(Idea) Met Coal Recovery Update - Impact On Warrior Met Coal And Alpha Metallurgical Resources

By: Jon Costello

I’ve remained long Warrior Met Coal (HCC) since I bought shares for myself and clients in the low-$40s per share earlier this year. Frankly, I’ve been surprised by the extent of outperformance since then. The macro environment has undoubtedly improved, but the recovery in metallurgical (MET) coal prices has been much more subdued than what is implied by the surge in Warrior and Alpha Metallurgical Resources (AMR) stock. The shares have surged 68% and 64%, respectively, from their lows in June.

Considering the share price performance, I want to review macro met coal developments to assess the near-term outlook for Warrior and AMR shares.

A Tepid Macro Recovery

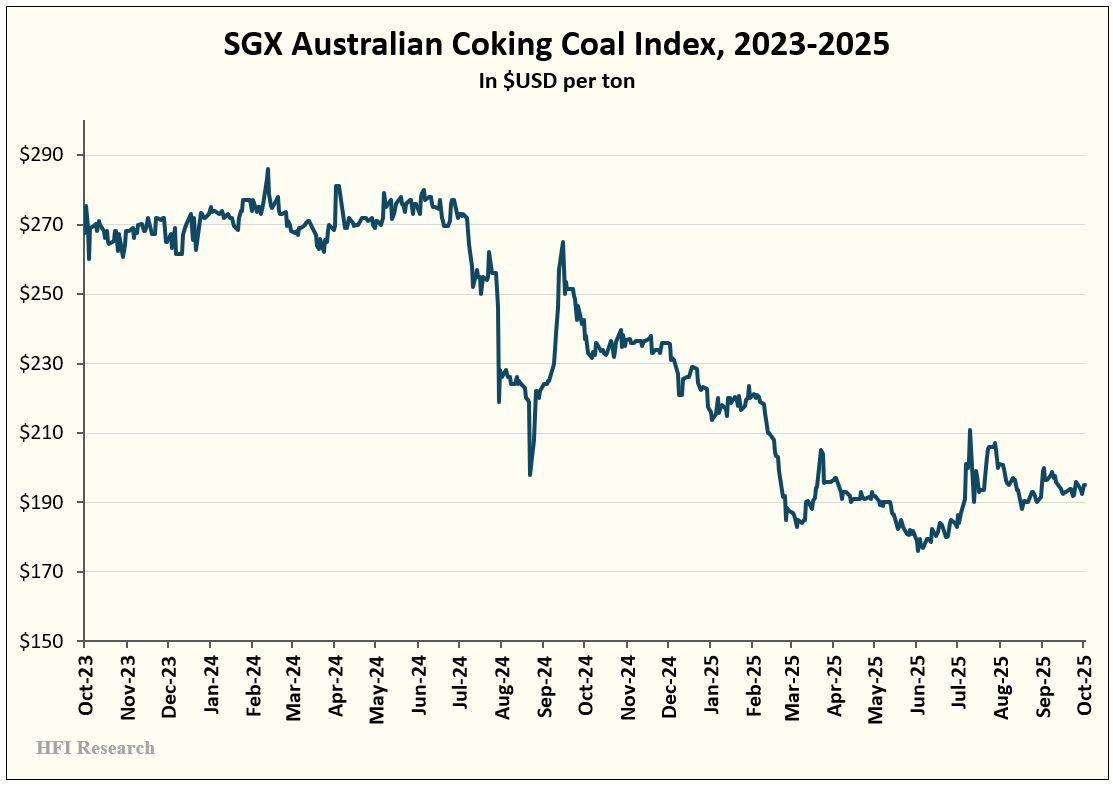

Over the last six months, the met coal market has been shaped more by episodic catalysts that slightly tightened the spot market than by a strong demand recovery. Met coal prices have rebounded from recent lows but remain low by historical standards.

Increasing steel demand isn’t the culprit for the price improvement, as steel demand has been choppy so far this year. Instead, the met coal price has been driven by idiosyncratic market developments. The standout bright spots were the government measures enacted in India and China. Both were marginal positives for the met coal market in 2025.

In India, the government implemented import quotas on metallurgical coke. The quotas took effect on January 1, 2025, and lasted until June 30, 2025, before being extended through the end of the year.

The quotas led to a coke shortage for Indian steelmakers. Coke is the fuel used to heat steelmaking blast furnaces. The shortage of coke forced domestic steelmakers to rely more on their own coke ovens for converting met coal to met coke. Increased met coal imports from Indian steelmakers boosted demand for met coal from abroad. Met coal prices tracked demand slightly higher.

The Indian government’s reason for implementing the quotas was to restrict cheap imported coke that was undercutting the country’s domestic met coke industry. Despite protests from Indian steelmakers, the measure is expected to be extended further into 2026.

In China, the world’s largest steel producer and consumer, the government took measures to address weak steel demand and steel production overcapacity. In March, the government pledged to “promote restructuring of the steel industry through output reduction.” The measures were a sign that Chinese authorities recognized that the country’s steel industry faced a grim future after major steel importers imposed anti-dumping trade barriers against Chinese steel exports. If China could rationalize its steel supply, prices would firm and the domestic steelmaking industry would emerge on a more stable footing.

The measures are likely to cause the shuttering of older, low-efficiency blast furnaces, while benefiting newer, highly efficient, integrated steel mills. These newer mills use higher-quality coke and premium hard coking coal. If they’re more profitable, they’ll consume more high-quality met coal. As a result, China’s steelmaking capacity limits are net bullish for met coal imports and large global producers.

Then, around mid-year, the Chinese government took further action and placed curbs on the country’s met coal production. It also increased inspections of coal producers to enforce compliance. Analysts estimated that one-third of China’s coking coal mines either suspended or curtailed production.

China’s measures came in response to met coal prices dropping below the cost of production. The intent was to limit the fallout on the domestic coal industry, as persistently low prices threatened to trigger industry-wide bankruptcies and layoffs. The measures also aimed to reduce some risks caused by ongoing underinvestment during periods of low prices, such as attempts to cut corners with regard to worker safety and environmental rules.

These measures implemented by the Indian and Chinese governments were largely responsible for the marginal increase in global met coal prices over recent months. They also reined in the market’s high short position earlier in the year. Met coal producers like Warrior and AMR have received an outsized benefit due to their logistics optionality and strong balance sheets.

While these measures were positive for the met coal price, others were more bearish. For example, weather events, such as India’s monsoon season, reduced steel demand more than usual this year.

More importantly, China’s retaliatory 15% tariff on U.S. met coal imports effectively cut off the country as an export destination for Warrior and AMR. However, since the met coal market is global, the companies were able to redirect their product elsewhere.