(Idea) Peabody Energy

Editor’s Note: Ideas from HFI Research is a separate paid subscription to HFI Research. Peabody Energy is not a holding in the HFI Portfolio. Please consider subscribing to support Jon’s excellent work.

By: Jon Costello

Peabody Energy’s (BTU) prospects are challenging to appraise due to the company’s complicated history, its exposure to an unusually broad array of risks, and a controversial pending asset acquisition. The shares are clearly cheap, but their price reflects the real risk of permanent capital loss. That said, they offer explosive upside amid a met coal price recovery.

In view of the risk of permanent capital loss amid low coal prices, Peabody shares are most suitable for investors who seek to speculate on a coal price recovery and hold for one-to-two years. A met coal price recovery, in particular, would offer a potent free cash flow boost, which could send the shares up by more than 100% from their current price.

Investors looking to benefit from long-term compounding of intrinsic value per share are likely to be better served owning Warrior Met Coal (HCC) over the long term. Due to its superior management, low operational and financial risk, and the huge potential upside in its shares, Warrior remains my favorite coal name.

Peabody Energy Overview

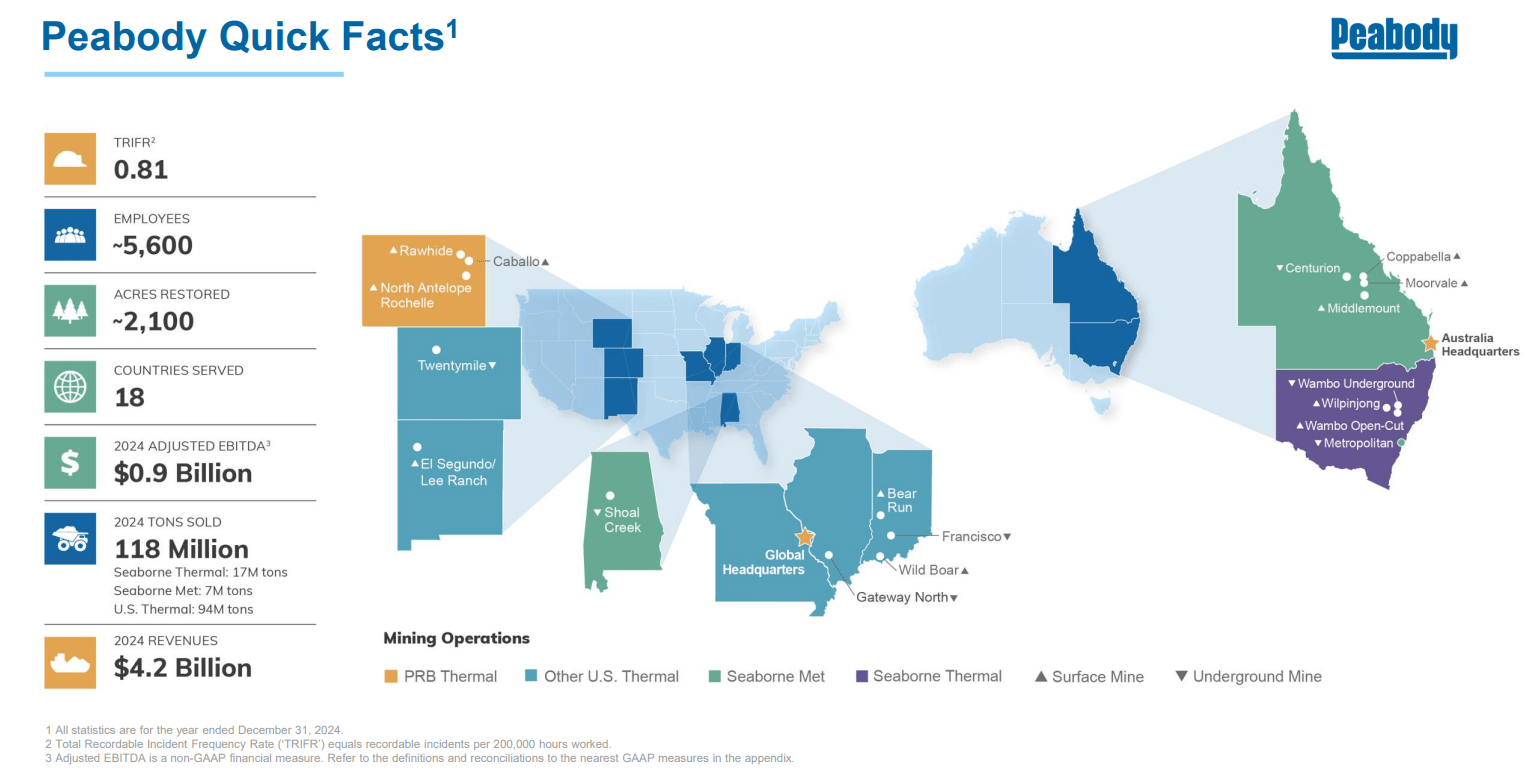

Peabody Energy operates in both thermal and metallurgical (met) coal in the U.S. and Australia. The graphic below provides an overview.

Source: Peabody Energy Presentation at B. Riley Investor Conference, May 21, 2025.

