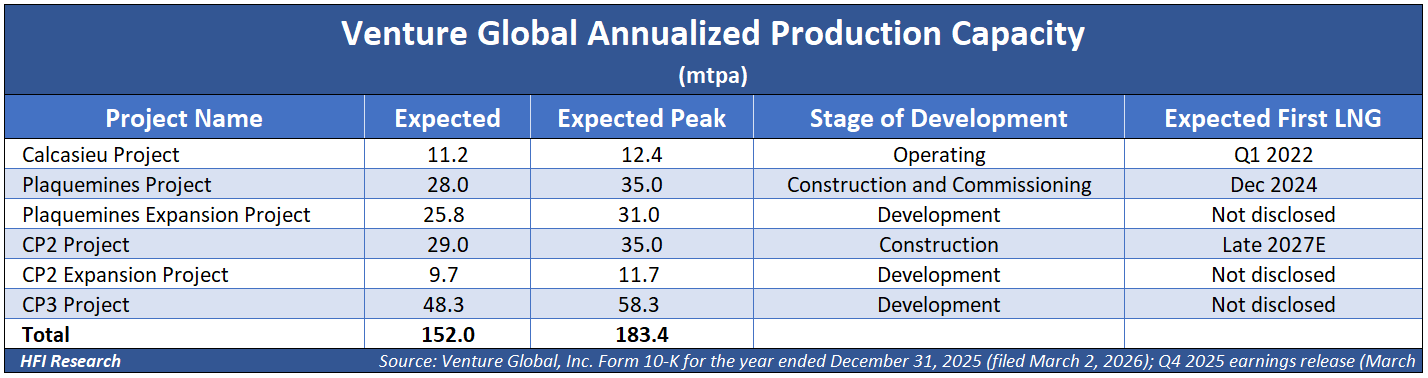

VG owns two liquefaction facilities on the Louisiana Gulf Coast: Calcasieu Pass, which declared commercial operations in April 2025, and Plaquemines, which is currently in commissioning. Plaquemines Phase 1 is expected to reach commercial operations in the fourth quarter of 2026 and Phase 2 in mid-2027. The company has a third facility, CP2, a $33 billion greenfield project that received final investment decision (FID) in July 2025, is under construction, and expected to commence LNG production in late 2027. Beyond these, VG has expansion projects at both Plaquemines and CP2, as well as a separate greenfield project, CP3, in early development.

VG’s competitive edge is its construction speed and modular cost discipline. Rather than using two or three large liquefaction trains as older U.S. projects did, VG uses dozens of smaller, factory-built mid-scale trains that can be installed sequentially. Its first facility, Calcasieu Pass (CP1), went from FID to first cargo in roughly 30 months, a timeline the company bills as the fastest FID-to-first-cargo for a greenfield U.S. LNG project.

VG also owns a fleet of seven LNG tankers with two more on order, bringing the total fleet to nine. This lets the company ship its own cargoes to wherever in the world LNG prices are highest. Most of its U.S. peers sell at the Gulf Coast dock and let the buyer profit from shipping the LNG overseas. To the extent VG’s facilities produce more LNG than their contracted nameplate capacity, the company can use its own tanker fleet to capture spot prices on those excess volumes.

CP1 is currently producing at roughly 11.2 million tons per annum (mtpa), about 12% above its 10 mtpa nameplate capacity, thanks to the same modular design that enabled fast construction. As Plaquemines completes commissioning, VG’s consolidated output will climb to approximately 40 mtpa by the time both of its phases reach commercial operations. The table below summarizes VG’s full project portfolio.

Investors should avoid VG shares at the current price. My concerns center on three areas: the company’s deteriorating margin economics, its slow-to-deleverage balance sheet, and management practices that, in my view, put minority shareholders at risk. The sections that follow walk through each in turn.

From an economics perspective, revenue tied to spot pricing will wind down as contracted SPAs replace it, compressing margins even as total LNG production volumes rise. The balance sheet is an issue because leverage peaks in 2026, and only the bull-case EBITDA scenario fully deleverages the company back toward 2025 levels by 2028. And management’s conduct toward VG’s contracted counterparties and IPO disclosure practices raises questions about how this team is likely to treat minority shareholders when their interests diverge from its own.