(Idea) Chemours - Jon's Favorite Capital Cycle Investment Idea

By: Jon Costello

Chemours (CC) was formed on July 1, 2015, as a spinoff of DuPont’s (DD) more cyclical businesses. Chemours operates in three businesses: Thermal & Specialized Solutions (TSS), Titanium Technologies (TT), and Advanced Performance Materials (APM). In 2024, the company generated $5.8 billion in sales and $786 million in Adjusted EBITDA. This year, it is on track to earn approximately $750 in Adjusted EBITDA. It has an enterprise value of $5.6 billion. Its Adjusted EBITDA run-

Chemours Overview

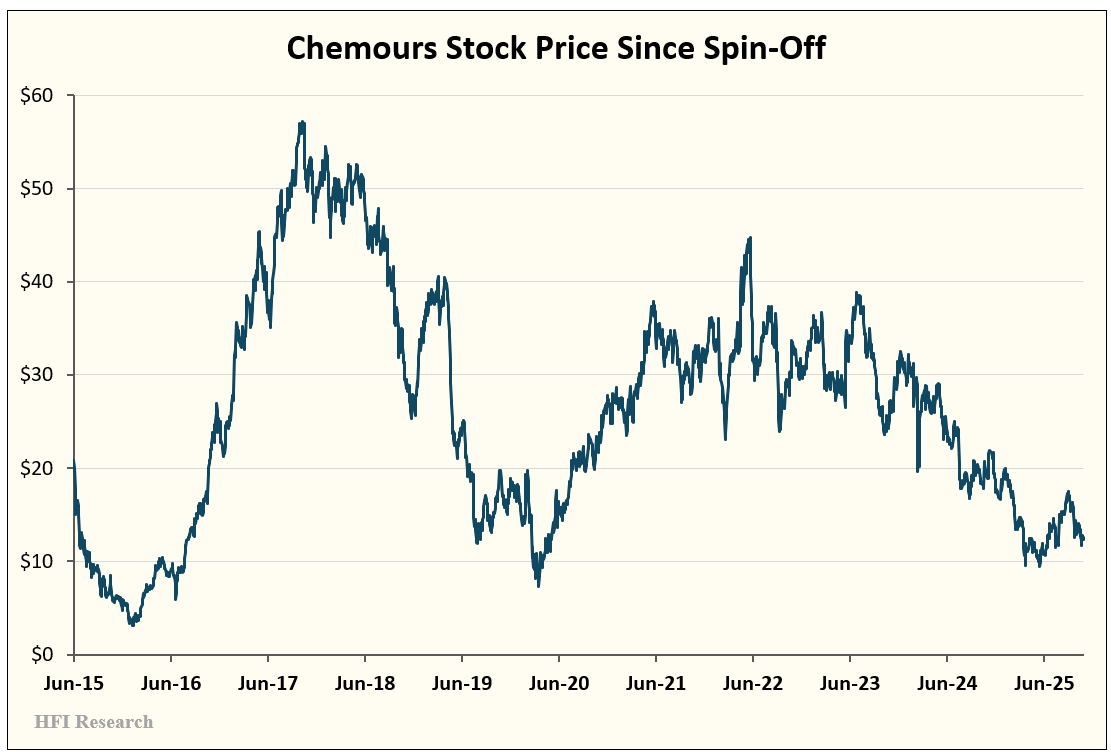

Chemours shares have been on a steady decline since 2023, as shown below. The shares are currently priced at a discounted valuation characteristic of a cyclical trough.

