(Public) Mach Natural Resources - Natural Gas Torque With Income

By: Jon Costello

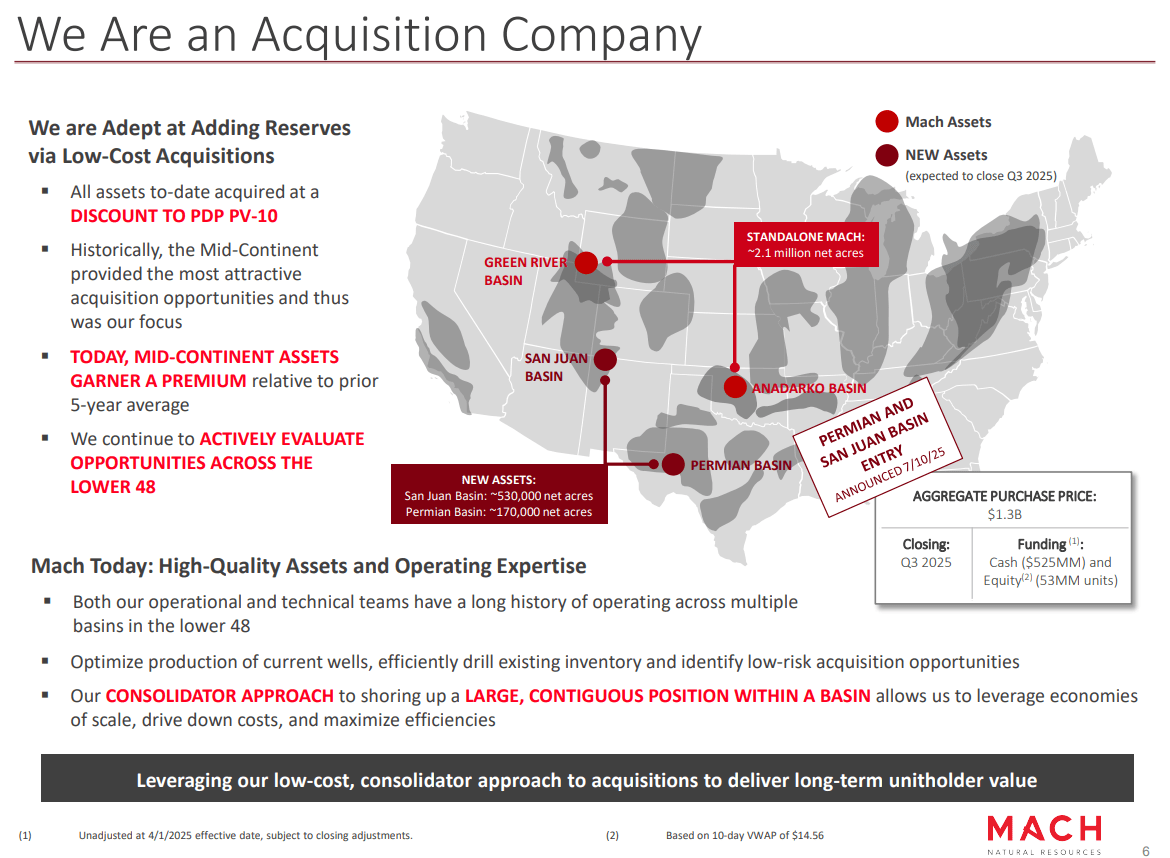

Mach Natural Resources’ (MNR) operations were previously focused exclusively in the mid-continent region before it announced two transformative asset acquisitions on July 10. The acquired assets expanded the company’s footprint into the San Juan and Permian Basins. An overview is shown below.

Source: Mach Natural Resources Q2 Earnings Presentation, August 2025.

The post-acquisition entity will produce approximately 151,000 boe/d comprised of 20% crude oil, 15% NGLs, and 65% natural gas.

The recently acquired assets extend MNR’s reserve life from 8 to 10 years. Their most notable feature is the low decline rate. The company states that the San Juan and Permian assets possess a base decline of only 10% and 8%, respectively, compared to the pre-acquisition entity’s 20%. After integration, these assets will bring MNR’s base decline rate down to 15%, making it one of the lowest among its U.S. E&P peers.

