(Idea) Strathcona Resources (Part 1 and 2)

Editor’s Note: Strathcona Resources is our favorite E&P pick for the incoming oil bull cycle. The article below was first published to HFI Research main subscribers on Dec 14, 2023 and March 7, 2024. Market data will be different than today, so please take that into account.

Part 1

Note to readers: Dollar references are to Canadian dollars unless otherwise specified.

For years, Strathcona Resources (OTCPK:STHRF) (SCR:CA) has flown under the radar in the Canadian oil patch. It was a private company that pursued rapid growth through an idiosyncratic acquisition strategy, which involved pursuing complex special situations to cobble together a heavy oil giant that is now the fifth-largest E&P in Canada.

Like all Canadian E&Ps, SCR shares have sold off with the recent plunge in oil prices. We believe they represent an attractive long-term buy among E&Ps. We value the shares at $30 and expect that value to grow over time under the stewardship of the Waterous family.

Strathcona’s Idiosyncratic History

Until it came public in October, SCR had been a privately owned E&P investment vehicle for Waterous Energy Fund (WEF), a private equity firm founded in January 2017 by Adam Waterous. SCR is the kind of company where prospective investors have to understand its history to appreciate its current operations, value, and likely future course. However, readers not interested in the corporate history can skip ahead to the next section.

Executive Chairman Adam Waterous is SCR’s architect. After a stint as a McKinsey & Co. consultant, he entered the oil and gas business in 1991 by founding Waterous & Co., an oil and gas mergers and acquisitions advisory boutique, with his brother Jeff.

In 2005, Waterous & Co. was sold to Scotiabank in 2005, at which point Adam became the head of Scotiabank’s global investment banking business. He left the bank in January 2017 to start the WEF.

WEF was founded as a private equity vehicle to acquire oil and gas assets. Waterous believed in the long-term oil bull thesis and viewed the depressed prices after 2014 as an attractive buying opportunity. He got right to work in building WEF’s suite of assets, focusing primarily on low-decline heavy oil assets in Western Canada.

The following is a timeline of the WEF’s acquisitions under Adam Waterous’ leadership.

January 2017: WEF buys condensate-rich natural gas assets producing 5,000 boe/d in the Kakawa area of the Montney out of creditor protection. Waterous names the entity Strath Resources.

April 2017: WEF acquires 67.1% of the common shares of Northern Blizzard Resources for $244 million from U.S. private equity firms Riverstone Holdings and NGP Capital Management. Northern Blizzard produced heavy oil, mostly in Saskatchewan. After the acquisition, WEF changes the company’s name to Cona Resources.

May 2018: WEF acquires the remaining outstanding share of Cona Resources for $85 million.

June 2018: Strath Resources acquires Paramount Resources’ Resthaven/Jayar assets in the Montney for $340 million. Consideration was 50% cash and 50% Strath common shares, as well as warrants to purchase Strath shares. After the transaction, Paramount owned 15.6% of Strath Resources.

June 2018: WEF raises $1.4 billion in its first private equity funding, with a mandate to invest in energy assets either in Canada or the U.S. Investors included pension plans, insurers, family offices, and university endowments. The fund’s potential targets included special situations, including restructurings and distressed energy assets in the range of $300 to $500 million.

January 2020: Cona Resources acquires Pengrowth Energy, a 35,000 boe/d heavy oil producer and owner of the Lindbergh heavy oil project near Cold Lake, for $740 million. The acquisition was funded through $585 million of equity and $155 million of debt.

August 2020: Strath Resources and Cona Resources merge to create a $1 billion enterprise, the largest wholly-owned private equity oil and gas producer in North America. Strathcona becomes the WEF’s sole operating company, producing 60,000 boe/d with 67% liquids with a 40-year reserve life. The rationale behind the tie-up was to have Strath’s condensate production hedge Cona’s heavy oil input costs.

Mid-2020: Acquired a 45% interest in private Osum Production, a troubled owner of Cold Lake oil sands assets, from Blackstone Group (BX), Warburg Pincus, and Singapore’s GIC sovereign wealth fund for an undisclosed sum. Osum produced approximately 20,000 boe/d. Osum’s owners had invested more than $770 million into it since 2008, and the company had acquired the Orion oilsands asset from Shell (SHEL) for $325 million in 2014.

