By: Jon Costello

MPLX (MPLX) units continue to fit the mold of a ballast portfolio position. When we first invested in them back in April 2021 ($27.27), we viewed them mostly as a yield generator with the kicker of a low growth rate. At the time, the $30 billion market cap company was guiding to $800 million of annual capex. Its return on equity in the low teens implied low-single-digit Adjusted EBITDA growth over the longer term.

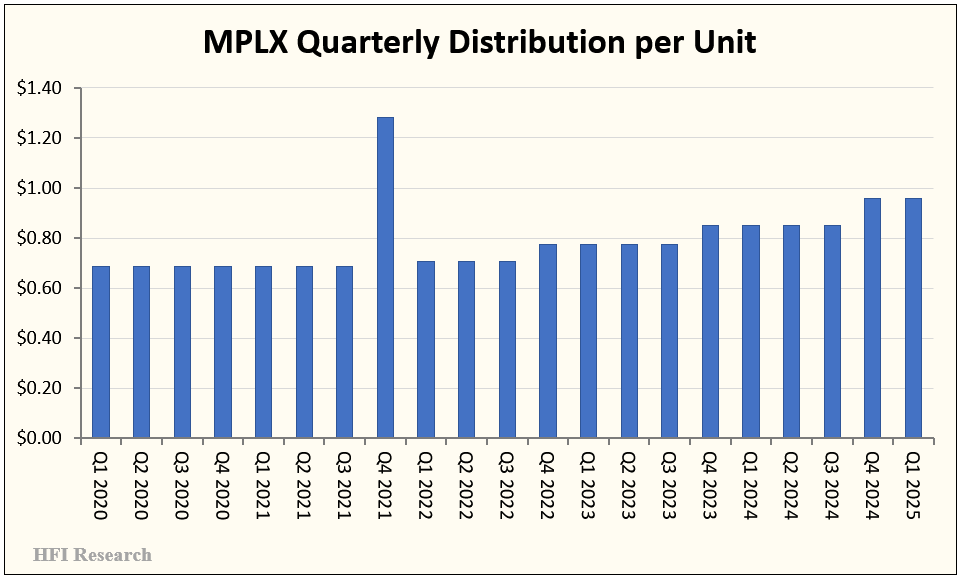

Over the past few years, however, we've been pleasantly surprised. MPLX has actually invested closer to $2 billion per year of capex instead of its guidance of closer to $1 billion. The result has been greater than expected Adjusted EBITDA growth, which, in turn, has driven greater than expected distribution growth. In November, MPLX increased its quarterly distribution by 12.5%, its third distribution increase of at least 10% in as many years.

While the company's organic growth capex has indeed tracked around $1 billion, it spent additional capex sums on executing bolt-on acquisitions and increasing its ownership interests in pipelines. The additional capex spending has generated attractive returns on capital while also fortifying the company’s midstream franchise, which now touches 10% of U.S. natural gas production.

We credit MPLX’s former CEO, Mike Hennigan—now the company’s Executive Chairman—for the company’s outstanding performance in recent years. His execution, characterized by regularly under-promising and over-delivering, has caused the units to approach their highest price since the MLP bubble back in 2015. We expect MPLX’s performance to continue under its new CEO, Maryann Mannen.

We remain steadfast holders of MPLX units. Over at least the next three years, we expect mid-to-high single-digit cash flow and distribution growth. The units will remain a ballast in our HFIR Energy Income Portfolio.

