(Idea) Chesapeake Energy - A Dominant Natural Gas Producer

We’ve followed Chesapeake Energy (CHK) since we first bought shares in 2013. Since then, the company has undergone seemingly endless strategic changes, which eventually led to its bankruptcy in June 2020 when commodity prices collapsed.

Today, the company and its operating environment have changed dramatically from a decade ago. The shale land grab is over, the industry has matured, and consolidation is well underway. After emerging from bankruptcy in February 2021, CHK has set itself up for success as a leading gas-focused producer. Since then, it has:

Emerged from bankruptcy with a long-term debt balance of $1.3 billion, down from $9.1 billion beforehand.

Acquired 724 MMcf/d Vine Energy for $2.2 billion, increasing its footprint in the Haynesville.

Acquired Chief E&D Holdings and other interests of Tug Hill in the Marcellus for $2.0 billion, adding 835 MMcf/d of natural gas production.

Sold its liquids-rich Powder River Basin assets in Wyoming to Continental Resources for $450 million.

Struck an agreement to sell 300 MMcf/d of LNG feedgas to the Golden Pass LNG terminal.

Sold liquids-rich Eagle Ford acreage that produced 27,200 boe/d to WildFire Energy for $1.43 billion.

Sold its remaining Eagle Ford acreage that produced 36,000 boe/d to INEOS Energy for $1.4 billion.

Agreed to supply 2 million tons per annum of LNG feedgas to Gunvor Group.

After these deals, CHK was tied with Antero Resources (AR) for second place among independent natural gas producers in the U.S.