November 2020: WEF launches a takeover bid to acquire 40% of Osum Oil Sands’ outstanding common shares. Osum had remained a private company. Some Osum shareholders had sought an exit and supported the deal, though others considered the offer too low and fought it. The deal closed in June 2021 after WEF increased its offer price. WEF’s acquisition price per Osum share was less than a quarter of the price implied by previous funding rounds.

June 2021: WEF combines Strathcona Resources and Osum Oil Sands Corp. The combined entity continued under the name Strathcona Resources. Strathcona remained 100% owned by the WEF, its investors, and Strathcona employees. At the time, it produced 80,000 boe/d of 75% liquids and had a proved and probable reserve life of 60 years. In the deal, Strathcona secured a $1 billion credit facility from a syndicate of Canadian and international banks to facilitate additional expansion. This is the point at which SCR begins to look like it does today. The company had its three operating segments intact. These included its Cold Lake thermal, Montey condensate-rich natural gas, and Saskatchewan heavy oil segments.

January 2022: Strathcona acquires Tucker thermal oilfield assets from Cenovus Energy (CVE) through a company called Stickney Resources for $800 million. Tucker produced approximately 20,000 boe/d.

March 2022: WEF closes on its fourth equity capital raise, raising $345 million to fund the acquisition of Caltex Resources, a producer of 13,000 boe/d of heavy oil in Alberta and Saskatchewan using enhanced oil recovery techniques. After the acquisition, WEF merges Caltex with Strathcona and increases the combined entity’s credit facility to $1.5 billion.

August 2022: Strathcona acquires private-equity-backed Serafina Energy for $2.3 billion, funding the deal mainly through borrowings on its revolving credit facility. Serafina produced 40,000 boe/d in Saskatchewan. The deal brought Strathcona’s total production to approximately 115,000 boe/d.

Pipestone Deal Brings Strathcona Public

On August 1, 2023, Strathcona and publicly-listed Pipestone Energy announced a deal in which Strathcona would exchange 9% of its equity for all Pipestone common shares. Pipestone produced approximately 37,000 boe/d of light oil and condensate. A large part of Pipestone’s value was that one-third of its production was condensate, which had tended to trade at a premium to WTI. Condensate is particularly valuable as a diluent for bitumen, which comprises a large part of SCR’s production. The competition between oil sands operators for condensate supply has pushed up its price, increasing production costs for major oil sands producers.

SCR’s all-stock offer valued Pipestone at around $2.70 per Pipestone share. Since this was only a small premium to Pipestone shares, which had been trading in the mid-$2 range.

Many Pipestone shareholders believed the offer significantly undervalued the company due to its large reserve value, premium condensate pricing, and growth prospects. Some voiced their concerns in public, making the deal contentious on the Pipestone side. Still, SCR had already won the support of Pipestone's management and board, making the deal likely to occur.

The Pipestone shareholders had a point. Valued on a per-flowing-barrel of oil equivalent basis, SCR's offer came at $26,000, well below other recent Montney deals, most of which were made at $40,000 to $60,000. Other Pipestone shareholders believed Pipestone’s assets were better suited for a large operator. They were also glad to participate in Strathcona’s upside, as Pipestone provides SCR with condensate to hedge its heavy oil production.

Ultimately, SCR’s bid carried the day. The price SCR paid was very attractive for its shareholders. The deal closed on October 3, after the end of the third quarter. Consequently, it has yet to publish quarterly financial documents on the combined entity.

With the Pipestone deal complete, Strathcona became the fifth largest oil producer in Canada, producing 185,000 boe/d with a market cap of $8.6 billion and an enterprise value of $11.5 billion.

We should touch upon a final incident in SCR's timeline that isn’t company-related but could sway investor opinion of SCR and its leadership nonetheless. In late October 2023, Adam Waterous became the target of an apparent smear campaign sparked by a backlash over his efforts to reform the board of the Banff Centre for Arts and Sciences. We investigated the incident and believe the allegations against him are false and ridiculous. The incident does nothing to change our positive view of Adam Waterous.