With annual production over the past four quarters of 118 million tons per year, Peabody is the largest U.S. coal producer. It has been pivoting its operations away from thermal and toward metallurgical coal for the past few years.

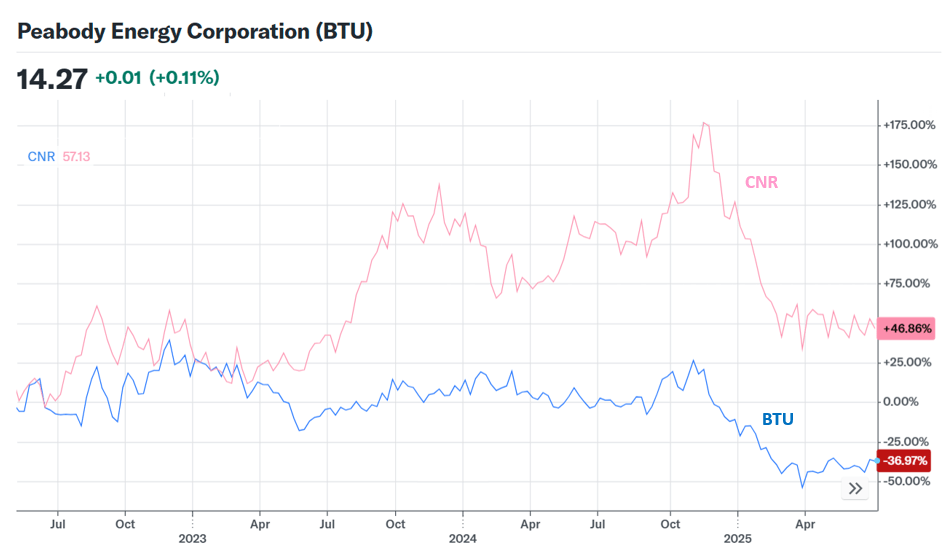

Peabody shares have underperformed their peers due to the company’s higher cost structure and ongoing track record of poor capital allocation. Over the past three years, Peabody's stock has badly lagged behind its nearest domestic comparable, Core Natural Resources (CNR), as shown in the chart below.

Source: Yahoo! Finance, July 9, 2025.

Over the past four quarters, Peabody generated $855.2 million in Adjusted EBITDA. Given its $1.4 billion enterprise value, its shares trade at a rock-bottom 1.6-times EV/EBITDA ratio on a trailing 12-month basis.

Low coal prices over recent months have pressured Peabody’s financial results. In the first quarter of 2025, the company generated $144.0 million in Adjusted EBITDA. Given cash tax payments and full-year capex guidance of $450 million, the company is essentially operating at cash flow breakeven.

The bull case for Peabody centers on the consistent cash flow the company generates from its thermal coal assets, coupled with the cash flow torque provided by its expanding met coal operation.

The bears have been winning, however, due to the various negatives in the company’s picture. These negatives, which present various risks to shareholders, are discussed below.