(Idea) Tronox - Multi-Bagger Potential From A Titanium Dioxide Market Recovery

Please be sure to read our primer on the chemical sector and the titanium dioxide market.

By: Jon Costello

Tronox Holdings’ (TROX) fourth-quarter 2025 results point to a recovery in its earliest stages, with volumes clearly inflecting higher and prices lagging.

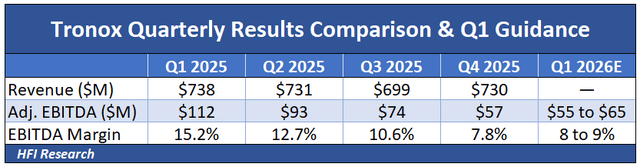

The company’s fourth-quarter revenue came in at $730 million, up 8% year over year and 4% from the previous quarter. The performance was driven almost entirely by higher sales volumes, which increased by 13% from the previous quarter. The result was ahead of management’s expectation of a 3% to 5% improvement. Meanwhile, Zircon volumes were up 27% year-over-year and 95 from the previous quarter.

The volume outperformance was driven by activity in India, Latin America, and the Middle East, where antidumping duties against Chinese imports have created opportunities for non-Chinese producers to gain lasting market share.

While the fourth-quarter volume recovery was real, it was met with continued pricing deterioration. Titanium dioxide prices declined roughly 8% from the fourth quarter of 2024, while Zircon prices declined by 23% over the same period.

The result of the higher volumes and lower price was Adjusted EBITDA of $57 million on a 7.8% margin, down 56% from $129 million in the year-ago quarter. Full year 2025 EBITDA was $336 million, down 40% from $564 million in 2024, on revenue that declined by only 6%. Quarterly results are shown in the table below.

The table shows that Adjusted EBITDA margins deteriorated in each quarter of 2025, even as volumes recovered in the second half of the year. Pricing was the culprit, compounded by cost headwinds from lower mining and upgrading rates, resulting in a collapse in fixed-cost absorption. The company also reported $233 million in restructuring charges for the closures of its Botlek facility in the Netherlands and its Fuzhou facility in China, though these were excluded from the adjusted figures.