The New Strathcona

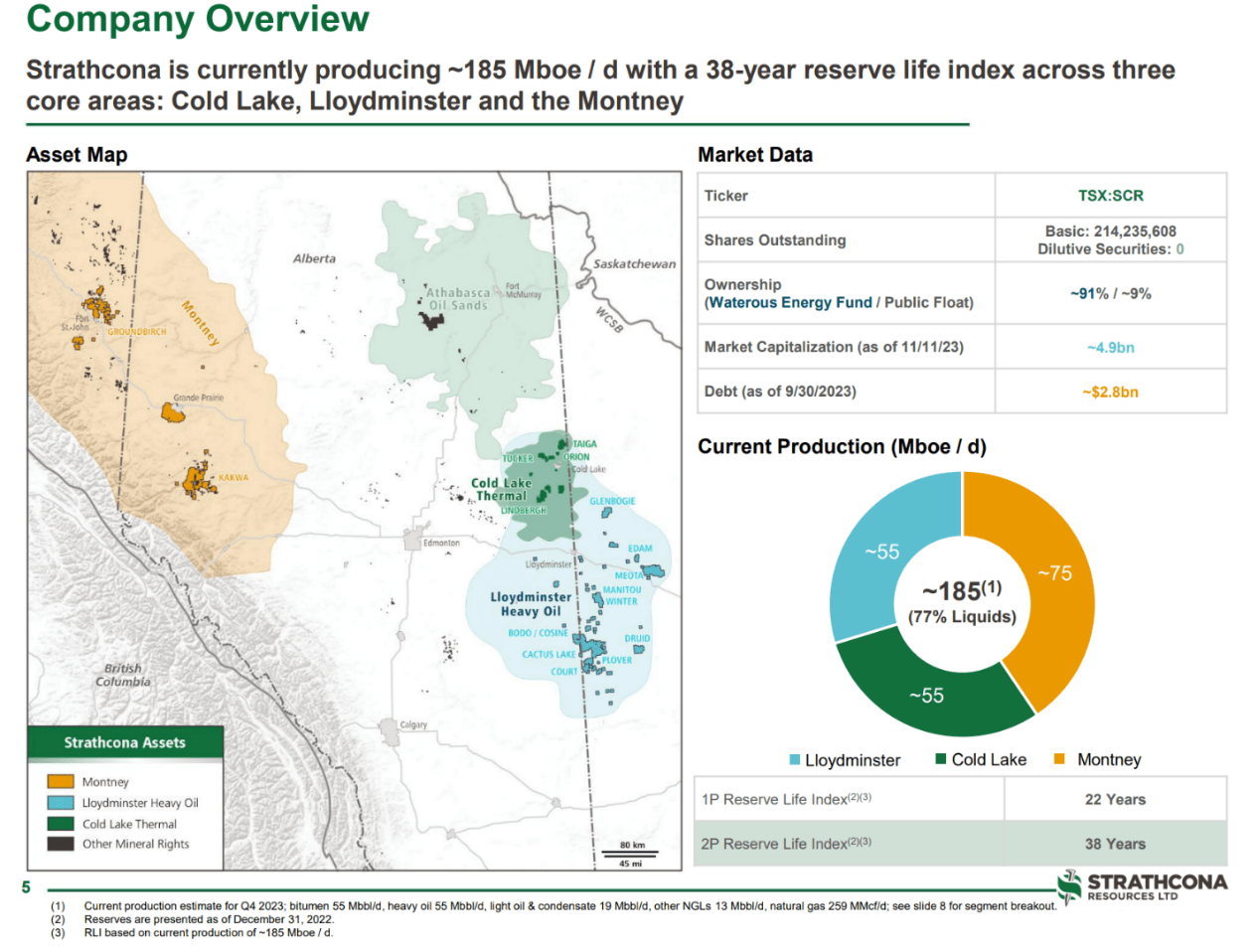

Today, SCR produces 185,000 boe/d with a proved and probable reserve life of 38 years, one of the highest among North American E&Ps. The company intends to grow production in 2024 to between 190,000 and 195,000 boe/d. An overview from the company’s latest investor presentation is shown below.

Source: SCR November 2023 Investor Presentation, Nov. 12, 2023.

SCR entered the fourth quarter 80% hedged at US$78 per barrel WTI. The hedging program locks in cash flow to fund debt paydown and near-term capital expenditures.

In 2024, SCR expects to spend $1.3 billion in total capex. Of the total, $800 million is sustaining capex intended to keep production flat. It will be allocated equally across the company’s three main operating areas. Beyond that, SCR plans to spend $250 million on building out existing facilities and another $250 million on expanding longer-lead facilities meant to accommodate long-term production growth. These growth projects are expected to increase companywide production capacity by 25,000 boe/d.

