(Idea) Petrobras - Attractive Relative To Peers

By: Jon Costello

For years, Petrobras (PBR) overpromised and underdelivered on production growth to its shareholders. The company was a perennial underperformer due to geological, operational, regulatory, and political factors.

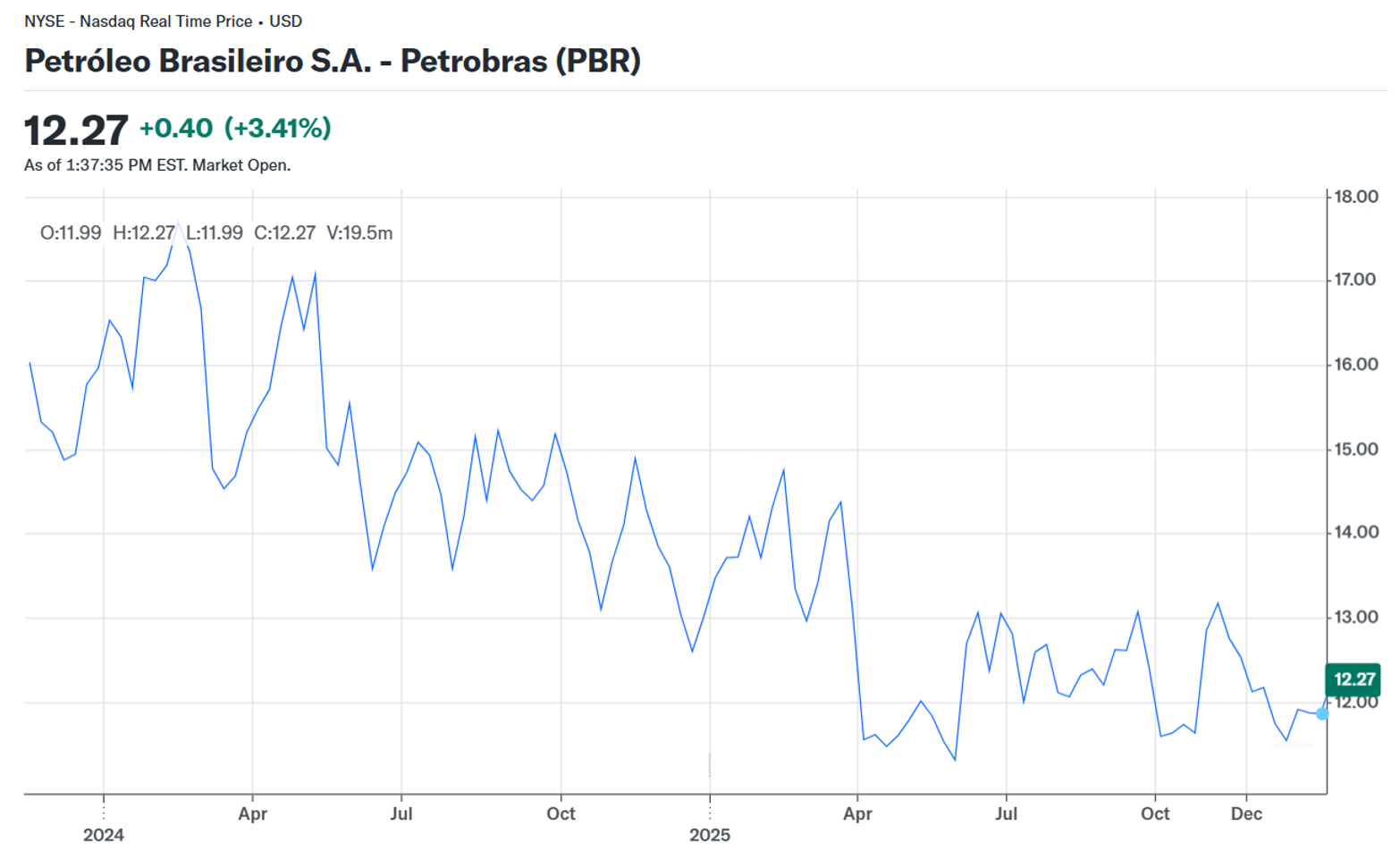

However, performance has recently improved. The turn is visible in the company’s quarterly results, though its stock has yet to respond, as shown in Petrobras’s three-year stock chart.

Source: Yahoo! Finance, Jan, 13, 2026.

I last covered Petrobras in October 2024. Since then, it has outperformed my expectations as its production has grown and its operations have become more efficient. The question today is whether these changes are sustainable. If they are, the stock is attractive at its current price.

Evidence is mounting that the changes are indeed sustainable. We expect significantly higher commodity prices over the coming years, and the shares are likely to do very well in a rising commodity price environment.

Consider that over the next five years, Petrobras’s production is set to increase from 3.1 MMBoe/d in 2023 to 3.5 MMBoe/d in 2030. Increasing production, combined with improved operating performance, will enhance cash flow torque to commodity prices. Moreover, capex is slated to decline over the same timeframe, which can turbocharge free cash flow growth. Higher dividends for common shareholders will likely follow.

If Petrobras can execute over the coming years, I expect its shares to outperform the international major oil companies that comprise its peer group. If commodity prices break significantly higher, I expect them to surge to multi-year highs, more than 50% above the current share price.