(Idea) Saturn Oil & Gas: Undervalued Or Value Trap?

Saturn Oil & Gas (SOIL:CA) is the ultimate E&P battleground stock. The bulls point to big upside and the bears see steep downside risk.

Without a doubt, the shares are cheap based on the numbers alone. Saturn screens better than nearly all its peers based on price-to-reserve value and cash flow torque to commodity prices. The question is how likely that value is to be realized by shareholders.

In Saturn’s case, the negatives in the picture raise red flags that suggest the company is of lower quality than its numbers alone imply. The risk of the stock being a value trap makes it too hard for us to get comfortable owning the name, despite its statistical attractiveness.

Until the company can reduce debt, its shares will remain in the penalty box. Moreover, shareholders will be at constant risk of dilution and permanent capital loss. Since debt reduction is likely to take a number of years, these risks for shareholders are long-term in nature.

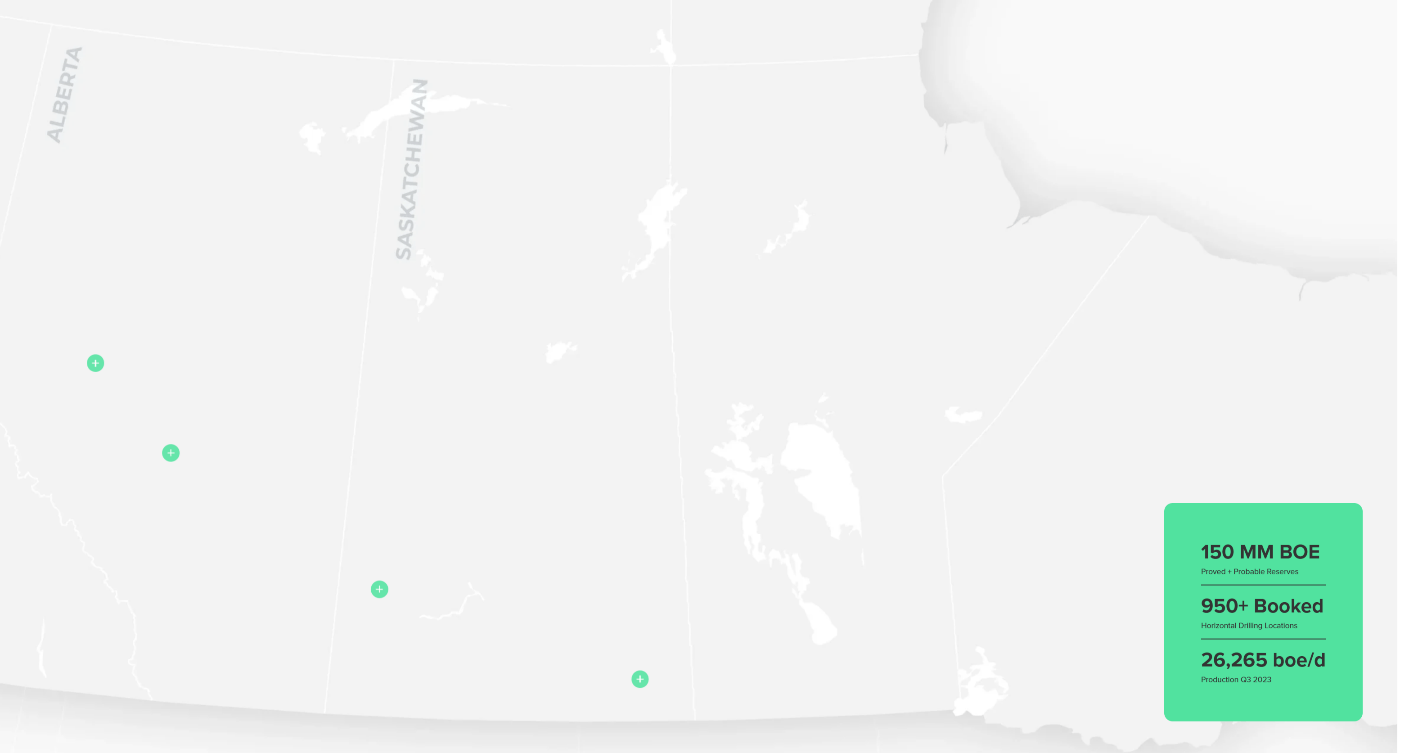

Saturn Overview

Saturn produces approximately 26,500 boe/d, which in the fourth quarter of 2023 was split 75% crude oil, 8% NGLs, and 17% natural gas. Its assets are located in Alberta and Saskatchewan, Canada.

Source: Saturn Oil & Gas website.

Last week, Saturn made a splash when it announced a new major acquisition from Crescent Point Energy (CPG). In the deal, Saturn paid $525 million for 13,000 boe/d of production in Saskatchewan comprised of 96% liquids.

The deal further polarized Saturn bulls and bears. The bears noted the deal came after management pledged to focus on paying down debt instead of expanding the company.

The bulls, by contrast, were gratified by the deal’s strategic rationale. For one, the acquired assets’ 96% liquids content is superior to Saturn’s existing production base, which produces 83% liquids. The acquired assets are also contiguous with Saturn’s existing asset base. And while the assets didn’t come cheap—at $40,385 per flowing barrel—their price tag reflects their oily nature and low royalty rates. The deal metrics are more attractive on an NPV10 basis, by which the deal came at an attractive 0.65-times PDP.

The deal also makes sense from a strategic standpoint, as it significantly increases Saturn’s scale in its core operating area. Management estimates a 20-year inventory life at the current development rate.

The most impressive feature of the acquisition wasn’t the assets, but the more lenient terms Saturn’s lenders offered to finance it. The new $625 million in financing replaces the company’s senior secured term loan that carried a 16% interest rate. It also reduces the need for hedging and involves no capital spending restrictions.

Saturn’s largest institutional shareholder, GMT Capital Corp., provided $100 million of equity financing for the deal at $2.35 per share, a discount of 11.3% to the pre-deal share price. The financing added 42.6 million shares to Saturn’s existing diluted share count of 180.2 million shares, representing 23.6% dilution. If the underwriters exercise their over-allotment option, dilution increases to 27.2%.

Given the stock's battleground status, it's worth comparing the positives and negatives to determine whether the shares are worth the risk.