(Idea) Oneok - Red Flags

By: Jon Costello

Oneok (OKE) is a popular large-cap midstream stock for investors seeking exposure to U.S. natural gas demand growth in the coming years. The company’s EBITDA is expected to grow as natural gas and NGL throughput increase in its midstream systems across the Bakken, Mid-Continent, and Permian basins.

OKE shares have declined 36% from their 52-week high of $118 in November 2024 to what appear to some to be bargain levels. Wall Street brokerage houses maintain price targets above $100 and are universally bullish on OKE’s prospects. The stock’s 5.4% yield appears attractive going into a lower interest rate environment. Additionally, OKE trades at a 9.8-times EV/EBITDA multiple, below its peer average of 10.8 times.

The stock’s recent decline has caught the attention of some of our sharp-eyed subscribers as a long-term income investment.

Source: Yahoo! Finance, Aug. 29, 2025.

Despite the seemly attractive setup, OKE’s financial performance over the past few quarters raises questions about its ability to sustain its historically high return on capital employed (ROCE). A declining ROCE portends a lower trading multiple and potential difficulty generating significant free cash flow growth over the longer term.

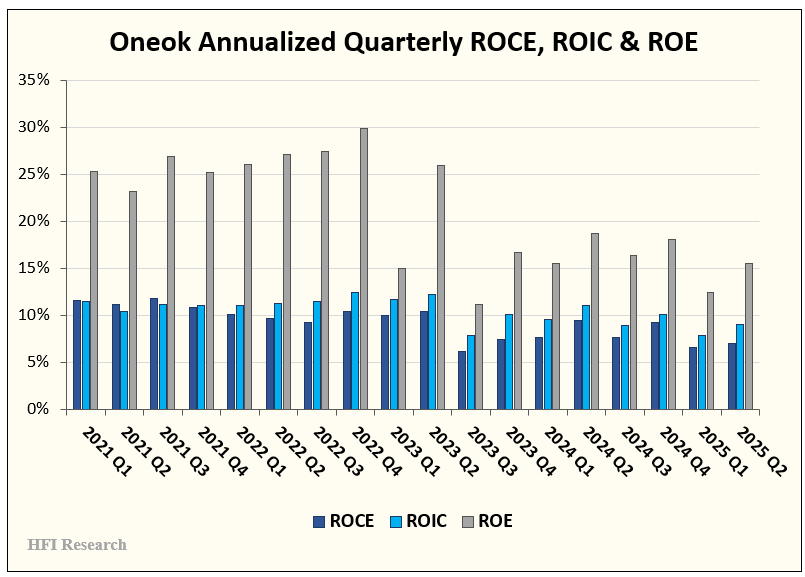

Since the end of 2022, the company's ROCE, return on invested capital (ROIC), and return on equity (ROE) have all trended lower, as shown in the following chart.

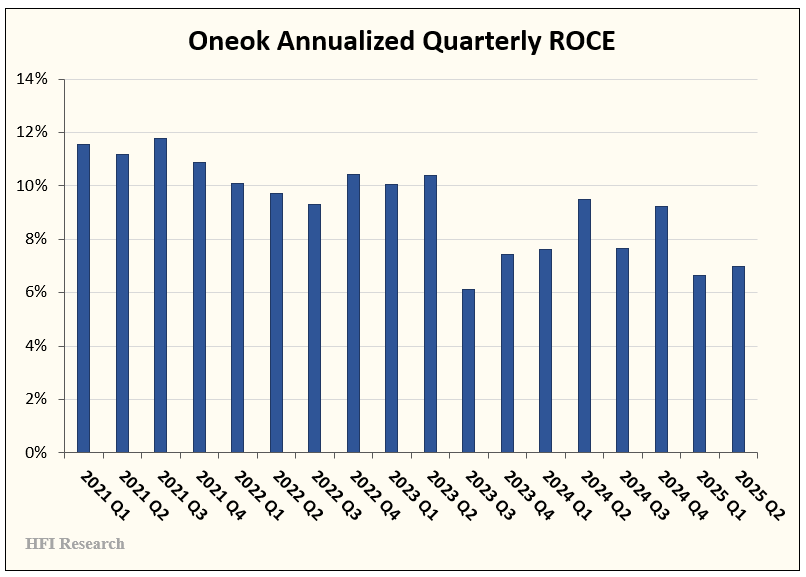

Zooming in on ROCE—arguably the most important metric for assessing midstream performance—shows a concerning downward trend.