CHK’s Major Transformative Deal

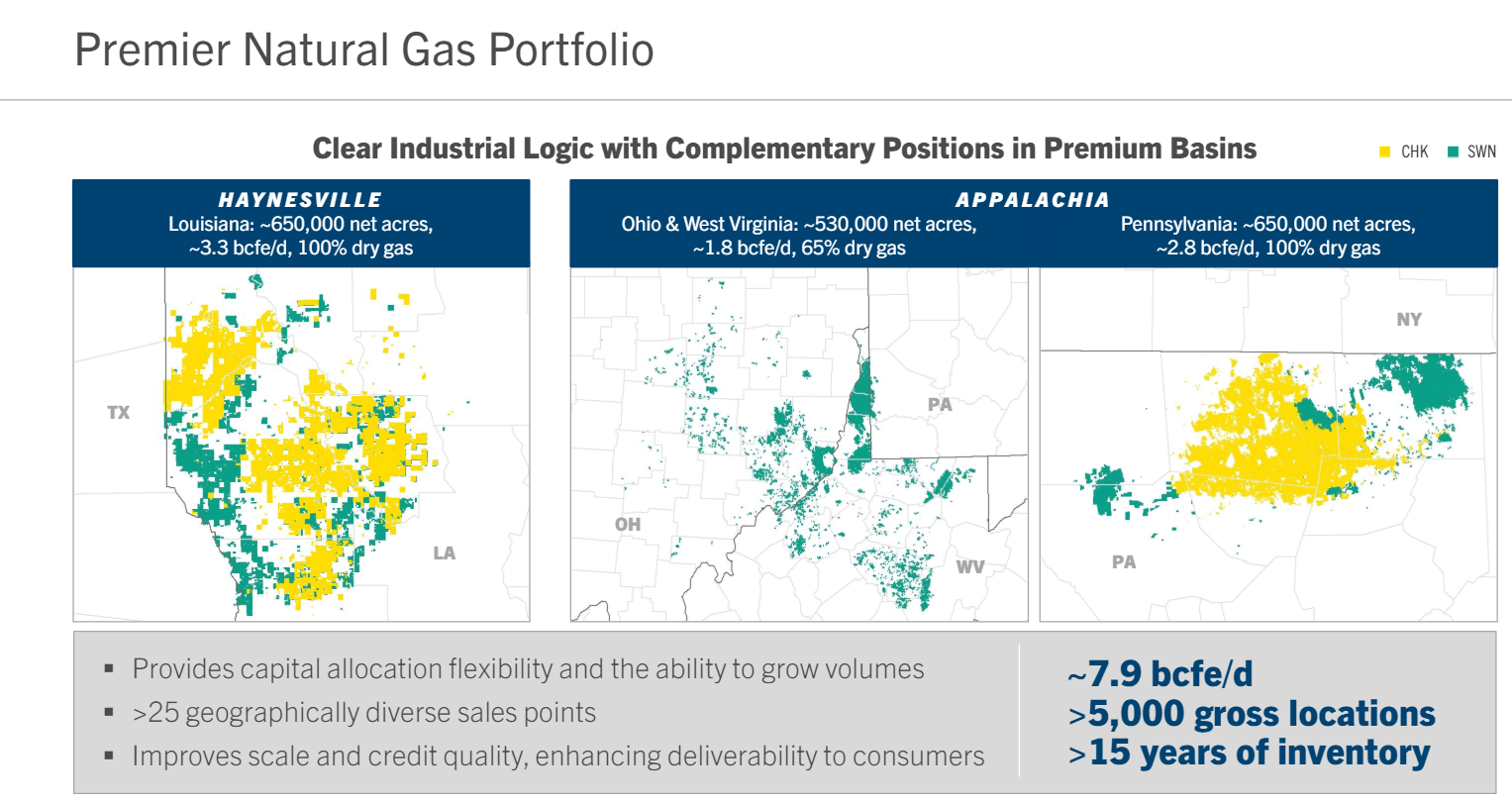

Then, on January 11 this year, CHK announced its acquisition of Southwestern Energy (SWN) for $7.4 billion. The combined entity would be the second-largest U.S. independent natural gas producer after EQT (EQT), with 1.8 million net acres in the Haynesville and Marcellus shale basins.

The deal makes strategic and operational sense. The combined entity will bring increased scale that lowers operational and G&A expenses. It will possess greater leverage over service providers and midstream operators while strengthening CHK’s marketing operation.

As we’ve seen with the large oil-focused shale operations, we expect the combined entity to be managed with less emphasis on production growth and more emphasis on maintaining reserve life.

Operationally, the two companies’ assets are contiguous in both operating regions. The chart below shows CHK’s acreage in yellow and SWN’s in green.

Drilling results for both companies are consistently strong, and we don’t expect that to change. CHK management estimates 15 years of high-quality drilling inventory. Unfortunately, the figure can’t be corroborated with either company’s reserves because the reserves were estimated using $2.64 per mcf natural gas, too low to render accurate reserve data, just as the $6.36 per mcf used in both companies’ 2022 reserve reports was unrealistically high.

We don’t see a risk to the deal closing as expected in the second half of the year. However, the potential for the FTC to become more activist regarding large energy sector deals introduces some uncertainty into the verdict.

The Deal’s Macro Impact

CHK’s acquisition of SWN will also have important macro ramifications. Consolidation among E&Ps has placed increasing volumes of U.S. natural gas production in fewer hands. After the CHK/SWN deal is completed, the top five independent producers will account for 15% of U.S. domestic dry gas production.

Adding 7.5 Bcf/d of supply from the oil majors and large producers’ share of domestic supply increases to 22.5%, certainly enough to make material additions or subtractions to overall supply. The greater the market share of these large gas producers and the more mature the shale gas resource becomes, the more likely it will be that producers behave rationally in response to natural gas prices.

In fact, the market appears to have reached a point where the major producers can reduce production in response to lower prices without running the risk that smaller producers add enough volumes to offset the curtailed volumes. Beginning in the fourth quarter of last year, producers, including EQT, Range Resources (RRC), CHK, SWN, and Comstock Resources (CRK), all curtailed gas production by allowing existing production to decline and/or scaling back their drilling programs.

These curtailments played a large role in precipitating a decline in total U.S. gas production, which was larger than we expected. Gas volumes dropped from a record high of 106 Bcf/d at the beginning of 2024 to around 100 Bcf/d today. The magnitude of the supply drop stabilized natural gas prices in the mid-$2.00 per mcf range, far higher than the high-$1.00 levels seen from February through April of this year. We believe rational behavior like this among gas producers, which is made possible by increasing industry consolidation, will improve the prospects of all gas-weighted E&Ps over the coming years.

