(Idea) Chemours - Investment Thesis Remains Intact Despite Weak Q4 Results

Editor’s Note: Please also read the original Chemours write-up.

By: Jon Costello

Chemours CC 2.19%↑ reported fourth-quarter 2025 results last Thursday, February 19. The results fell short of consensus expectations and caused the shares to decline by 25% from peak to trough over two days. After bottoming at $16.15, the shares have since recovered to $18.41, still shy of their recent high before earnings of $21.85.

While the fourth-quarter results were weak, management’s forward-looking expectations were considerably more optimistic. Overall, I expect results to improve over the course of 2026. A sustained recovery in the titanium dioxide market should support further gains in 2027. My Chemours investment thesis remains intact, and the shares remain attractive at their current price for a three-year or longer holding period.

The Cause of the Selloff

Without a doubt, the fourth quarter results were ugly on a GAAP basis, as the ongoing downturn in its Advanced Performance Materials (APM) and Titanium Technologies (TT) operating segments weighed on corporate profitability.

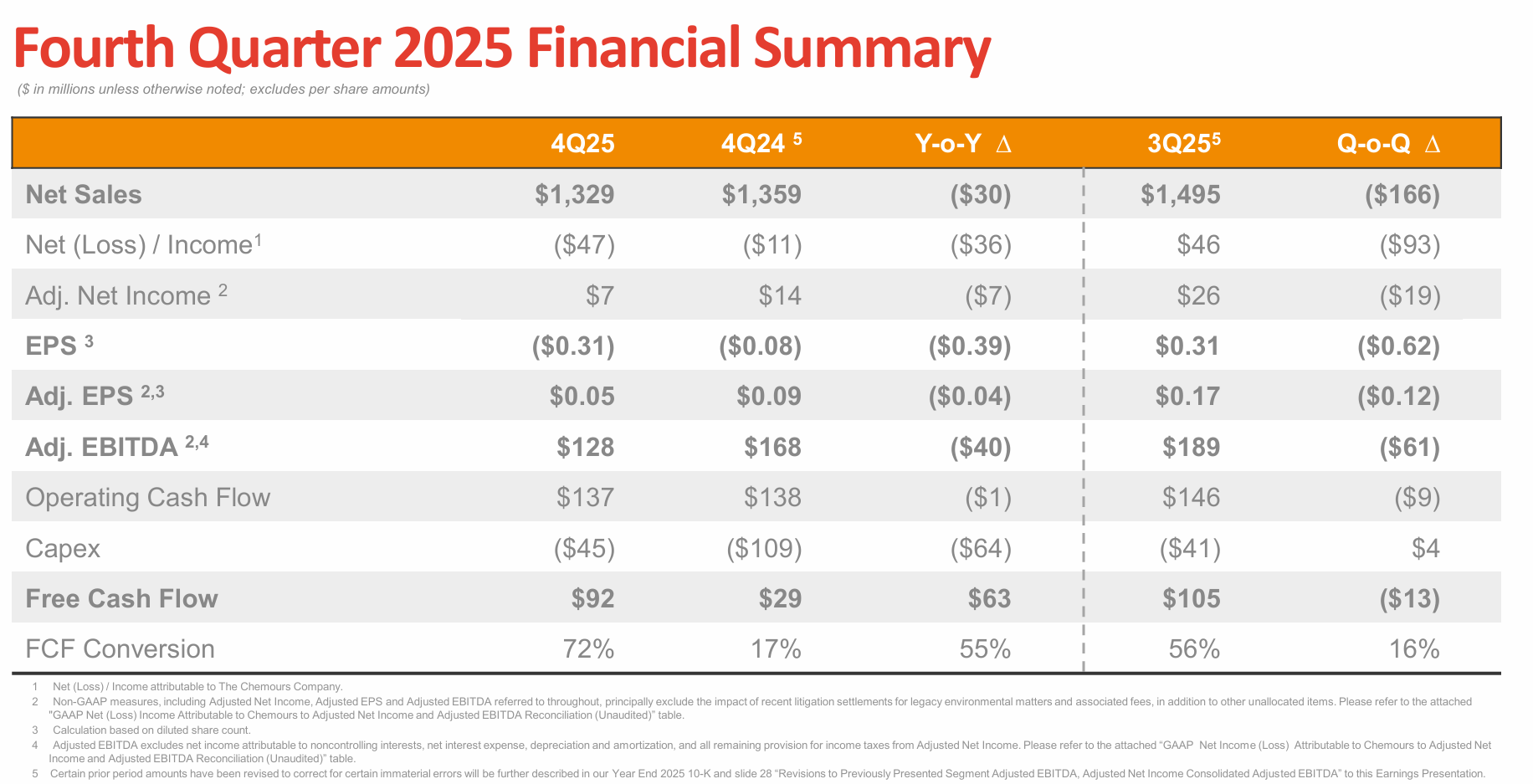

The consolidated quarterly results comparison is shown below.

Source: Chemours Q4 2025 Earnings Conference Call Presentation, Feb. 20, 2026.

As the table shows, cash flow results during the quarter were better. Operating cash flow was flat year over year, and capex was down significantly.

Management cited the impact of adverse “cost absorption,” or negative operating leverage, which occurs when sales volumes fall faster than unit costs and lower Adjusted EBITDA. Management also attributed the poor results to an unfavorable sales mix in the APM segment and higher taxes.

The reason why the shares sold off so sharply after earnings was that they ran so hard into earnings.

When the optimistic sentiment was met with a “meh” earnings report and near-term outlook, it’s no wonder that some investors decided to take profits rather than wait for clear signs of a more robust and sustainable recovery. If fundamentals continue to improve over the coming quarters—driving Adjusted EBITDA higher—I expect the shares to perform well from the current price.

Why the Selloff was Overdone