MNR’s new low-decline assets will enhance its capital efficiency and financial flexibility, which is crucial for an E&P that aims to maximize payouts to equity owners.

With the new assets, MNR can keep its reinvestment needs relatively low, allowing it to distribute a large portion of its cash flow to equity owners. The low-decline assets also boost the company’s cash flow potential amid higher oil and natural gas prices.

An Attractive Buy When Commodity Prices Are Low

WTI is currently trading in the mid-$60s per barrel, and Henry Hub natural gas is around $2.80 per mcf. Nobody would argue that either of these prices is “high.”

Given the long-term demand growth outlook for both commodities and the difficulty the North American industry will have meeting that demand at current prices, investors should consider increasing their exposure to oil prices now, before prices are sustained at much higher levels.

MNR is an attractive alternative for investors who want to get paid while waiting for the commodity price cycle to inflect higher. The company’s ten-year PDP reserve life at its pro forma production level after its recent acquisitions gives investors ample time to wait for higher commodity prices to trigger a rally in its equity price.

MNR’s acquisition strategy is agnostic with regard to commodity mix. It purchases assets based on their value and price without reference to whether they’re weighted toward oil or gas. Consequently, MNR is more likely to make bargain purchases, which is all-important in maintaining and growing equity value through acquisitions. One downside of this approach is that it complicates an investor’s efforts to envision the future for the purposes of gauging commodity mix and intrinsic value.

Robust Income Generation

As investors wait for higher commodity prices, they’ll be rewarded handsomely by the company’s generous tax-advantaged distributions to equity owners.

MNR seeks to reinvest enough capital to maintain flat production. Any cash flow above reinvestment requirements will be paid out as a variable distribution. MNR’s distribution will therefore depend upon how much cash flow it generates at different commodity prices and upon its hedging activities.