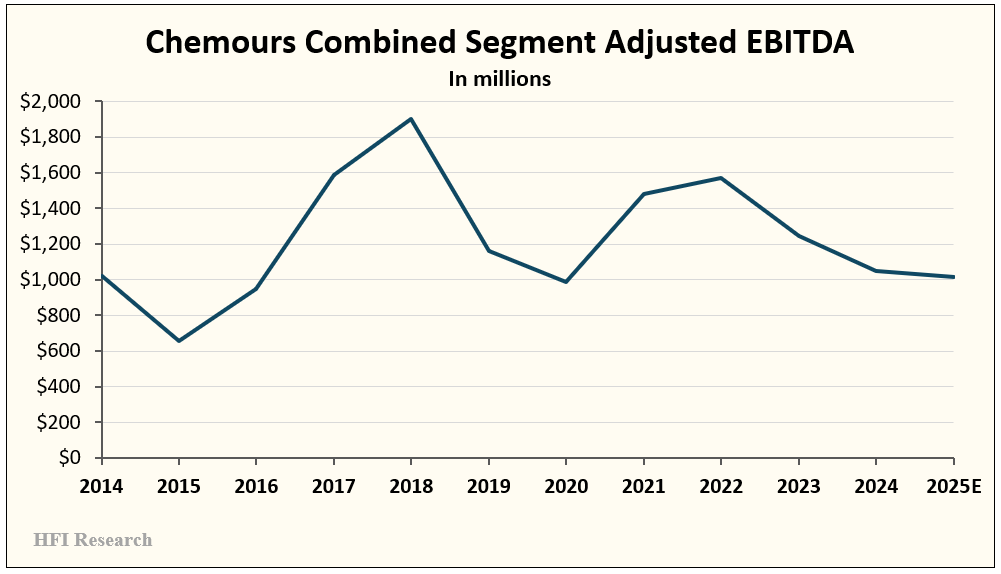

The selloff has coincided with the decline in Adjusted EBITDA. This year’s estimated $750 million is down nearly half from $1.4 billion generated in 2021.

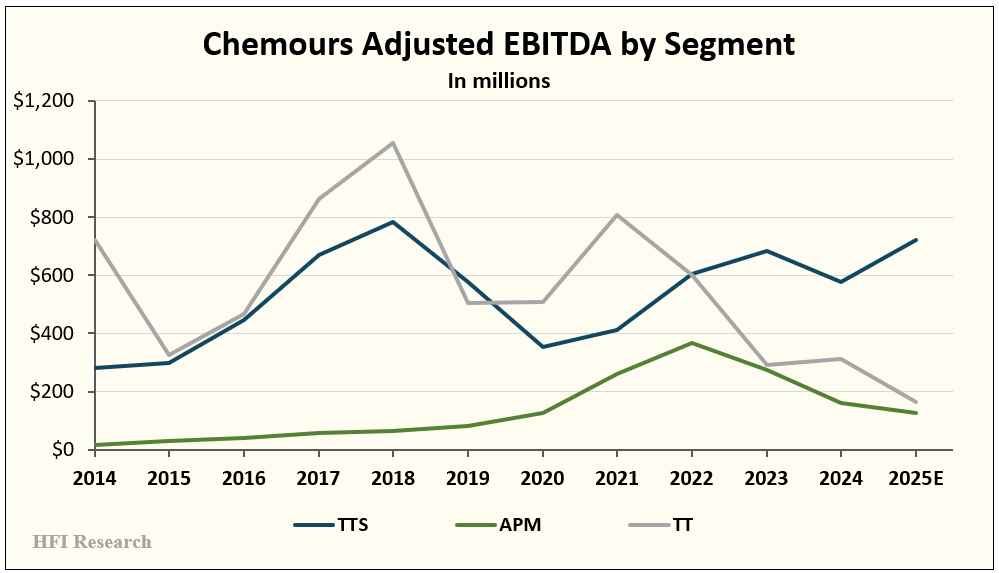

The decline was driven by the ongoing three-and-a-half-year downturn in Chemours’ two cyclical operating segments. These segments have been hit by weak domestic housing and construction markets, Chinese overcapacity, and, most recently, tariffs. The three segments’ annual Adjusted EBITDA contribution since 2014 is shown in the chart below.

When combined, Chemours’ cyclicality is evident.

Given the strong likelihood of a recovery in Chemours’ fundamentals over the next three years and the significant upside potential in its shares amid such a recovery, the time is right for aggressive investors to consider Chemours’ stock for long-term purchase.

Long-term investors in the company must be familiar with its operating segments, their EBITDA generation potential, and their challenges.

Thermal & Specialized Solutions (TSS)

This segment represents Chemours’ refrigerants and thermal-management portfolio. Its core brands are Opteon refrigerants and foam blowing agents, as well as legacy Freon hydrofluorocarbon (HFC) and chlorofluorocarbon (CFC) products. TTS’s end markets are air-conditioning and refrigeration for automobiles and buildings, foam insulation for buildings, and aerosol propellants for niche applications.

The TSS segment is currently Chemours’ profit engine, with strong margins that I believe are both insulated from cyclical forces and are sustainable. The segment’s demand drivers are climate change regulations coming into effect, air conditioning replacement cycles, and new construction.

