(Idea) InPlay Oil

Editor’s Note: Please note that this article was first published to HFI Research main subscribers on Feb 3, 2024. Market data in this article will appear outdated as a result.

Note: Dollar references are to Canadian dollars unless otherwise specified.

InPlay Oil (IPO:CA) is a Canadian E&P with a technical management team that is growing production through the drill bit. In 2023, it produced approximately 9,000 boe/d, comprised of 41% crude oil, 16% NGLs, and 43% natural gas.

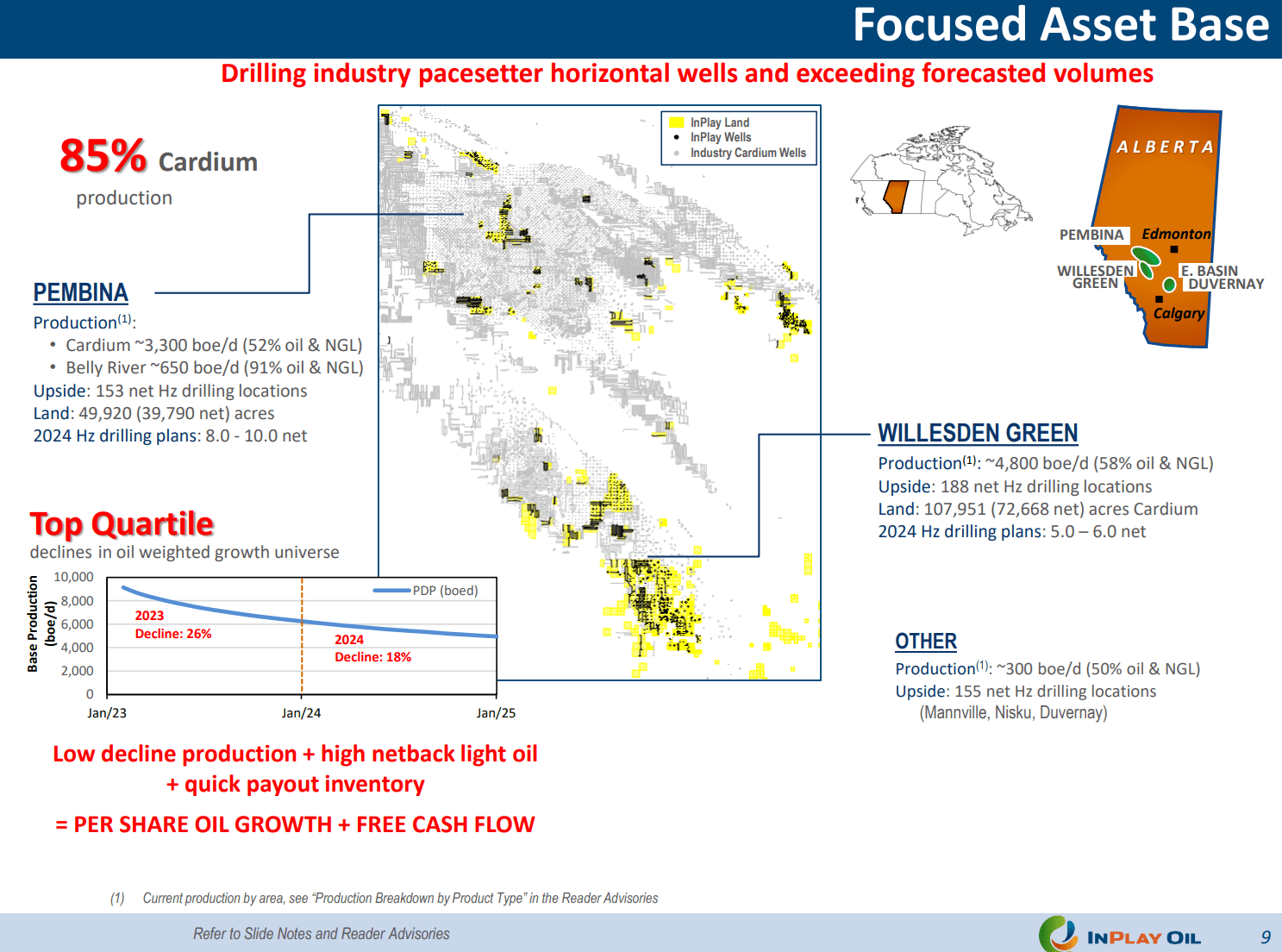

The company’s operations are focused primarily on the Pembina and Willesden Green plays of the Cardium in Alberta, which account for 85% of its production. East Duvernay production accounts for the remaining 15%.

InPlay’s assets are shown in the map below.

Source: InPlay Oil, February 2024 Investor Presentation.

The most attractive feature of InPlay’s stock is its high dividend yield. The company intends to pay the dividend on a monthly basis throughout 2024. Its $0.18 per share annual payout represents an attractive 8.5% yield on InPlay’s $2.13 market. We estimate InPlay generates enough free cash flow to pay its dividend down to US$73 per barrel WTI, which is quite low for a small E&P.

InPlay’s organic growth strategy is facilitated by its approximately 18 years of proved and probable reserves. Its targeted plays have significant oil in place and low recovery factors that management is intent on increasing. The company drills repeatable, low-risk horizontal infill wells and uses water floods to enhance recovery. These wells require little infrastructure investment. Its Pembina and Willesden Green wells boast first-year capital efficiencies in the low-$20,000 range. Its overall capital efficiency stands below $16,000, significantly better than most Canadian E&Ps.

Capital Allocation: Prudent and Conservative

Management has been disciplined with regatd to capital allocation. Its discipline can be seen in its approach to acquisitions.

After InPlay entered the Cardium play by acquiring publicly-traded Anderson Energy and a separate Caridum asset deal in 2016, it has made only two subsequent acquisitions. The first was a 240 boe/d acquisition of Cardium acreage in November 2020, which was made at a rock-bottom price of $7,900 per flowing boe in a depressed market.