Fourth-Quarter Results

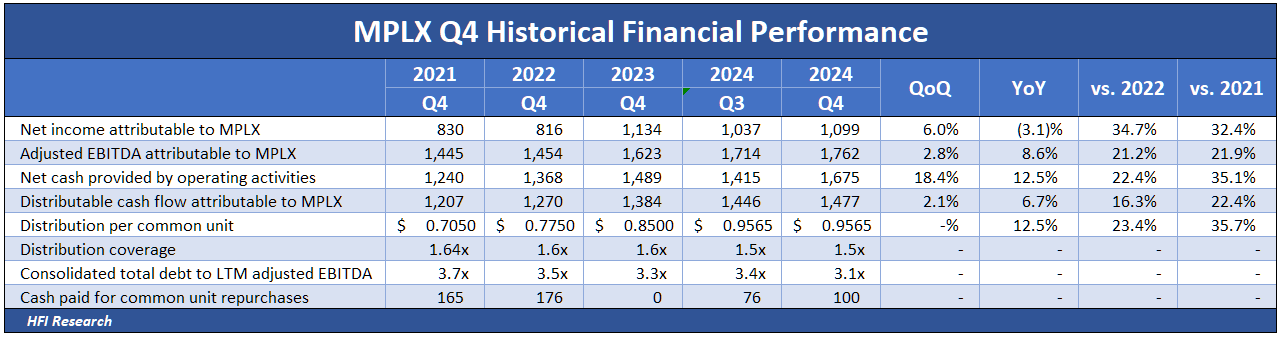

MPLX reported Q4 2024 financial results this morning. Adjusted EBITDA came in at $1.76 billion versus consensus expectations of $1.69 billion, for a 4% beat. Year-over-year Adjusted EBITDA grew by 8.6%, in line with the company’s growth rate in recent years. The cash flow growth facilitated a 12.5% year-over-year increase in the common distribution, maintaining a healthy 1.5-times coverage of the distribution by Adjusted EBITDA, a proxy for operating cash flow.

MPLX’s financial results were excellent. The following table shows the company’s impressive fourth-quarter performance and long-term growth.

Operating results during the quarter were similarly impressive, particularly in the company's natural gas and NGLs operations. However, a recent change in its segment reporting prevents a long-term comparison.

For context on how well these midstream assets can perform relative to refining assets, MPLX’s parent, Marathon Petroleum Corp. (MPC), reported $94 million of Adjusted EBITDA during the fourth quarter, a full 95% below that of MPLX. The MPLX distributions that MPC received during the quarter prevented MPC from reporting a large EBITDA loss.

