(Idea) Spartan Delta - Our Favorite Natural Gas Producer

Spartan Delta (SDE:CA) is the fourth iteration of the Spartan management team. The Spartan team has earned a stellar reputation for creating value across oil market cycles by identifying prospective acreage, developing it, and then selling it at a profit.

The team’s previous corporate iterations—and the spectacular returns they generated over the past fourteen years—are shown below.

Source: Spartan Delta Investor Presentation, Aug. 7, 2024.

SDE began its current “Delta” iteration by raising $25 million in 2019. In 2020, it bought Bellatrix Exploration out of bankruptcy for $64 million. Then in 2021, it acquired Montney acreage for $125 million, and in 2022, it acquired privately-held Velvet Energy, a Montney light oil producer, for $150 million.

In 2023, it partially monetized its asset base by selling its Montney acreage to Crescent Point Energy—now Veren (VRN:CA)—for $1.7 billion. After the sale, SDE paid a $9.60 per share dividend funded by the proceeds.

Later in 2023, SDE spun off Logan Energy (LGN:CA) to its shareholders at $0.30 per share. Logan shares currently trade at $0.80 per share.

Unveiling a New Position in the Duvernay

After the Logan spin-off, SDE management touted the company as an income-producing alternative to the growth-oriented Logan. At the same time, however, it was acquiring highly prospective Duvernay acreage on the cheap.

Management announced the company’s new Duvernay position in the second quarter, showcasing its new West Shale Basin acreage that will be developed essentially from the ground up. This is the preferred mode of growth of some of our favorite E&Ps, including Peyto Exploration (PEY:CA), Headwater Exploration (HWX:CA), and Logan Energy, all of which are among the best value creators in the North American oil patch. The potential for outsized returns stems from a company entering a play on the cheap and then having full control of where and when to drill and develop infrastructure. Once meaningful scale is achieved, further expansion can take various other forms, such as corporate acquisitions.

SDE’s Duvernay acreage is significantly more weighted toward liquids than the legacy acreage it held immediately after its Logan spin-off, most of which was located in the gas-rich Deep Basin. We expect SDE’s development of its Duvernay acreage to grow its production and its liquids weighting and, as such, to serve as a catalyst for a higher stock price in the next one to three years.

Management is optimistic about SDE’s Duvernay prospects. It commented in the company’s second-quarter results press release, “Based on compelling technical attributes and thorough technical analysis, Spartan believes that the majority of its acreage is in the tier one oil and condensate rich Duvernay fairway, which has the potential to unlock significant value as the asset is developed.”

SDE’s Duvernay position is located in the West Shale Basin, one of the last large-scale underdeveloped reservoirs in the Western Canadian Sedimentary Basin (WCSB). It holds the Kaybob Duvernay, Willesden Green, and Pembina Duvernay plays. It features Paramount Resources (POU:CA) and Baytex Energy (BTE:CA) as its largest active public E&Ps aside from SDE.

SDE began its push into the Duvernay earlier this year. In May, it acquired Tourmaline Oil’s (TOU:CA) 38,000-acre West Duvernay asset for $53.1 million in cash. The acquired asset is located in the condensate-rich northern Willesden Green area. SDE estimates the asset was purchased at an attractive 2.8-times multiple to 2024 net operating income generated at US$80 per barrel WTI and $1.75 per GJ AECO.

