(Idea) U.S. Coal Stocks Best Positioned For A Prolonged LNG Supply Disruption

By: Jon Costello

Most commentary on the Iran war has focused on oil. This is understandable due to the oil market’s central role in the global economy and its direct impact on consumers. WTI’s spike from the low-$60s per barrel before the war to $113 shortly after it began, and other events, like the strategic petroleum reserve release, immediately captured public attention.

But an often overlooked trade involves a commodity that gets far less attention: LNG. I’ve followed this market closely as a holder of Cheniere Energy (LNG) since January 25, 2021. Cheniere’s ability to sell cargoes at spot pricing through its marketing of uncontracted production makes it an obvious direct beneficiary of today’s high LNG prices.

Direct LNG plays have been bid up to prices that I believe make them unattractive for long-term holding. But there are secondary plays that benefit from the fact that LNG has no substitutes available at scale, barely any strategic reserves, and no spare global capacity. The most obvious is thermal coal, the only realistic backup fuel for LNG in power generation.

Energy expert Dr. Anas Alhajji recently commented on the bullish prospects for thermal coal, noting its use as a substitute for LNG.

Source: Anas Alhajji, X, March 15, 2026.

The thermal coal market was already tightening before the war. The Iran conflict has accelerated a recovery that was underway. Due to the war’s impact on LNG and the prospect for sustained higher coal prices, thermal coal names are worth considering for investors who expect a prolonged disruption in the Strait of Hormuz and/or continued LNG supply outages.

Impacts on LNG From the War In Iran

The closure of the Strait of Hormuz to commercial shipping in early March shut off roughly 20% of the world’s LNG supply. The world’s largest LNG exporter, Qatar, declared force majeure on its contracts after Iranian drone attacks damaged gas facilities. The attacks also forced QatarEnergy to halt all gas production. A full restart of LNG production will take at least a month, and likely longer.

Whereas oil supply has partial mitigants amid a sustained disruption, such as SPR releases, Saudi and UAE pipeline rerouting, and demand destruction, LNG has none. In fact, U.S. export terminals are already running at or near maximum capacity.

More recent developments further support coal as an LNG substitute. For one, yesterday’s Iranian missile strike on Qatar’s Ras Laffan Industrial City has materially worsened the outlook for LNG supply. QatarEnergy confirmed that the attack damaged two of its 14 LNG trains and a gas-to-liquids facility, taking 17% of Qatar’s LNG export capacity offline for more than three years. The offline capacity represents approximately 12.8 million tons per year. The loss of this capacity would put a severe dent in the looming LNG oversupply that kept me away from other LNG investments. Damage to the Qatar facility is the first sign that the war in Iran has caused more than just a temporary disruption that takes a few weeks to restart. If QatarEnergy’s reports of the damage and repair times are accurate, it represents a structural removal of supply from the global LNG market.

This event has significant implications for thermal coal. Long-lasting damage to Qatar’s LNG supply means that the gas-to-coal substitution trade, which was previously contingent on the duration of the Strait of Hormuz closure, now has a multi-year floor underneath it regardless of whether the Strait reopens. Asian and European utilities that were hedging against a short-term LNG outage may now be forced to secure baseload fuel alternatives for 2027 and beyond, and seaborne thermal coal is the only commodity available at the necessary scale. Newcastle thermal coal prices will likely trade higher after this event.

Coal Substitution

When natural gas becomes unavailable or prohibitively expensive, power generators switch to coal. We saw this in 2022 during the Ukraine crisis, when Russian pipeline gas to Europe was curtailed, and Newcastle thermal coal prices spiked to nearly $400 per ton.

The current disruption is different in several ways. The 2022 ordeal disrupted Russian coal supply, creating a dual shock to both natural gas and coal markets. The war in Iran has not directly disrupted coal supply; it has only removed LNG from the market. This means the coal price increase should be more moderate than in 2022, absent a dramatic escalation. At the moment, Newcastle thermal coal is trading around $132 per ton, up more than 30% year-over-year but far below the 2022 peak.

However, the LNG disruption is arguably more acute. Qatar accounted for approximately 20% of global LNG, and there is zero spare capacity anywhere in the world to replace it. Before the strike on Qatar’s LNG facilities, Morgan Stanley estimated that Japan, South Korea, and Taiwan alone could require an additional 1.5 to 2 million tons of thermal coal imports per month if the Qatari outage persists, an 8% to 10% jump in import demand from those three countries alone. Yesterday’s disruption will further increase their import demand.

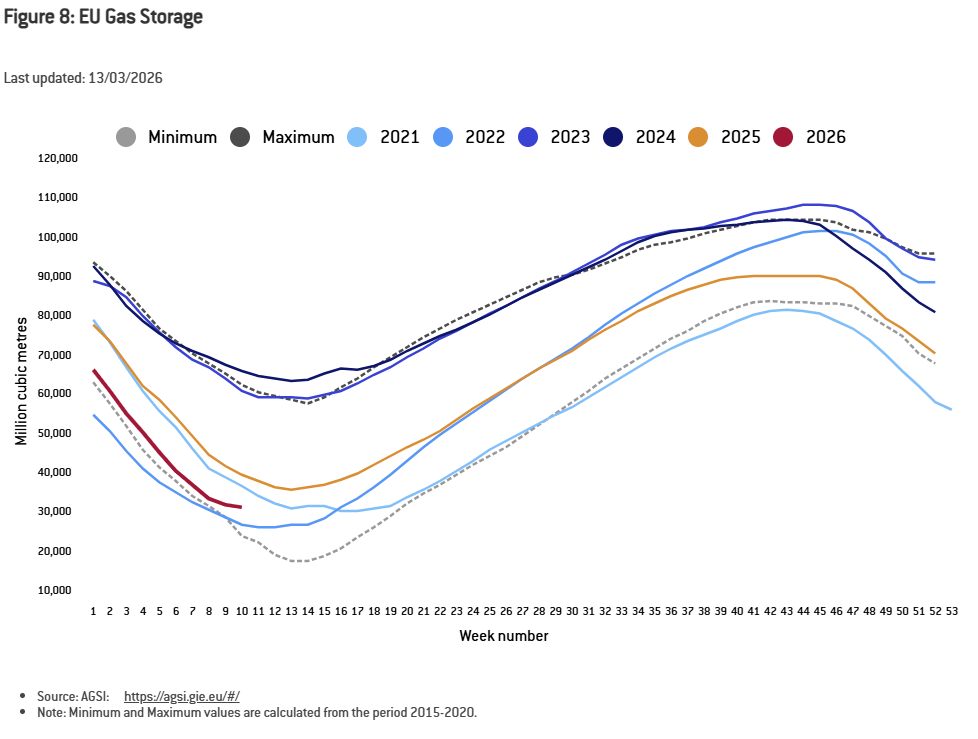

Europe is also vulnerable. European gas storage levels started 2026 at just 50 billion cubic meters, or roughly 46% full, versus 63 Bcm in 2025 and 77 Bcm in 2024.

Source: CEEnergy News, March 13, 2026.

European natural gas prices nearly doubled following Qatar’s declaration of force majeure. A UBS report noted that the market has not yet fully priced the gas-to-coal substitution trade into coal equities.