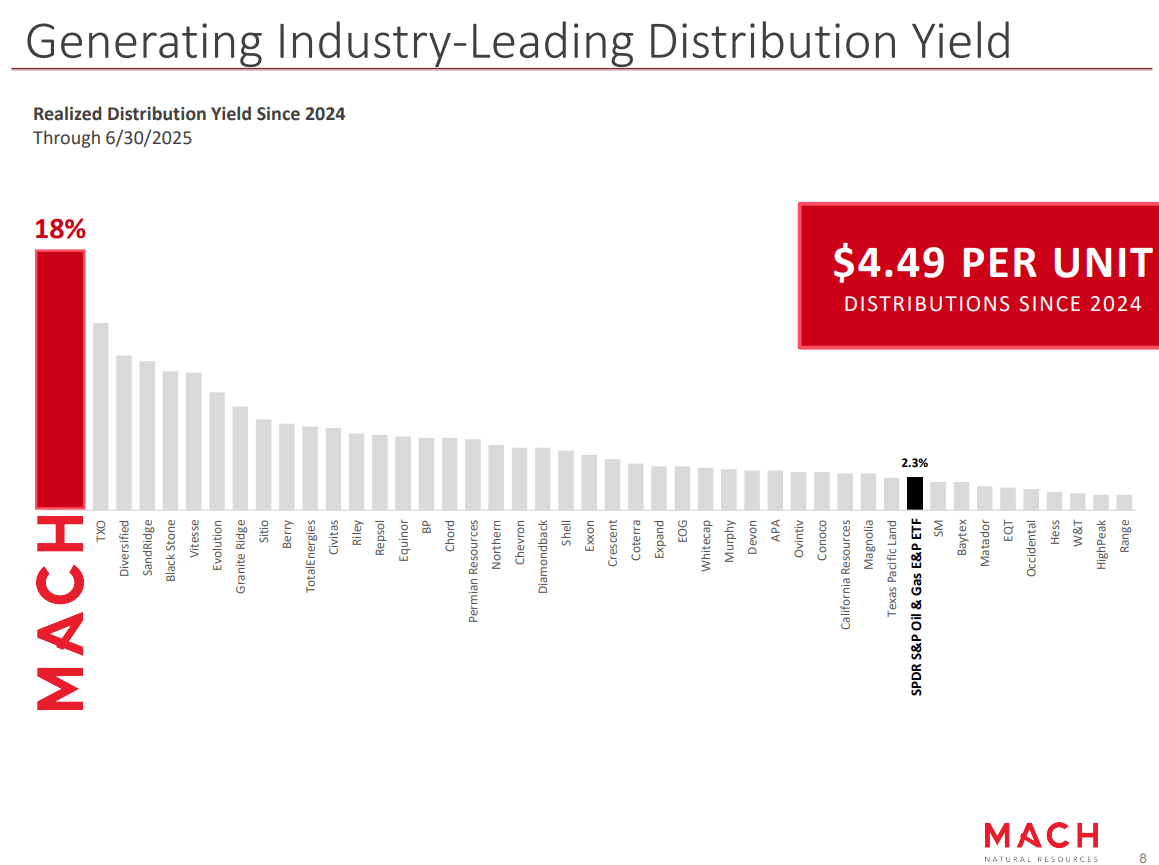

The company has already established itself as one of the top distributors of cash to equity owners among its E&P peers, as illustrated in the following chart.

Source: Mach Natural Resources Q2 Earnings Presentation, August 2025.

MNR is a master limited partnership, or MLP. As such, its common stock is referred to as “common units” or “limited partner interests.” Its payouts to equity owners are referred to as “distributions” instead of “dividends.” Based on the most recent distribution of $0.38 per unit, MNR units trade at a 10.6% distribution yield.

As an MLP, MNR’s limited partners are shielded from taxation at the partnership level by non-cash deductions that reduce taxable income allocated to limited partners. Depletion deductions for declining reserves, tangible asset depreciation for pipelines and equipment, and intangible drilling costs for ongoing drilling programs all reduce the partnership’s taxable net income.

As a result of these deductions, a limited partner in an MLP might receive $1.00 in cash distributions but have only $0.20 or less in taxable income. The untaxed portion of a distribution is considered a return of capital, which reduces the limited partner’s cost basis in their MLP units rather than subjecting it to current tax. Taxes are deferred until the limited partner sells their units, at which point the sale is subject to capital gains treatment for tax purposes. Also, if the investor’s cost basis in their units reaches zero, future distributions are taxed as capital gains.

The upshot is that limited partners stand to earn high cash yields on their common unit investment without paying much current income tax.

An upstream MLP like MNR differs from the more common midstream MLPs by its highly variable cash flow stream and distributions. Midstream MLPs typically generate more stable cash flows due to their fee-based model and lack of commodity price exposure. This is why they are capable of maintaining a stable quarterly distribution for many years.

Since most MLP investors own and understand midstream entities, they tend to favor more predictable yields. This tendency among MLP investors generally may cause MNR units to trade at a relative discount, but the lower multiple will also translate into a larger distribution yield. Longtime HFIR Energy Income subscribers will appreciate my fondness for owning higher-yielding, growth-oriented MLPs. Depending on one’s long-term outlook for oil and natural gas prices, MNR could be an attractive candidate.

Risks

Lower commodity prices and lower-priced hedges will likely limit MNR’s distributable cash flow over the next few quarters. However, even without hedges, if oil prices remain in the mid-$60s per barrel and Henry Hub natural gas trades around $3.00 per mcf, investors buying the units at their current price of $14.30 are likely to obtain a 5% distribution yield on their investment, with a high probability of much higher distributions when oil and natural gas prices increase to levels that incentivize additional marginal supply.

The primary risk to MNR unitholders stems from the company’s leverage. Leverage isn’t high, so the issue isn’t a high leverage ratio. Rather, risk resides in the structure of MNR’s reserve-based lending arrangement. The company’s long-term debt is limited to its reserve-based revolving credit facility, which has an initial borrowing base and commitment amount of $750 million and a maximum commitment amount of $2.0 billion. Borrowings on the facility are secured by all of the company’s assets. The facility is redetermined semi-annually in April and October and has a maturity date of February 27, 2029.

As of the end of the second quarter, MNR had $565 million drawn on the facility. The recent asset acquisitions will draw up to $525 million from the facility. MNR could emerge from the acquisitions with $1.1 billion in long-term debt. If commodity prices stay low, this level of debt could exceed the one-time Adjusted EBITDA, which the company considers its maximum acceptable leverage ratio.