This segment is a leading beneficiary of a movement by governments to force a refrigerant technology transition away from HFCs and to refrigerants with low global warming potential. In the U.S., the AIM Act is phasing down the production and consumption of HFCs. The leading replacement has been hydrofluoroolefins (HFOs), and Chemours, along with Honeywell (HON), holds a patented duopoly with its Opteon HFO product.

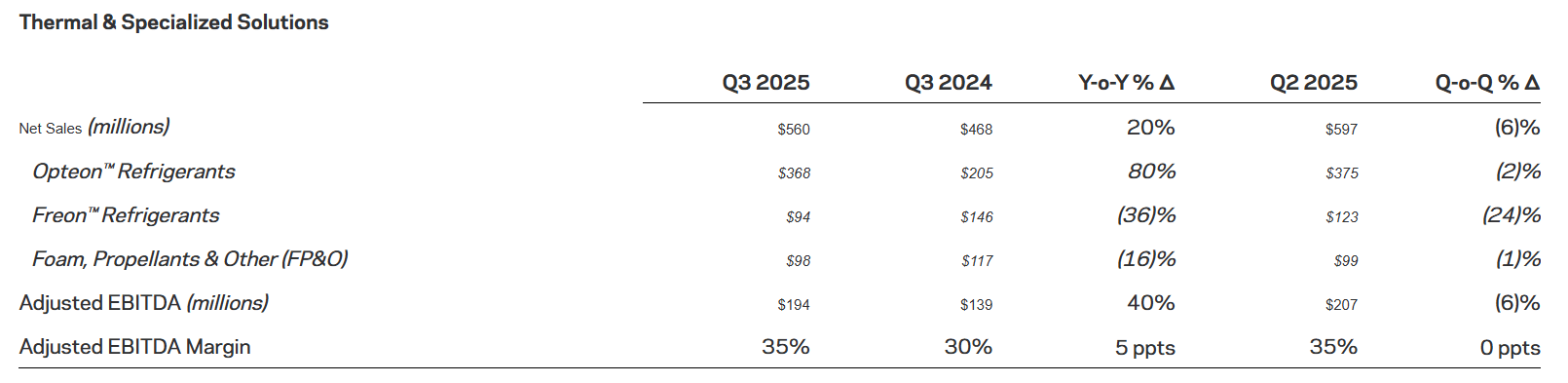

In the third quarter, TTS generated $560 million in sales, a 20% year-over-year increase. The increase was driven by 8% higher volumes and 11% higher prices. The Adjusted EBITDA margin came in at a historically healthy 35%. An 80% increase in Opteon sales drove the performance. Sales of the product now account for more than 75% of TSS segment sales. The impact of Opteon’s growth is illustrated in the table below, which depicts TTS’s third-quarter results.

Source: Chemours’ Q3 2025 Earnings Press Release, Nov. 6, 2025.

Clearly, Opteon’s growth is more than offsetting the shrinkage in Chemours’ legacy Freon and foam volumes, as expected.

Titanium Technologies (TT)

Chemours’ Titanium Technologies segment houses its Ti-Pure titanium dioxide pigment business. Titanium dioxide is a whitening agent and opacifier in paints, cosmetics, and other goods. Chemours is the second-largest producer of titanium dioxide in the global market, which is dominated by four firms. This segment is extremely cyclical, and its downcycle has been responsible for crushing Chemours’ Adjusted EBITDA. However, I believe the titanium dioxide market is near its cyclical trough, as explained in a previous article available here. As the cycle turns upward, it will drive most of Chemours’ Adjusted EBITDA recovery over the coming years.

The TT segment’s demand drivers include pigment demand from the paints and coatings, plastic, paper, automotive, architectural, and construction industries.

In the third quarter, TT generated sales of $612 million but only $25 million in Adjusted EBITDA, representing a 4% margin, due to an 8% decline in global titanium dioxide prices and a 2% decline in the segment’s sales volumes.

Advanced Performance Materials (APM)

This segment is Chemours’ high-end fluoromaterials portfolio. Its main products are Teflon fluoropolymers and coatings, Viton fluoroelastomers, Krytox specialty lubricants, and Nafion ion-exchange membranes.

Its products are used in semiconductors and advanced electronics, automotive applications, and energy transition applications such as hydrogen electrolysis and fuel cells.

APM is less cyclical and enjoys sustained higher margins. However, it is Chemours’ smallest Adjusted EBITDA contributor and is currently being negatively impacted by sluggish industrial end-user demand.

In the third quarter, the segment generated $311 million of sales and $14 million of Adjusted EBITDA. Volumes were down 15% year-over-year.