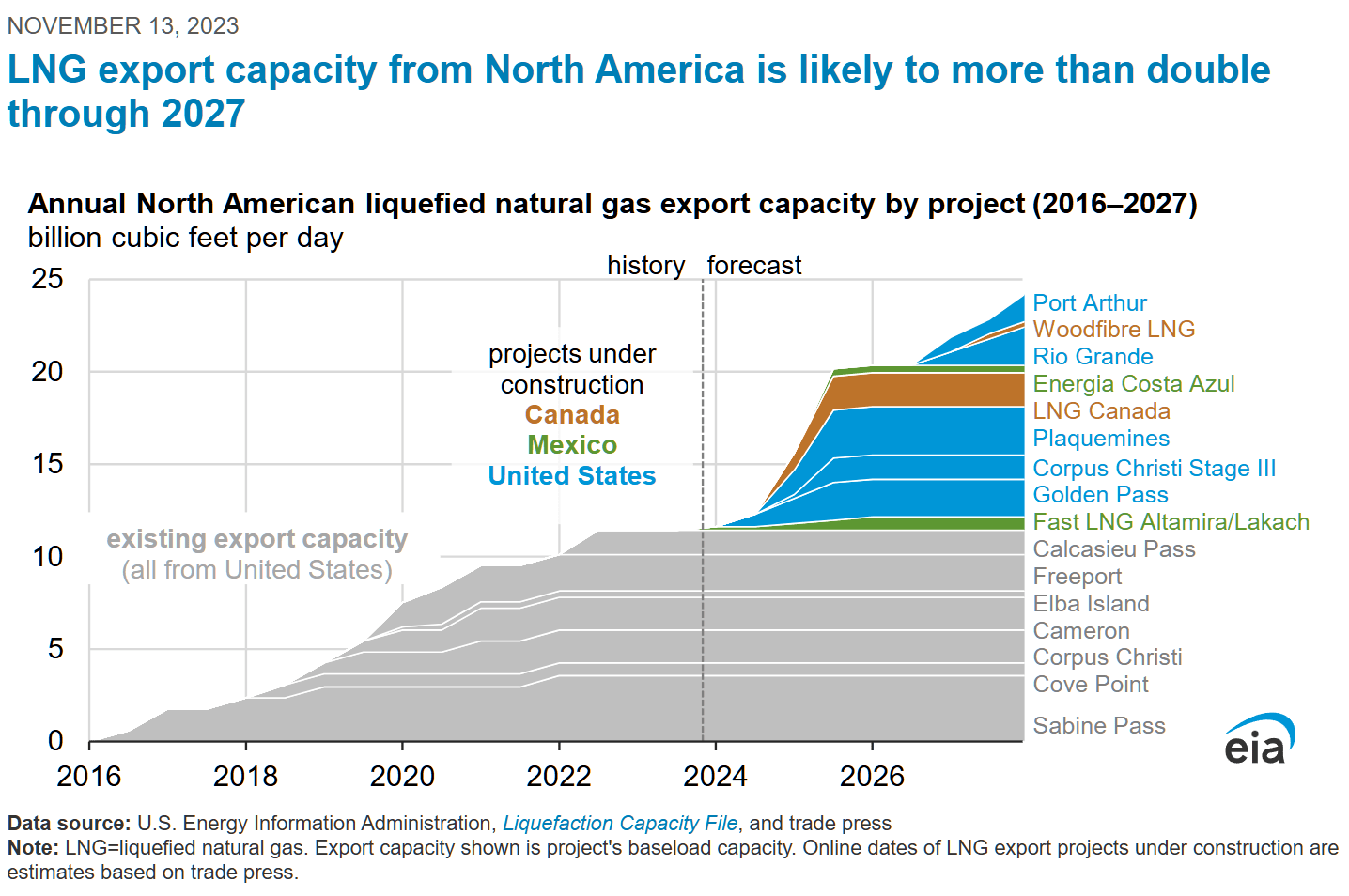

Turning to the demand side, the outlook for the natural gas market looks—dare we say it—bright when producer supply restraint is considered against the backdrop of bullish macro demand factors. While we view the optimistic demand projections related to an AI infrastructure buildout as more hype than substance, the LNG demand boost about to occur is every bit as real as the bullish forecasts imply. Over the next three years, the startup of LNG export facilities will boost domestic natural gas demand by 11.6 Bcf/d, or more than 10% from the current level, as shown below.

Source: EIA, Nov. 13, 2023.

This structural demand increase is expected to materialize with no additional boost from power burn. When combined with producer discipline amid low prices, it can contribute to sustained higher natural gas prices, which will directly benefit E&Ps.