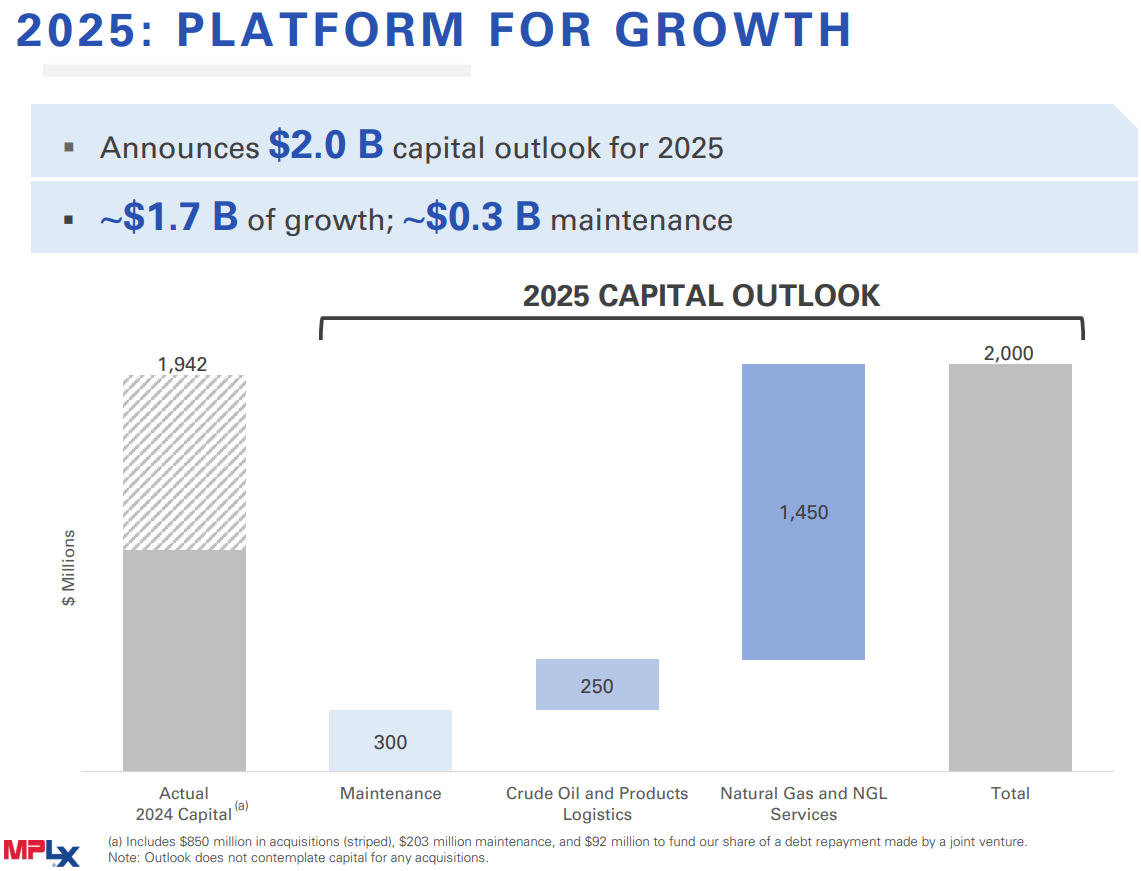

Just as important as MPLX's beat was its plan for 2025. The company will continue to grow its Adjusted EBITDA as new projects come online. Higher cash flow guidance allowed management to increase its annual capex guidance from the $1 billion seen in recent years to around $2 billion, as shown below.

Source: MPLX Q4 2024 Earnings Conference Call Presentation, Feb 4, 2025.

The company’s natural gas and NGL asset footprint buildout is expected to consume 85% of its growth capex in 2025. It will occur in the Marcellus, Utica, and Permian shale basins and the Gulf Coast. These investments in growth will drive companywide Adjusted EBITDA higher over time.

MPLX announced major growth joint venture projects with Oneok (OKE). One of these is a 50%/50% joint venture in a 400,000 bbl/d LNG export terminal, and the other is an NGL pipeline that will service the export terminal. The pipeline is being built, operated, and is 80% owned by OKE and 20% owned by MPLX.

MPLX added several other new growth projects during the fourth quarter. These include its Matterhorn natural gas pipeline expansion, which will increase the pipeline’s capacity from 2.0 Bcf/d to 2.5 Bcf/d. This pipeline alleviated a severe Permian natural gas bottleneck. MPLX is also expanding into fractionation. These projects will enter service in 2025 and 2026, respectively.

