(Idea) Chord Energy - Cheap

By: Jon Costello

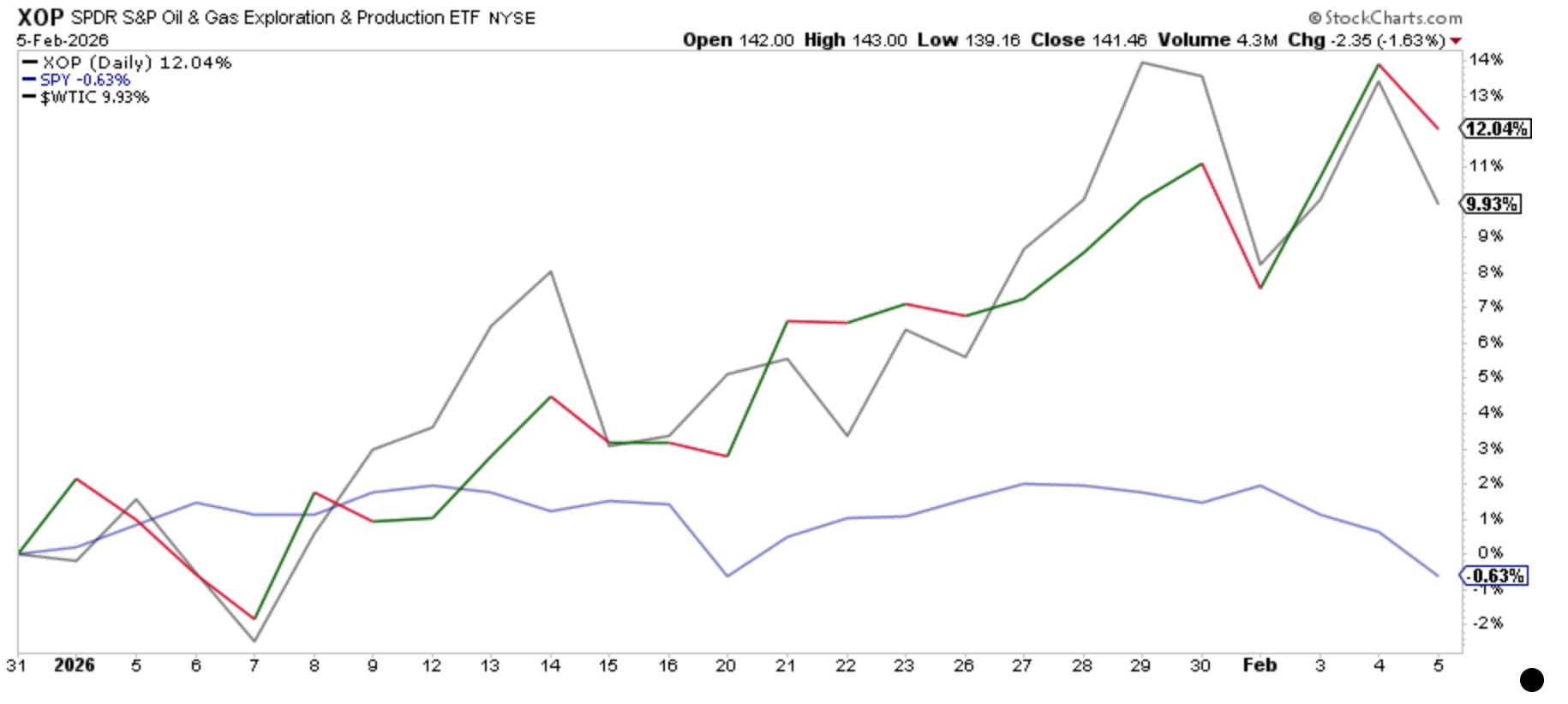

The E&P ETF, XOP 0.00%↑, has outperformed the S&P year-to-date by ~12%, mirroring WTI’s gains over the same period.

The ferocious run in the producer segment of the energy sector has left us wondering where opportunities might lie among the laggards. One of them is Chord Energy CHRD 0.00%↑.

Relatively speaking, CHRD has underperformed both XOP and WTI over the past 2 years.

Despite its stock’s relative underperformance, the company remains one of the better-managed independent E&Ps among shale producers. It has performed well in operations and financial performance for years and has amassed a substantial acreage position in the Williston Basin that will enable it to continue growing oil production and lowering costs, bucking the trends of gassier production and service inflation that beset many of its E&P peers.

Chord is the result of the combination of the legacy Whiting Petroleum, Oasis Petroleum, and Encana. It produces approximately 275,000 boe/d with production split 56%/19%/25% between crude oil, NGLs, and natural gas, respectively.

Chord is best viewed as a crude oil play, since its low price realizations for Williston Basin natural gas lessen the commodity’s revenue contribution. In the first three quarters of 2025, Chord earned 91%, 4%, and 5% of its revenue from crude oil, NGLs, and natural gas.

Chord has distinguished itself as a consistent operator. It raised oil volume guidance twice in 2025. At the same time, wells are coming in below initial cost estimates. The company has exceeded its quarterly guidance for lease operating costs while consistently driving them lower.

Chord isn’t using its newly acquired acreage to burnish its results. Excluding XTO assets, the company’s oil production grew by 800 bbl/d more than management’s initial guidance. Capex was $50 million below the company’s initial guidance, excluding the XTO assets.