(Idea) First Quarter Review And Thesis Check-Up For Transocean, Cheniere Energy, And New Stratus Energy

Editor’s Note: Suncor, Chemours, and Mach Resources update will be published on Monday.

By: Jon Costello

Transocean Q1 2026 Thesis Check-Up

Transocean RIG 2.24%↑ reported first-quarter results on Monday, May 4. Despite its strong performance, its shares declined by 8.3% on the day in response to the news.

Utilization and Dayrates Confirm the Cyclical Component of the Investment Thesis

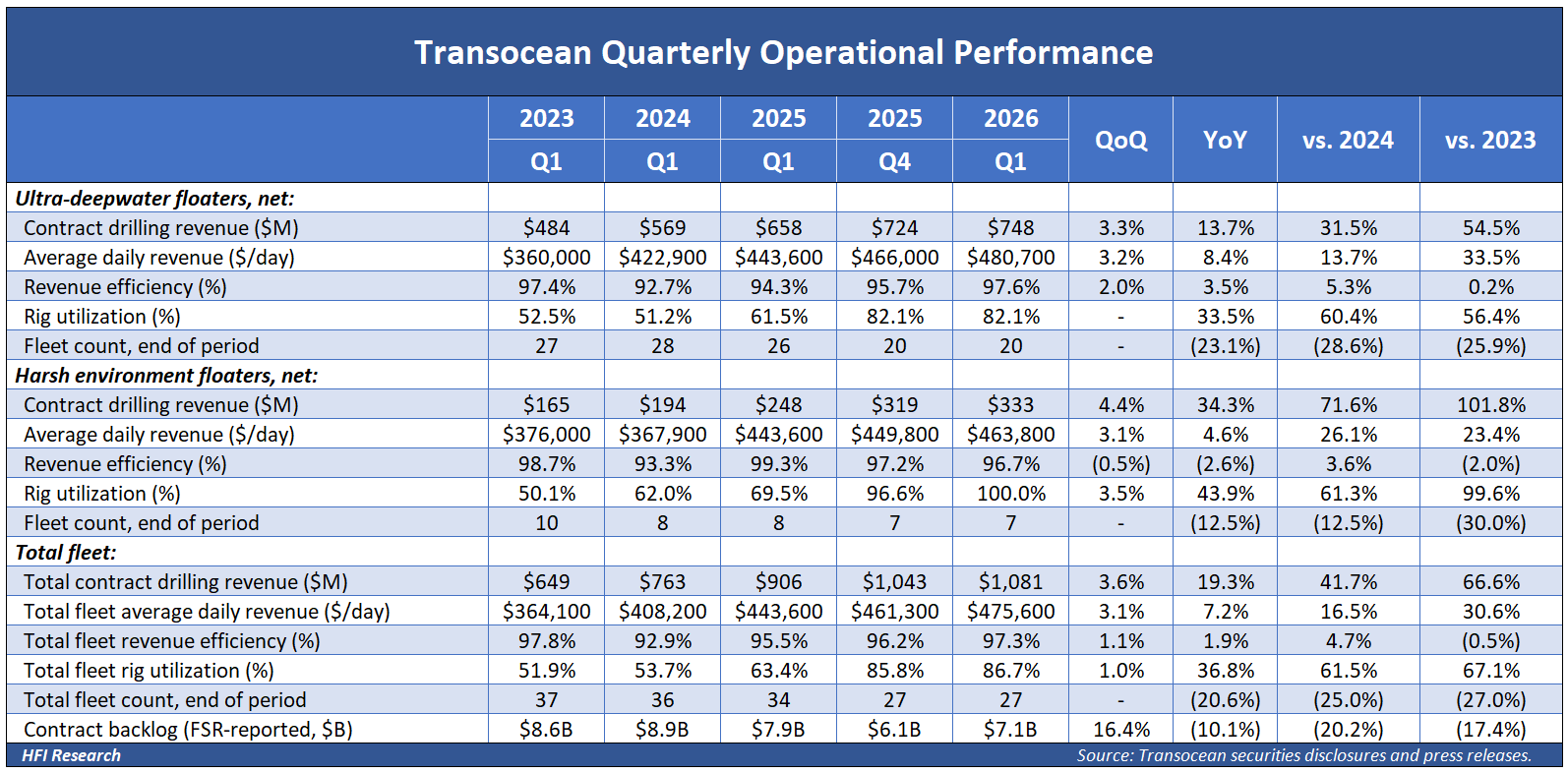

Transocean’s first quarter provided the cleanest read on operating leverage in years. Total fleet rig utilization reached 86.7% in the first quarter of 2026, up from 63.4% one year earlier and 51.9% three years earlier. A large share of that improvement occurred as the total fleet count fell from 37 units to 27 over the same three-year timeframe. In 2024, the company disposed of three older floaters and, in 2025, six ultra-deepwater drillships. In the first quarter of 2026, it sold the Discoverer India and Deepwater Champion for $27 million in aggregate net cash proceeds. That is the lever the disciplined-contracting thesis called for. A smaller, higher-spec fleet keeps utilization elevated as the cycle progresses, thereby improving the per-rig economics that ultimately flow down to shareholders.