The reserve-based nature of MNR’s long-term borrowings introduces the risk that unitholder value is impaired if persistently low commodity prices reduce the value of the reserves that serve as collateral. E&Ps typically transition away from this model and toward term debt, and I’d expect MNR to follow suit as it increases the scale of its operations.

Due to the vulnerabilities inherent in the reserve-based lending model, if commodity prices remain low, MNR could opt to allocate cash flow toward deleveraging instead of distributions. I’d support this approach, as it would lower the risk of permanent loss to unitholders and mitigate other risks associated with the company’s strategy. However, any cash flow put toward deleveraging would detract from the company’s capacity to pay quarterly distributions. A lower quarterly distribution could cause MNR’s unit price to decline.

Another risk to MNR unitholders is that low commodity prices could reduce the appeal of the units to MLP investors, causing the units to underperform and/or trade at a persistently low multiple. MNR’s model requires access to equity capital to fund new acquisitions, so a persistently low unit price could hinder MNR's ability to successfully execute its strategy.

There is also a risk that sellers of assets to MNR dump their units shortly after receiving them as consideration, thereby depressing the market price of MNR units. Fortunately, the company has addressed this risk in its recent deals by requiring sellers to refrain from sales for six months.

MNR faces the risk of a shrinking pool of private entities willing to sell to it—or to anyone else, for that matter—at today’s low commodity prices. If MNR cannot find attractive acquisition targets, management may be pressured to acquire properties for more than they’re worth. Furthermore, without additional accretive acquisitions, the company’s production would continue to deplete its PDP and proved reserves. Eventually, its units would trade at a discount to reflect the prospect of depletion.

All the risks enumerated above are substantially offset by management’s extensive experience in the energy industry. It can draw from the many cautionary tales in the annals of poorly-managed upstream MLPs. Linn Energy, in particular, stands out in my mind.

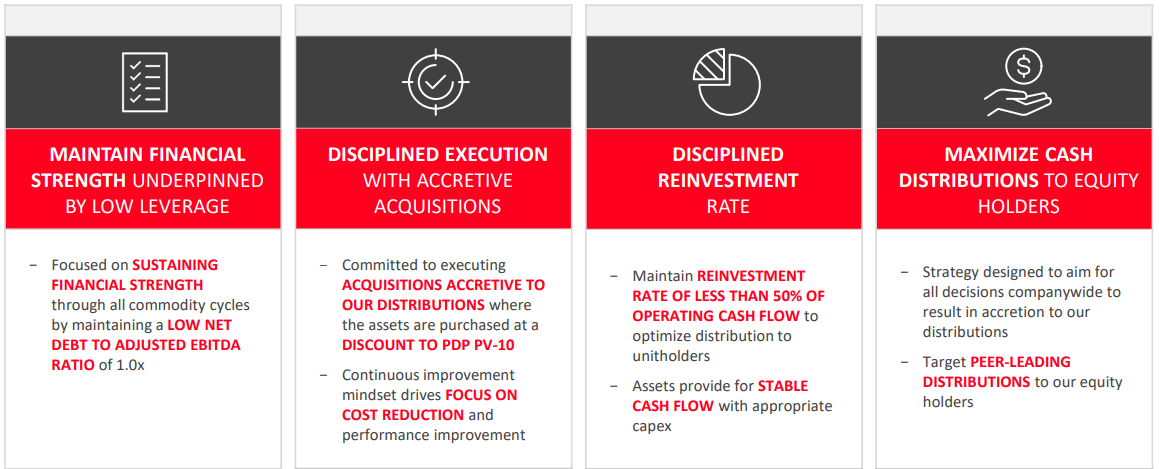

Management’s knowledge of industry history is likely to compel a more conservative approach and ensure that the company retains enough capital to fund production while maintaining access to cheap capital to fund acquisitions. In fact, its “four pillars” seem designed to avoid the mistakes made by others who adopted a similar strategy and structure.

Source: Mach Natural Resources Q2 Earnings Presentation, August 2025.

MNR unitholders should carefully monitor the company’s adherence to its pillars over their holding period. Given what’s at stake for heavily invested insiders, I don’t anticipate this becoming an issue.