OKE’s ROCE has decreased from comfortably above 10% to the high single digits. For context, the company’s weighted average cost of long-term debt is around 5.1%.

The results greatly reduce the appeal of OKE’s EBITDA growth, as the growth has been achieved at the expense of all-important returns on capital.

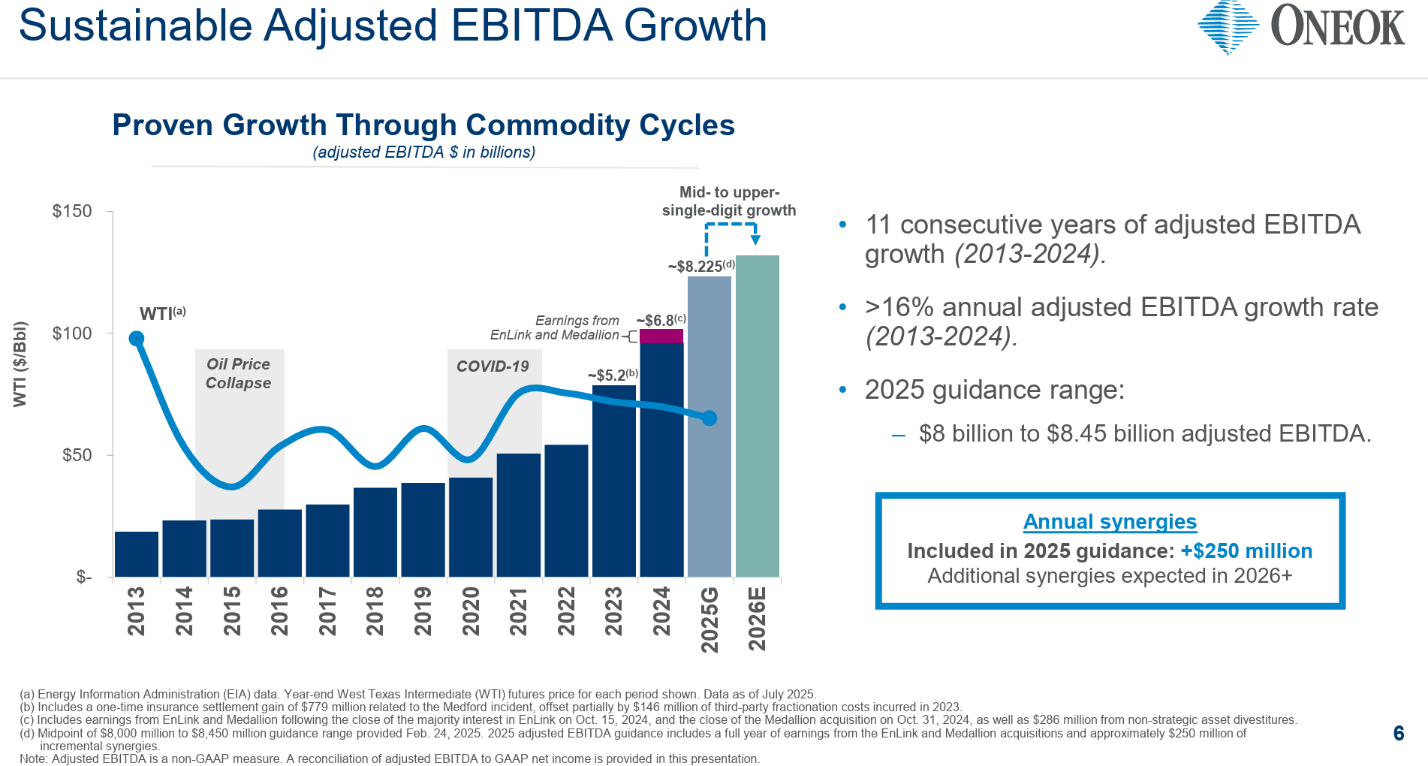

Source: Oneok August 2025 Investor Presentation.

I would rather own a business that earns high returns on capital and distributes free cash flow to equity owners than one that increases its EBITDA or free cash flow and sees its returns on capital decline, as OKE is doing now.