(Idea) Enterprise Products Partner - The Move Higher Is Just Getting Started

By: Jon Costello

For longtime holders of Enterprise Products Partners (EPD) like us, it seems like EPD units remaining under $30 is as certain as death and taxes.

Today’s price action is putting this adage to the test. EPD’s strong third-quarter results appear to be providing momentum for its units to break above their dreaded $30 resistance. This time, I believe the breakout will be sustainable.

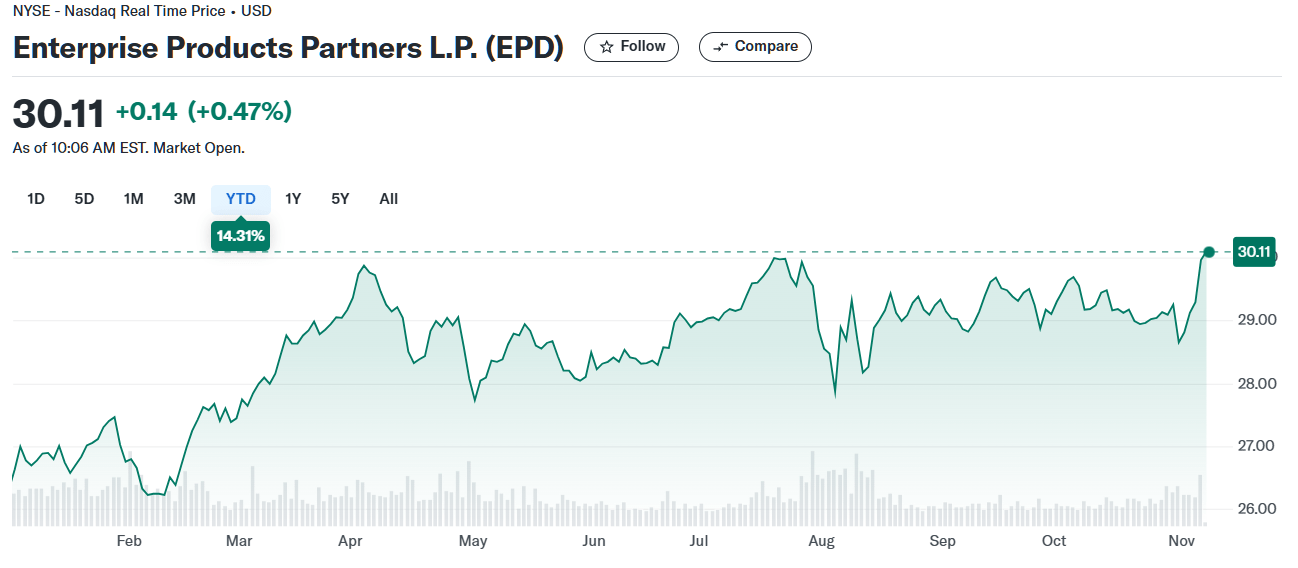

EPD’s $30 ceiling is evident in the year-to-date unit price chart.

Source: Yahoo! Finance, Nov. 6, 2024.

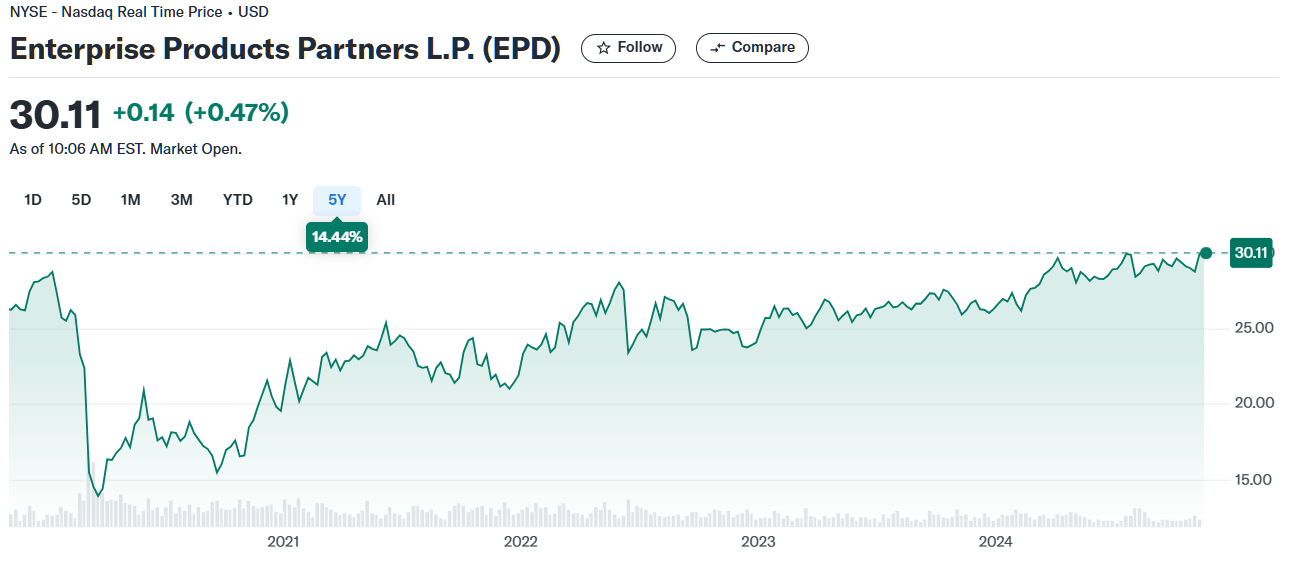

The upward momentum has been building since 2019, the last time EPD units traded close to $30.

Source: Yahoo! Finance, Nov. 6, 2024.

These units are too cheap, based on virtually any valuation metric. What they have going against them is their status as an MLP, I think indisputably the most hated asset class in the world. But they have so much going for them that I believe a higher unit price is next to inevitable.

A Trump win is another positive that is working in EPD’s favor. With the favorable regulatory regime the incoming Trump administration will bring, the avenues the company can pursue to achieve high-return growth will only expand from here.