(Idea) Kronos Worldwide

By: Jon Costello

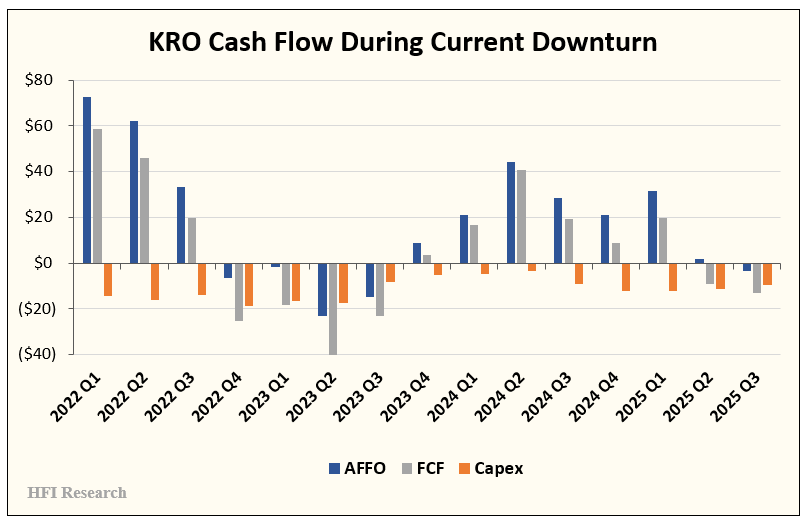

Kronos Worldwide (KRO) is experiencing a brutal downturn in the titanium dioxide industry. Lower sales prices and volumes have caused its earnings and cash flow to go negative for multiple quarters over the past few years, including the recently reported third quarter.

The downturn began in 2022, when higher feedstock costs for titanium dioxide producers coincided with weakening demand from major customers. Since then, KRO and its peers have experienced declining and weak free cash flow.

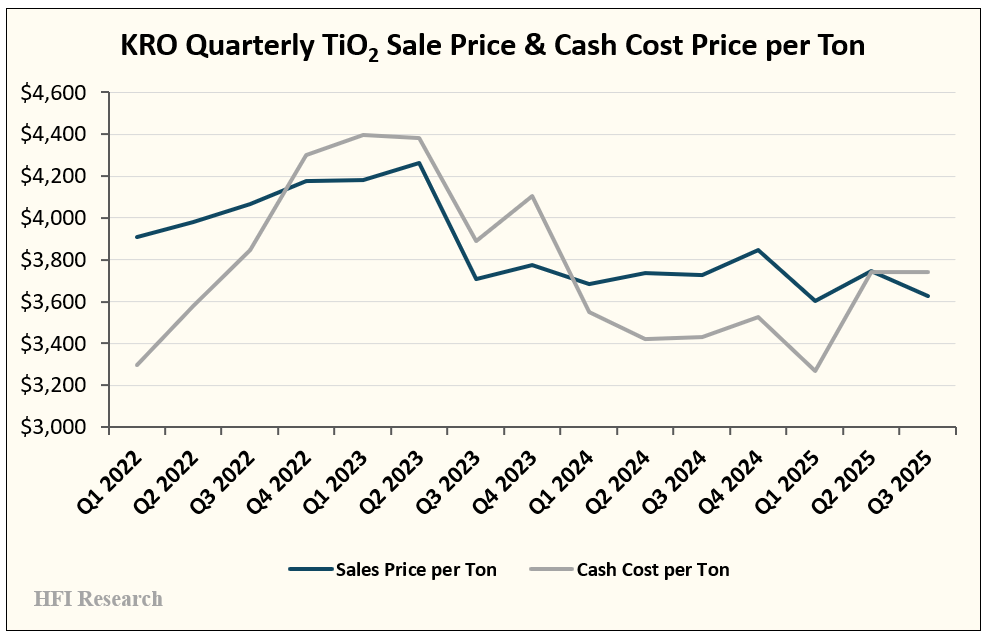

The weakness was caused by excess supply amid tepid demand. In this environment, KRO’s sales prices struggled to keep pace with rising per-ton costs.

Operating conditions have intensified recently for the entire titanium dioxide industry, prompting additional retrenchment among producers during the third quarter. However, the clear takeaway is that current margins are unsustainable. It is only a matter of time until the market recovers.

Low prices have already led to unprecedented curtailments in global production volumes. The industry’s production capacity has declined. Titanium dioxide inventories are low. Anti-dumping tariffs have removed the primary source of low-cost supply. These and other factors are likely to usher in higher prices. Eventually, producers will have to increase their production volumes, at which point operating leverage will inflect higher.

I expect cyclical factors to usher in a cyclical recovery in 2026. KRO is likely to enter that period with a strengthened competitive position and enhanced profitability potential relative to its peers. Recovering profits and cash flow will send its shares higher.