(Idea) Genesis Energy - The Only Independent Gulf Of America Pipeline Operator Is At An Inflection Point

By: Jon Costello

Please see the previous write-up on Genesis Energy.

Genesis Energy, LP GEL 0.00%↑ has quietly transformed itself over the past 18 months. The company sold its soda ash business for $1.425 billion, used the proceeds to dramatically clean up its balance sheet, and is now a focused Gulf of America pipeline company with two transformational deepwater projects ramping into full production. At $17.60 per unit, GEL trades on a 4.1% yield with trailing EBITDA of $544 million and 15–20% guided growth into 2026. Distribution coverage sits at 2.77x. The market is still pricing GEL units as a leveraged turnaround, but the inflection has already happened, as I have discussed in previous articles.

GEL is one of the more attractive risk-reward setups in midstream today. The company controls critical infrastructure that every deepwater Gulf of America producer depends on, and the market is still anchored to an old narrative regarding leverage and complexity that no longer applies. While the unit price is up 37% over the past twelve months, it remains well below its pre-pandemic levels, implying the re-rating is underway but far from complete. Analysts target $19.33. I think intrinsic value is meaningfully higher.

GEL’s High-Quality Assets

Post-divestiture, GEL operates three segments: Offshore Pipeline Transportation, Marine Transportation, and Onshore Transportation Services. The offshore network spans roughly 1,400 miles of crude oil pipeline and 764 miles of natural gas pipeline in the Gulf of America. Key assets include its 64% owned Cameron Highway Oil Pipeline System, or “CHOPS,” which spans some 400 miles with more than 700,000 barrels per day (bpd) of design capacity, its 64% owned Poseidon system in the central and western Gulf, its 29% owned Odyssey system in the eastern Gulf, and its 100% owned SYNC system, which spans 105 miles and is dedicated to the Walker Ridge area and Shenandoah. GEL’s revenue is tariff-based on life-of-lease dedications with long-term contracts. Less than 5% of its gross margin is derived from take-or-pay minimums, as its customers actively use its pipelines, indicating its assets are competitively positioned.

What makes GEL special is that it’s the only independent crude oil pipeline operator in the Gulf of America. Shell (SHEL) and BP (BP), the two largest producers in the Gulf, are integrated operators, which creates inherent conflicts. For instance, when Shell owns a pipeline and also produces the crude that flows through it, the third-party producer shipping on that same system knows they’re not the priority customer. Since GEL has no upstream production, its incentive is purely commercial, namely, to maximize throughput at competitive tariff rates. That independence serves as a structural moat, which becomes more valuable in exactly the kind of tight supply environment we’re in now.

The Balance Sheet Transformation

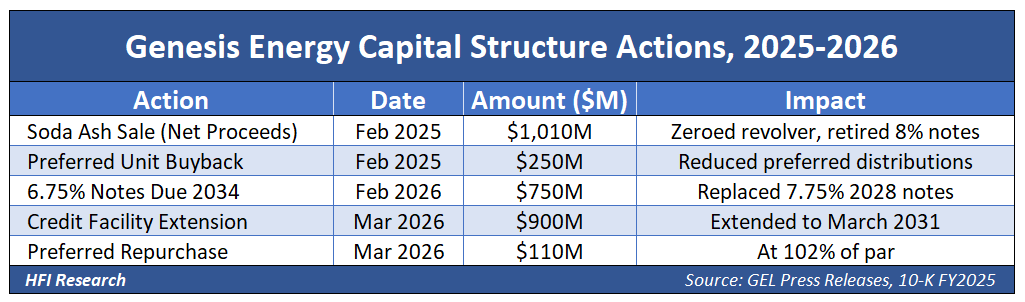

In February 2025, GEL closed the sale of its soda ash operations to WE Soda for $1.43 billion gross and $1.01 billion net. The company immediately paid down its $800 million revolver, redeemed $406 million of 8.0% senior notes due 2027, and repurchased $250 million of preferred units. Annual capital cost reduction: over $120 million. This was GEL trading a cyclical commodity business for balance sheet freedom at exactly the right time.

Since then, GEL has continued cleaning house. It issued $750 million of 6.75% notes due 2034, replacing 7.75% notes due 2028 and saving $12 million in cash interest per year while extending the maturity wall by 6 years. The credit facility was extended to 2031 and expanded to $900 million.

In March 2026, the company repurchased another $110 million of its preferred units at 102% of par. The upshot is that the company has no material debt maturities until early 2029, a minimal revolver balance, and bank leverage of 5.12x, which is poised to compress as EBITDA grows. At a 15% to 20% EBITDA growth rate, the math gets GEL to sub-4.5x leverage by late 2026 without any additional asset sales. That is an investment-grade trajectory.

Shenandoah And Salamanca Change Everything

The core of GEL’s bull case is that the Shenandoah oil production platform, a 120,000 bpd deepwater platform expandable to 140,000 bpd, delivered first oil in July 2025 and reached 100,000 bpd within 75 days from just four Phase 1 wells. It accomplished this feat more quickly than industry consensus expected. Shenandoah’s output connects directly into GEL’s 100%-owned SYNC pipeline. Meanwhile, the Salamanca oil production platform adds another 50,000 bpd of nameplate capacity, with first oil in September 2025 and three wells currently ramping toward 40,000 bpd. Together, these projects are expected to generate approximately $150M in incremental annual segment margin once at full production, representing a 27% uplift to the company’s baseline EBITDA. This is not a projection. It is occurring right now.