(Idea) TotalEnergies - The Risks Outweigh The Dividends

Message from Jon:

Dear Subscribers,

I'll be taking a week off to spend some time with my family in Vermont. I'll have access to the internet, so feel free to contact me. I'll be back the following week.

Hope you're having a wonderful summer!

Sincerely,

Jon

By: Jon Costello

We are always on the hunt for attractive energy equity investments. I was initially intrigued by TotalEnergies' (TTE) outsized dividend yield. Our commodity price outlook is cautious for oil for the next few quarters, and I figured TTE's outsized dividend yield would be an attractive vehicle for navigating potential stormy macro conditions.

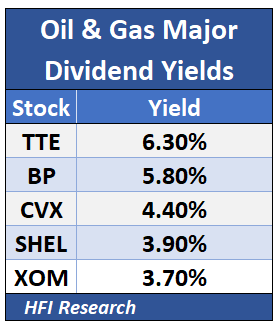

After all, TTE’s dividend stands well above its global oil and gas major peers, at 6.3%.

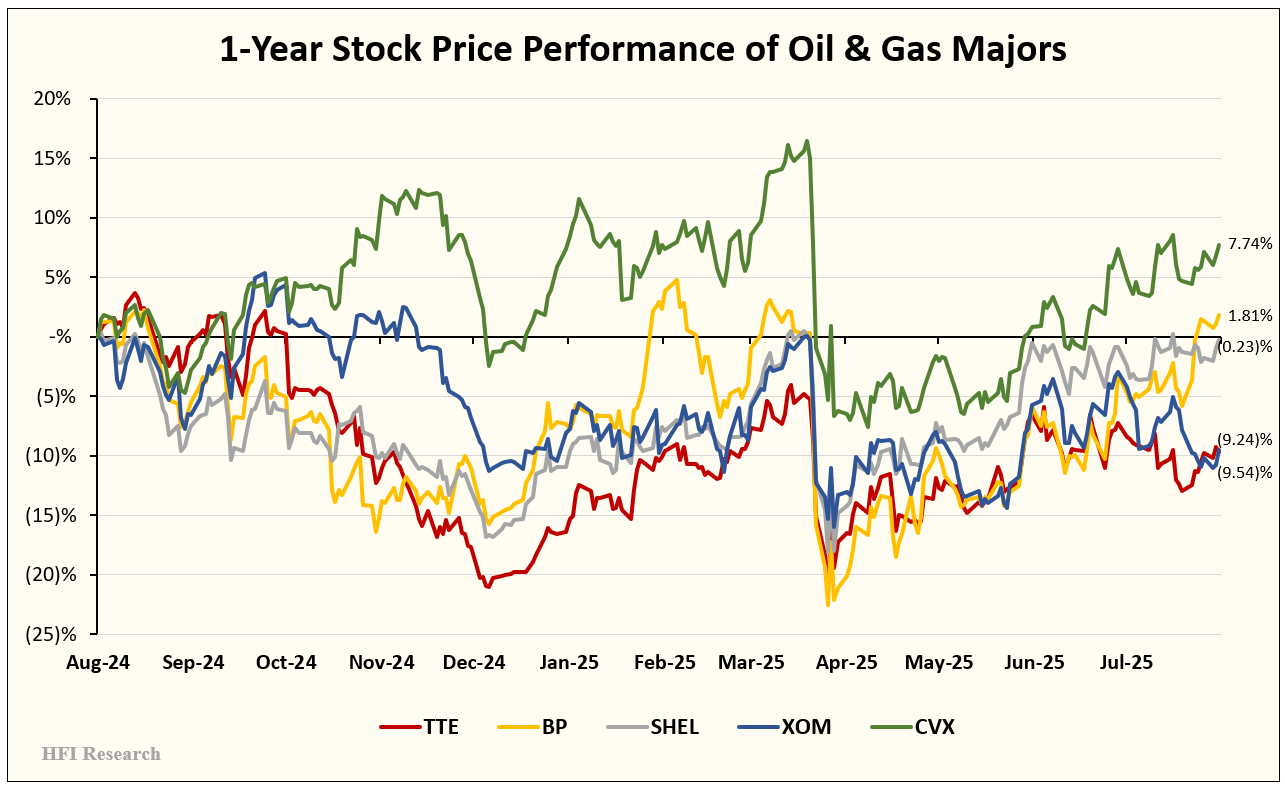

Not surprisingly, the high yield is partly a function of an underperforming stock.

But the picture became more concerning when I looked under the hood.

First, TTE’s financial results have notably fallen behind those of its peers. This has been the main cause of the company’s share price underperformance.

However, from an investor’s perspective, the implications of management’s aggressive expansion into wind and solar power generation are equally concerning.

While TTE’s peers, such as BP (BP), Shell (SHEL), and Equinor (EQNR), have significantly slowed their renewable investments, TTE has fully embraced renewables. Based on the performance of other solar and wind projects in the U.S. and Europe, TTE’s strategy carries considerable risk for long-term shareholders.