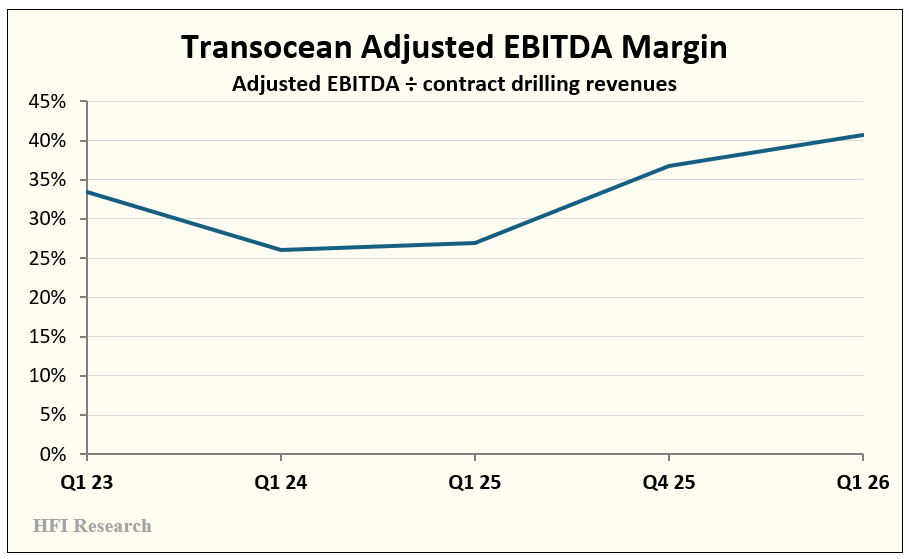

Adjusted EBITDA margin went from 26.9% in the first quarter of 2025 to 40.7% in the first quarter of 2026. In dollar terms, the margin increased by $175 million, indicating that roughly 112% of incremental revenue dropped down to EBITDA.

The trend of higher Adjusted EBITDA margin is another illustration of Transocean’s emerging operating leverage. In the first quarter, the higher margin was driven by 19.3% increase in revenue amid lower costs. Fleet rationalization drove most of the improvement. Some of the revenue increase during the quarter was attributable to revenue being pulled forward, but this does not materially change the picture.

Daily revenue also supports the trend of increasing operating leverage, as the total fleet average daily revenue increased from $443,600 in the year-ago quarter to $475,600 in the first quarter, the highest quarterly average in over a decade, according to CEO Keelan Adamson. Leading-edge contracts are landing at $450,000 per day on the Var Energi (VARRY) contract for the Transocean Barents, in line with the current fleet average.

Additional upside should come from sector tightening rather than catch-up to the leading edge. The operating-leverage payoff is a key part of my Transocean investment thesis, which I outlined in my previous Transocean articles.

Balance Sheet Improvement Ahead of Schedule

Deleveraging is running ahead of schedule. Total debt at quarter-end was $5.137 biillion, down $549 million from $5.686 billion at year-end 2025, and down $1.597 billion from $6.734 billion one year earlier. The major debt transaction in the quarter was the March redemption of the 8.375% Senior Secured Notes due February 2028. Transocean paid $365 million in cash, including the early-redemption premium, to retire the $358 million remaining principal balance, thereby reducing future interest expense by approximately $40 million through maturity. CFO Robert Vayda guided to retiring at least $750 million of total debt in 2026, ending the year with approximately $4.9 billion in principal and trailing net-debt-to-EBITDA of approximately 3.3x. That leverage ratio is well within the 3.5x target management gave for late-2026 on the second-quarter 2025 call.

The Valaris (VAL) transaction will significantly accelerate the deleveraging process two years out. Management is targeting approximately 1.5x leverage within roughly 24 months of close on a pro forma backlog of approximately $12 billion. Cost synergies are guided at more than $200 million, which is incremental to the company’s $250 million cost-reduction program. Two years from now, Transocean’s consolidated leverage profile will approach the kind of investment-grade profile I described in my previous Transocean investment thesis articles.

Backlog, Market Trends, and Benefits of the Valaris Deal

The forward setup is the strongest I have seen over my multiple years of covering the name. Firm contract coverage stands at 86% for 2026 and 73% for 2027, and Chief Commercial Officer Roderick Mackenzie noted that the year-to-date average award duration of 480 days is double the full-year 2025 average. That is a clear signal of a tightening market. Market commentary on the call was markedly more constructive than at any prior point during my coverage. Mackenzie forecasted offshore capex rising from approximately 13% of operator capex toward nearly 30% by 2028 and approaching $100 billion annually by 2030. Adamson stated that he expects deepwater utilization to approach nearly 100% by the end of 2027.

The offshore capex turn I wrote about in my Transocean articles is now showing up in the data. The Valaris combination delivers the structural benefits I described in my February article. Pro forma, Transocean owns 73 rigs, including 33 drillships, which represent roughly one-third of the marketed global drillship fleet. Adding jackup cash flow, geographic reach into the Middle East, North Sea, and Latin America, and a lower cost of capital reduces the odds of another dilutive equity offering.

The wrinkle in the first-quarter report was the news that the U.S. Department of Justice issued a second information request on May 4 in connection with the deal. I suspect this news—which was perceived as negative for the prospects of the deal’s consummation—is what sent the shares lower during the session, which fits the price action better than anything in the operating numbers.

I’m not concerned about the deal’s prospects. I don’t expect the authorities to ultimately stand in the way of this deal. CEO Adamson characterized the second request as “part of the process,” while reaffirming a second-half 2026 close, and noting that prior conversations with the Department of Justice had been “going very well.” The deleveraging path remains intact.