One year later, InPlay acquired publicly-traded Prairie Storm Resources, a 1,800 boe/d producer focused on the Willesden Green area of the Cardium, for $42.3 million. The deal was made at an attractive $23,500 per flowing boe and at 1.3-times operating income.

The deal was attractive from an asset perspective. Prairie Storm’s assets were complimentary with InPlay’s. Its 18,500 net acres of undeveloped acreage and 21-year proved and probable reserve life improved InPlay's near-term and longer-term production growth prospects. The addition of Prairie Storm’s 4.9 million barrels of PDP and 21.3 million boe of proved and probable reserves increased InPlay’s own PDP and proved and probable reserves by 50% and 65%, respectively. Furthermore, Prairie Storm’s production declined at a low 10% annually, reducing InPlay’s average decline rate.

InPlay financed its Prairie Storm acquisition mostly with debt. Equity dilution to its shareholders in the deal was only 12%. The debt it took on to finance the deal was ultimately paid down in 2022 amid elevated commodity prices.

The deal’s positive impact on InPlay’s production, reserves, and those same metrics on a per-share basis can be seen in the charts below.

Source: InPlay Oil, February 2024 Investor Presentation.

This was clearly a good deal for InPlay. It checked all the boxes in advancing management’s stated objectives. Going forward, we expect InPlay to continue to be disciplined with regard to acquisitions due to management's technical bent and the company's long reserve life, both of which relieve the pressure to pursue a deal over at least the next few years.

Significant Oil Price Torque

Inplay offers significant torque to higher oil prices, though less than Baytex Energy (BTE) and Crescent Point Energy (CPG). What it does offer, however, is a higher dividend yield than either of these larger E&Ps. Moreover, InPlay’s dividend is sustainable down to relatively low oil prices, which makes the 8.5% payout attractive as long as oil prices remain in the mid-$70s per barrel or higher. We expect higher oil prices over the balance of 2023, so InPlay’s shares are among the most attractive E&Ps for income-seeking investors.