Improved Partnership Governance

In light of MNR’s MLP status, governance could be thought of as a risk, as many MLP investors are familiar with the entity’s various governance weaknesses. Since MLPs were introduced in the energy sector on a wide scale in the early 2000s, unscrupulous operators have used it to profit at the expense of limited partners.

I don’t regard governance as a concern for MNR common unitholders. The company does not have incentive distribution rights that disproportionately allocate distributions to the general partner and away from limited partners. Additionally, MNR’s general partner has no economic interest in the MLP. As a result, the general partner isn’t likely to receive disproportionate benefits in the event of a conversion from MLP to a C-corporation, should such a conversion occur.

Like other MLPs, outside passive minority investors in MNR cannot nominate independent directors, but risks to these limited partners in MNR are offset due to the entity’s high percentage of insider ownership. Their interests are therefore aligned with outside passive investors. Consider that affiliates of MNR’s chief sponsor, Bayou City Energy Management, own 49.4% of Mach’s outstanding units, and CEO Tom Ward beneficially owns 9.4% of the common units after the deal. Any action these insiders take to harm limited partners would also directly harm them.

Valuation

MNR is difficult to value at the moment because the company hasn't issued guidance in connection with its newly acquired assets. Until the deals close, likely later this quarter, many operational and financial details will remain unknown.

My MNR valuation assumes that operating expenses decrease marginally in the post-acquisition entity. Interest expense is significantly higher on a per-boe basis, as are midstream expenses. I assume annual capex of $430 million.

Hedges have played a key role in supporting the company’s cash flows during times of weak commodity prices. Before taking account of the recent acquisitions, approximately 40% of MNR’s oil production in the second half of the year is hedged at an average price of $68.26. About 44% of second-half natural gas production is hedged at $3.8 per MMBtu.

Inclusive of legacy hedges and assuming WTI of $65 per barrel and Henry Hub natural gas of $3.00 per mcf, the company’s units at $14.30 generate an approximately 11.3% free cash flow yield. MNR’s second-quarter distribution of $0.38 per unit is roughly 110% covered by free cash flow.