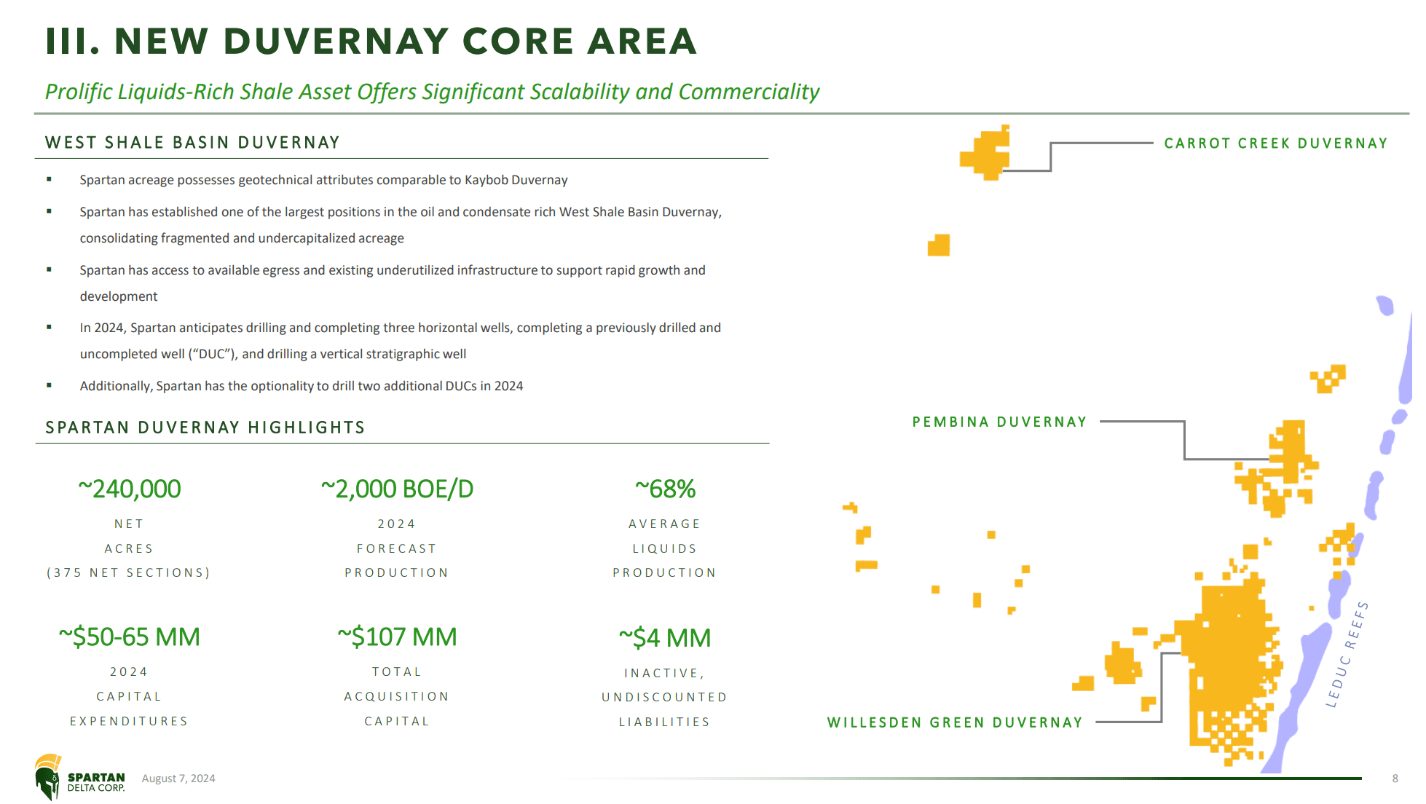

At the time of the acquisition, SDE also unveiled its 240,000-acre Duvernay position, which is shown below.

Source: Spartan Delta Investor Presentation, Aug. 7, 2024.

The position was acquired for a total of $106.6 million, representing a low average cost of $444 per acre. The acreage came with 2,000 boe/d of production, which was 68% liquids.

Given the low entry price and drilling results to date, the asset offers extraordinary returns if it meets management’s expectations.

The market greeted the acquisition announcement with a yawn. SDE shares haven’t moved much since the announcement. However, SDE’s slightly higher debt load since then results in a larger enterprise value.

It’s notable that the market didn’t pay much attention to SDE as it built its Montney position in the 2020-to-2023 timeframe. That position was later sold to Crescent Point Energy, now Veren, for $1.7 billion in 2023.