(Idea) Tourmaline Scores With Its Crew Energy Acquisition

Earlier today, Tourmaline Oil (TOU:CA) proved yet again that it’s one of the best-managed natural gas-weighted operators in North America. The company announced a masterful acquisition of Crew Energy (CR:CA), an independent intermediate E&P operating across 220,000 acres in the Montney play in Alberta.

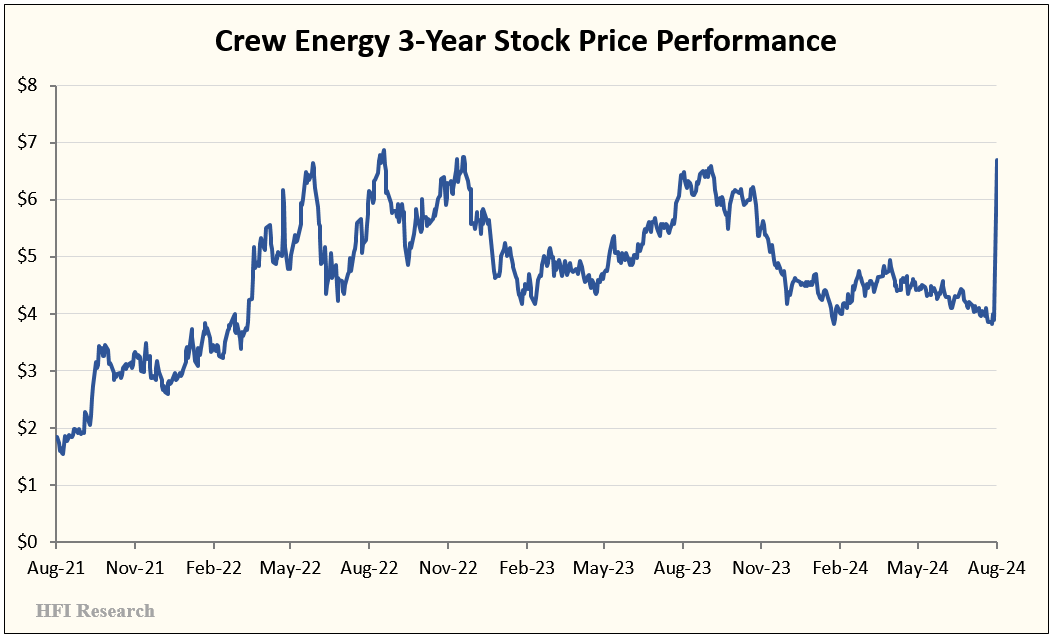

TOU’s all-stock bid values Crew at $1.3 billion and includes the assumption of $240 million of Crew’s net debt. The deal metrics work out to $6.69 per Crew share, a 72% premium over Crew’s closing stock price as of Friday and the highest price for the shares since December 2022. Crew shareholders will receive 0.114802 TOU shares for every Crew share they own. In connection with the deal, TOU will issue 18.778 million shares, adding 5.3% to its 355.4 million share count at the end of the second quarter.

The deal is a win-win for Crew and TOU shareholders. Crew shareholders receive an offer price close to a cyclical high and a massive premium over Friday’s closing price. TOU shareholders stand to benefit from Crew’s operational and strategic fit with TOU’s legacy acreage and infrastructure.

The market cheered the deal. Tourmaline’s shares traded 4.2% higher after today’s announcement, to $60.73. The deal sparked a rally in other Canadian gas-weighted intermediate E&Ps as investors used the deal’s metrics to imply that Crew’s peers were undervalued.

The deal is TOU’s latest since it acquired Bonavista Energy for $1.5 billion last November. It continues TOU’s consolidation of the Northeast British Columbia Montney fairway at cyclically low Western Canadian natural gas prices.

For years, TOU had pursued Crew only to be rebuffed as Crew was not for sale. This summer, however, after Crew stock had dismally underperformed peers, its board had a change of heart and began to entertain bids. After receiving several competing offers, it agreed to be acquired by TOU.

The deal’s timing was outstanding for TOU, as it came just as Crew shares plumbed multi-year lows.

Assuming the deal closes as expected in October, TOU management expects its 2024 production to average 587,500 boe/d, above its previous guidance of 580,000 boe/d. Production will be weighted approximately 75% to natural gas and 25% to liquids.