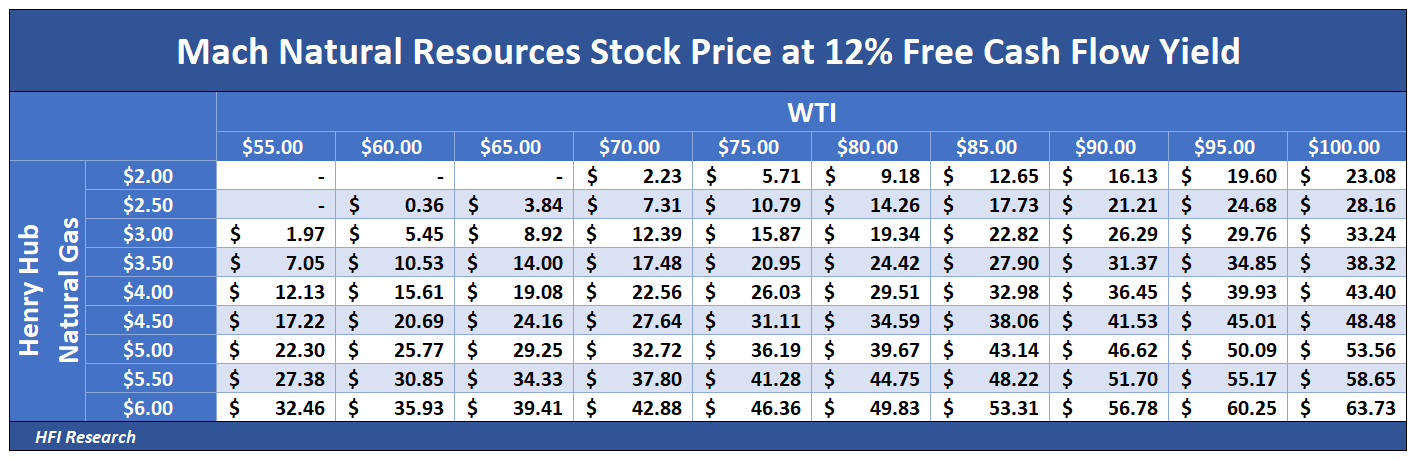

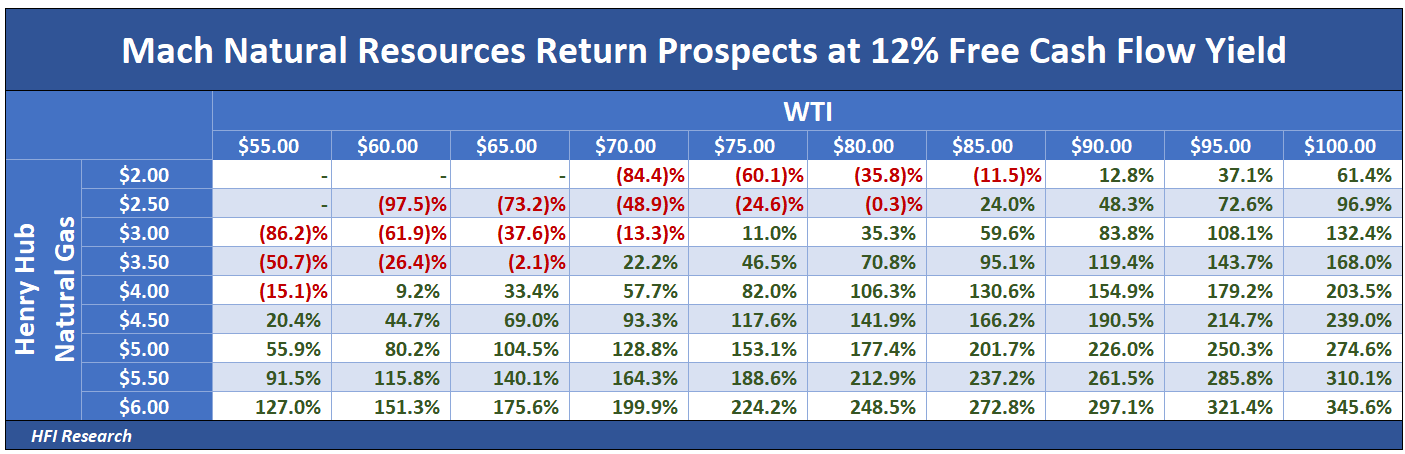

Without hedges, MNR under the above assumptions generates a 7.5% free cash flow yield—not too shabby in the current environment of low commodity prices. The following—admittedly rough—unit price estimates assuming a 12% free cash flow yield follow from my valuation.

The table below depicts the returns on offer from the current $14.30 unit price. The figures reflect free cash flow, not returns generated from cash distributions. However, they do reflect distributions if the company paid out all of its free cash flow.

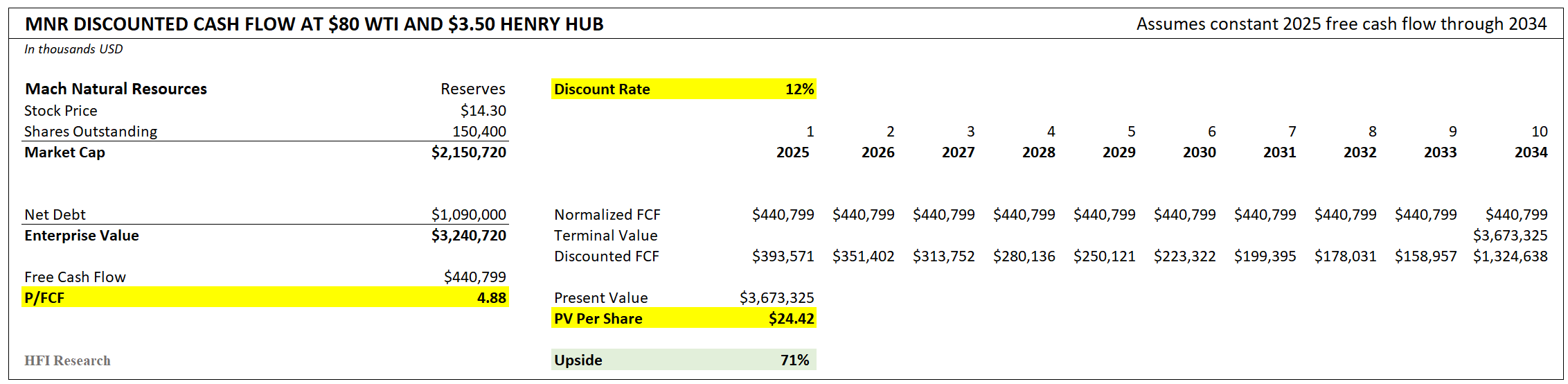

Assuming a long-term average WTI price of $80 per barrel, Henry Hub natural gas price of $3.50 per mcf, and using a 12% discount rate, results in a valuation of $24.42 per share for MNR, implying 71% upside from the current price of $14.30.