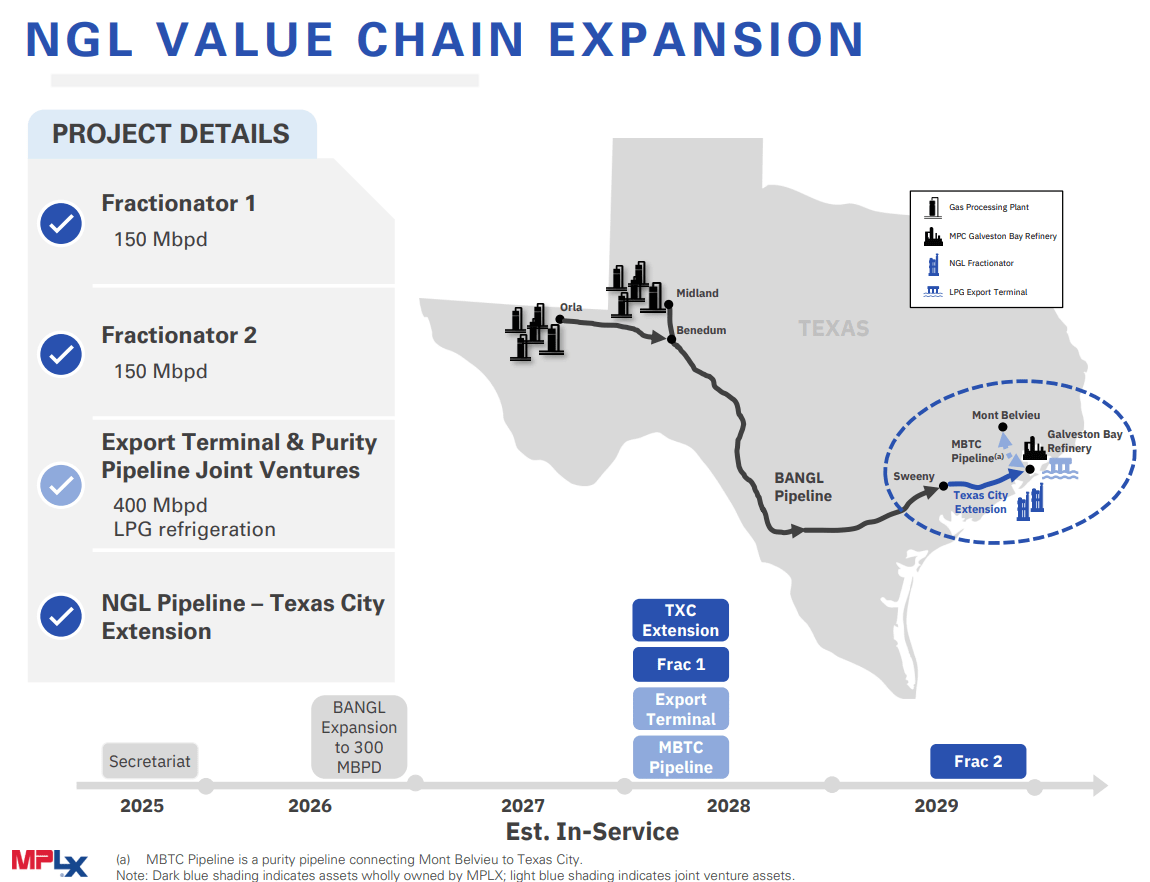

Historically, the company has used third parties to fractionate its transported volumes. However, its natural gas infrastructure buildout over recent years has enabled sufficient integration for the company to source its own feedstock and then carry out the other services along the natural gas value chain, with fractionation being the latest addition. MPLX’s integration for natural gas and NGLs is shown in the graphic below.

Source: MPLX Q4 2024 Earnings Conference Call Presentation, Feb 4, 2025.

Other projects currently underway include MPLX’s expansion of its BANGL NGL pipeline from 125,000 bbl/d to 250,000 bbl/d and its expansion of the Utica shale gathering system.

These projects will keep growth momentum on track. We expect mid-single-digit percentage cash flow growth to drive a higher unit price. Due to inflation escalators in its contracts with MPC, cash flow will remain protected from inflation. We expect the yield on MPLX units to remain around today’s 7.4%.

Risks

Immediate risks include an acquisition by MPLX’s parent MPC, though MPC has stated that it prefers operating as two standalone entities. MPLX’s recent unit price run-up makes an acquisition by MPC less likely than it would have been before 2024 when the units traded at a steeper discount to value.

Another risk that MPLX faces is more long-term in nature. It relates to the midstream industry’s historical propensity to overbuild. More disciplined players like MPLX and Enterprise Products Partners (EPD) tend to sanction growth projects only when they’re justified by customer interest and financial returns; witness EPD’s announcement that it would not go forward with its Sea Port Oil Terminal. Unfortunately, the midstream industry has always included a bunch of aggressive growers who spoil the party for even the most disciplined industry participants. Today’s most aggressive grower would be Energy Transfer (ET). We’d lump Kinder Morgan (KMI) into the group, as well.

Midstream equities have had a spectacular run since 2020, but the risk is growing that the industry’s capital cycle is about to turn downward. Overexpansion can lead to lower returns on capital, which in turn lowers equity valuations in the sector. We’ll closely monitor developments in the industry and how they relate to its capital cycle.

Conclusion

We’re hard-pressed to find an income vehicle as attractive as MPLX units. Even though the units no longer trade at a steep discount—as they did when their yield exceeded 9%—we expect long-term Adjusted EBITDA growth to drive them higher. Investors can feel comfortable allocating funds to the units at their multi-year highs. With other sectors overvalued in today’s frothy markets, investors can still do well with a long-term holding in MPLX.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of MPLX, EPD, ET either through stock ownership, options, or other derivatives.