SCR’s capital structure is simple. Long-term debt consists of $1.619 billion drawn on the company’s $2.3 billion bank revolver, a $525 million bank term loan due in February 2024, and $679 million of unsecured senior notes due in July 2026. Total long-term debt was $2.82 billion as of early November 2023.

SCR benefits from tax pools that will shield $5.6 billion of future income from taxes. As a result, the company won't pay taxes for many years.

Over the coming months, 100% of SCR’s free cash flow will be allocated to paying down debt and $150 million of derivatives inherited from the Serafina acquisition. When long-term debt reaches $2.5 billion, management plans to pivot toward distributing the “vast majority” of free cash flow to shareholders through a variable dividend and possibly share repurchases, which would be opportunistic.

Due in large part to its hedges, the company expects to pay down the debt taken on over the past few months by the end of February 2024. If WTI remained at US$70 per barrel and assuming no hedges, a US$15 per barrel WCS-WTI differential, and 190,000 boe/d of production, we estimate SCR would generate approximately $400 million of free cash flow. Allocating all free cash flow to debt reduction would allow the company to hit management’s $2.5 billion debt target by the end of 2024.

SCR’s share price faces some headwinds. For instance, 70% of Pipestone had been owned by three large shareholders. These shareholders are likely to sell the SCR shares they received in the Pipestone acquisition. Concerns about their selling will create an overhang that prospective shareholders hate. Moreover, their actual selling will increase downward pressure on the share price. Long-term investors should use these price distortions that bear no relation to fundamental value to buy SCR shares.

On SCR’s third-quarter conference call, management said that WEF is likely to liquidate some of its stake in SCR in two-to-three years. The liquidation is likely to occur by way of non-dilutive secondary share sales, so it shouldn’t be perceived as an overhang. Such sales would increase the trading liquidity of SCR shares, which would be positive for shareholders.

Longer-term, SCR’s main objective is to continue to grow and compound intrinsic value per share. We believe shareholders are in good hands with its current leadership. Executive Chairman Adam Waterous, now 62 years old, believes the long-term oil bull thesis remains in play.

Waterous will remain the Chairman of WEF and Strathcona. His former positions as a leading Canadian investment banker and top private equity executive have given him a deep understanding of the Canadian oil industry from top to bottom—the companies, people, assets, markets, trends, etc. He understands where the good assets are and, equally important, where they aren’t. He has a good grasp of asset value and is comfortable going against the grain of industry trends, with a flair for buying cheaply during downturns in a counter-cyclical fashion. This has been a hallmark of commodity executives who have successfully created vast wealth through acquisitions. He takes a value-based approach to oil and gas investing and brings unmatched expertise in pursuing complex special situations. We believe he will continue to build value through outstanding capital allocation.

Waterous typically hunts for bargains, but he isn’t afraid to pay up for assets with low-decline, long-lived reserves, as he did in the Serafina deal. As with any acquisitive company, shareholders face a risk that SCR pays too much for an acquisition, but given the company’s long-term disciplined track record, we believe the risk is minimal. And in terms of strategy, we don’t expect SCR to make any strategic mistakes as long as Adam Waterous is at the helm.

SCR plans to use its new publicly-listed shares to facilitate growth, though any acquisition would have to be accretive. Management acknowledged that SCR shares are currently undervalued on SCR's third-quarter conference call.

Insiders have recently bought shares on the open market, putting action behind their stated belief the shares are cheap. On December 6, Director Director Andrew Kim bought 3,000 shares at $22.04 and Director Cody Church bought 1,140 shares at $22.00. On December 7, Kim bought another 3,600 shares at $20.66.

We don’t expect SCR to use its shares as currency in a deal unless it obtains significantly more value than it gives up by issuing shares or until the share price recovers.

After SCR reaches management’s debt target, we expect it to return to making acquisitions. We expect targets to be in the 50,000 boe/d to 75,000 boe/d range with assets that complement SCR's existing positions in Cold Lake thermal, Lloydminster heavy oil, and the Montney. Adam Waterous believes that consolidation in the Canadian oil patch will continue until there are nine or ten large publicly traded E&Ps. We suspect he intends to make SCR one of them.