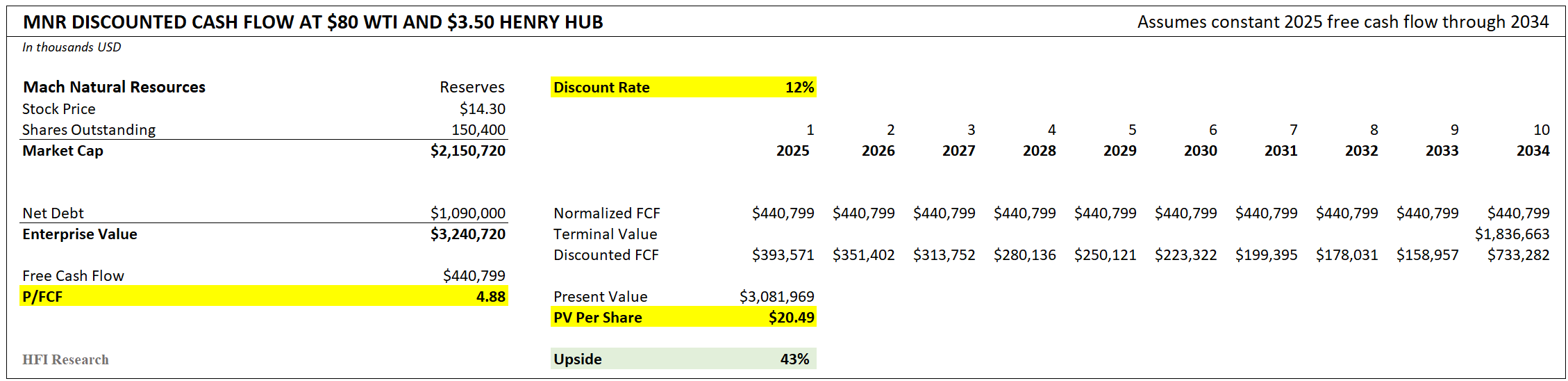

Reducing the terminal rate by half to reflect the company’s reserve life results in a value per share of $20.49, implying 43% upside from the current price.

MNR’s hedges stabilize its cash flow in what has been a volatile and at times tumultuous 2025. The stable cash flow has enabled the company to acquire attractively-priced assets and remain in good standing with regard to its lending syndicate and debt covenants.

MNR’s distributions are likely to fall next year unless WTI averages more than $68 per barrel and Henry Hub natural gas prices average $3.00.

Regarding reserve life estimates, using MNR’s pro-forma disclosures for the newly acquired acreage, its PDP reserves now extend 10.3 years, up from 8.4 years before the transactions.

Before the recent acquisitions, MNR’s proved reserve life was 11.4 years, based on the company’s full-year guidance of 81,000 boe/d production. The company has not provided enough information to determine proved reserves after the deal. PV-10 for MNR’s reserves cannot be estimated because the PV-10 values of the acquired entities have not been disclosed.

Conclusion

MNR should be considered as a potential long-term holding for investors who seek a large income return with the prospect for significantly higher returns at high commodity prices. Due to the risks stemming from the company’s high payout ratio and reserve-based borrowing model, investors must exercise caution in sizing an MNR position appropriately. I recommend a smaller weighting of no more than 3% in a portfolio, at least until the company can deleverage and/or reduce risk stemming from its debt. Given MNR’s significant cash flow torque, even a small weighting can have an outsized impact on a portfolio’s performance if commodity prices rise.

We’ll be monitoring MNR’s progress over the coming quarters and years. I’m keeping dry powder available in my HFI Research Energy Income Portfolio and stand ready to buy these units amid a selloff.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in MNR, over the next 72 hours.