(Idea) Comstock Resources

Note: This article was first published to HFI Research main subscribers on April 26, 2024. This is an archive post for subscribers in this service.

Investors should avoid Comstock Resources (CRK). There is no reason to reach for investment profits with such a name when downside risks loom large and attractive alternatives abound. The company’s few positive attributes are overshadowed by glaring negatives that keep us far away from the shares. In fact, after taking a closer look at the company, we consider it to be one of—if not the—worst-managed shale E&P in North America.

We believe CRK could be an attractive short for investors seeking to hedge their long natural gas exposure or speculate on a prolonged bout of low natural gas prices. But all others should avoid the shares in favor of Spartan Delta (SDE:CA), Tourmaline Oil (TOU:CA), or Birchcliff Energy (BIR:CA).

CRK Shareholders are at Risk

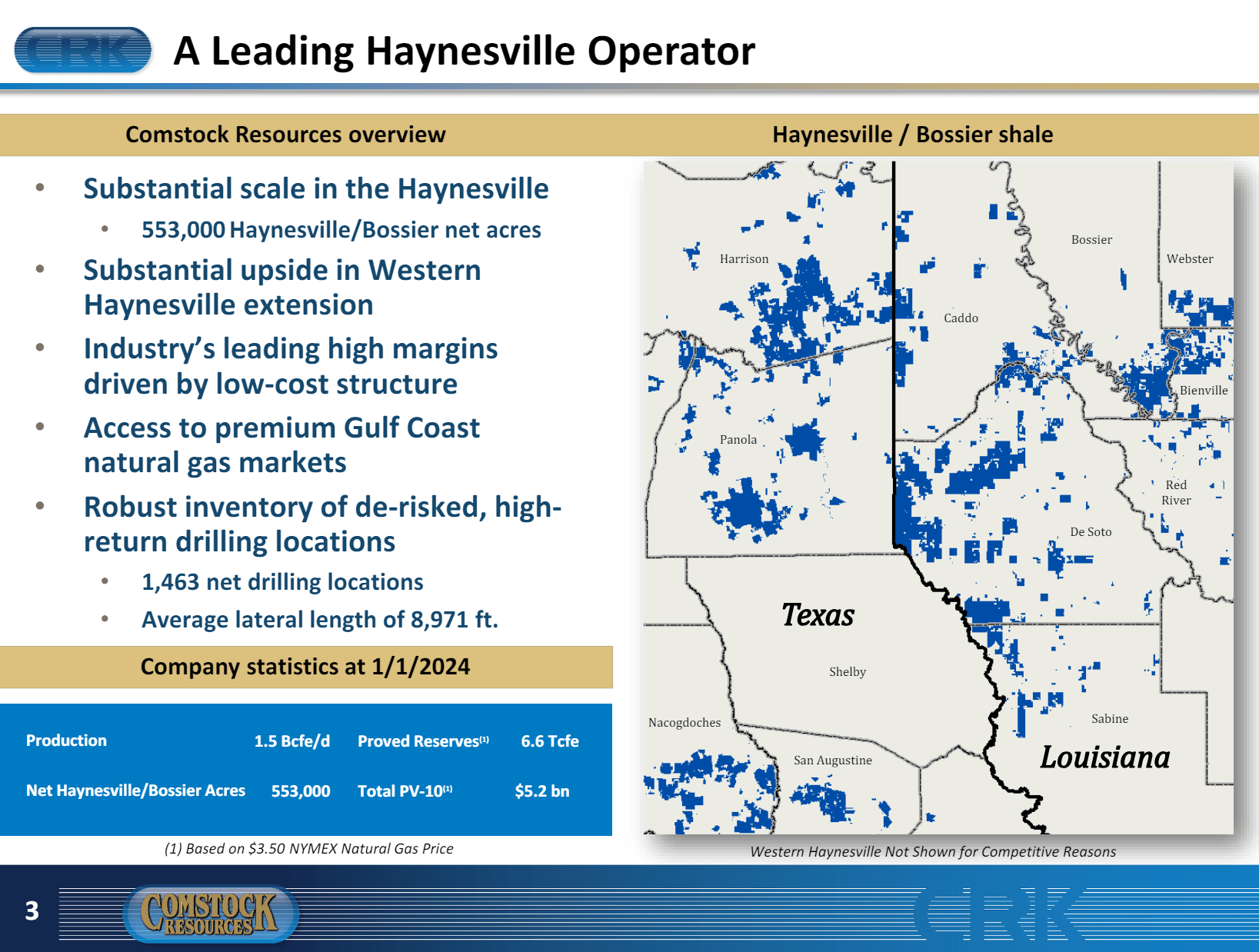

CRK’s positives touted by management are its core acreage position in the Haynesville and Bossier shales plays in Louisiana and Texas, as well as its 25 years of drilling inventory at current production rates. The company has also proved successful at growing its reserves. In 2023, it replaced 109% of 2022 production with new reserve additions despite lower average prices during 2023.

Management’s overview is shown below.

Source: CRK April 2024 Investor Presentation.

In 2023, Henry Hub natural gas prices averaged $2.74 per mcf. CRK generated $1.02 billion in operating cash flow during the year while spending $1.43 billion on capex. It funded its $410 million cash flow deficit through cash on hand, selling $41.3 million of assets, and increasing borrowings on its credit facility by $590 million. It ended the year with $16.7 million in cash.

As it entered 2024 with extremely low prevailing natural gas prices, its high debt balance put it at risk of violating covenants on its revolving credit facility if natural gas prices remain flat at current prices for several quarters.

In response to the concerning financial situation, management switched gears to “batten down the hatches,” as Chairman and CEO M. Jay Allison claimed on CRK’s fourth-quarter 2023 earnings conference call, held on February 14. It released one frac crew and two rigs while suspending its quarterly dividend to retain the $140 million of cash dividend payments. It also reduced full-year capex from $1.45 billion in 2023 to around $900 million this year. We suspect that the reduction in drilling activity this year will translate into lower production in 2025.

The problem for CRK is that it needs significantly higher natural gas prices to generate free cash flow. Based on management’s guidance, we estimate the following price sensitivity to natural gas prices. Its $200 million interest expense, in particular, increases cash flow breakeven considerably. We estimate cash flow breakeven at 2024 capex of $900 million to be approximately $3.10 per mcf. That’s a far cry from today’s $1.61. Clearly, at the current price, CRK will burn significant amounts of cash. Once it draws down its cash, it could be forced to issue shares or sell valuable assets.

Despite these risks, the company continues to spend on expanding and proving up its Western Haynesville acreage. It is running two rigs in the area in 2024 to lay the groundwork to supply feedstock for LNG export facilities in the Gulf Coast that are set to arrive over the next few years.

We estimate that if natural gas averages $2.50 per mcf this year, CRK will end the year with a debt-to-EBITDA ratio of 2.8-times, below its revolving credit facility’s maximum net leverage ratio of 3.5-times. At the end of 2023, CRK had $480 million outstanding on its $1.5 billion facility, so if natural gas prices increase to $2.50 per mcf, it should be able to survive in decent shape. But if prices remain depressed around current levels, EBITDA will decline and drawings on the revolver will increase, pushing CRK’s leverage ratio closer to its covenants and calling survival into question.

Abysmal Capital Allocation

Jay Allison has been CRK’s Chairman and CEO since 1997. Over his tenure, he has presided over epic levels of value destruction. Since 2003, he has continuously raked up long-term debt to grow the company. Even in the good years, such as 2022, when he allocated free cash flow to pay down debt, debt continued to creep higher.