(Idea) Cardinal Energy - Bargain Bin

Editor’s Note: Cardinal Energy is not a holding in the HFI Portfolio. Ideas from HFI Research is a separate paid subscription service from HFI Research.

Jan 26, 2025 Cardinal Write-up

By: Jon Costello

Note: Dollar values are in Canadian dollars unless otherwise specified.

The recent selloff amid global E&P stocks has sent Cardinal Energy (CJ:CA) shares deep into bargain territory. We fully expect the company to survive this downturn in fine shape. Investors in its shares will benefit from significant growth in production, cash flow, and dividends over the next two years and beyond.

Cardinal ensured its growth prospects by raining debt twice in 2025. The closed two term-loan unsecured debenture financings together totaled $105 million and featured a weighted average interest rate of 7.96%.

Combined with the company’s $190 million available on its borrowing base facility, the $105 million debt issuance ensured that Cardinal will have the resources necessary to fully develop its Reford project.

The downside of the debt issuance was that it increased the company’s cash interest expense and net debt-to-cash flow while marginally reducing its free cash flow breakeven.

Production Growth Set to Increase Shareholder Value

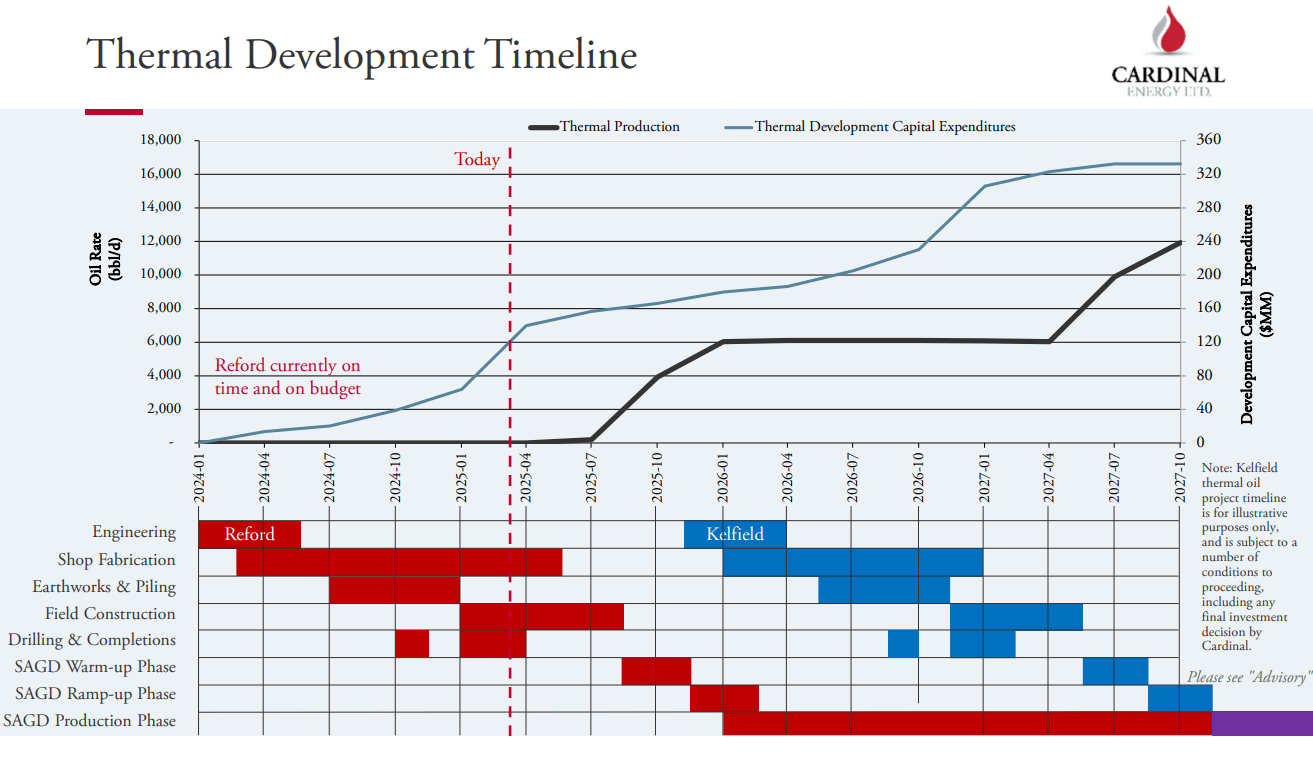

The financings will allow Cardinal to complete its growth projects. The company is working on a small oil sands steam-assisted gravity drainage (SAGD) project called Reford. The project’s completion timeframe has remained unchanged, with the pre-production warm-up phase scheduled to begin by the end of the year. Reford is expected to begin its production ramp in early 2026. It will transition to commercial production shortly thereafter.

When operating at capacity, Reford will add 6,000 bbl/d of heavy oil production to Cardinal’s existing production base of approximately 21,500 boe/d of mostly conventional light oil.

Once Reford has been placed into service, the company plans to begin its second SAGD project, called Kelfield. The project is also expected to add 6,000 bbl/d of heavy oil production and will increase Cardinal’s total production to 33,500 boe/d. Kelfield’s timing is currently expected to be one year after Reford.

The development timeline of these two projects is shown below.

Source: Cardinal Energy March 2025 Investor Presentation.

Cardinal currently expects to fund Kelfield using cash flow from operations, which will benefit from Reford’s production. Of course, if oil prices remain low, Cardinal will have the option of postponing its Kelfield project. We would only expect the company to proceed with the project if WTI is trading at the high-$60s per barrel or above. Anything below that level could risk the deterioration of the company’s financial position.

If both Reford and Kelfield are completed on time, we estimate that Cardinal will generate approximately $500 million in annual adjusted funds flow by the end of 202 at US$80 per barrel WTI. Its production would have increased from the current rate of 21,500 boe/d to 33,500 boe/d.

If Cardinal’s shares traded at four times cash flow, they would trade at approximately $12.00 per share by then. However, the shares may garner a premium relative to their historical trading multiple. We wouldn’t be surprised to see Cardinal shares trade to $13.50, and perhaps higher, depending on the prospects for additional oil sands projects planned at the time.

50% Chance of a Dividend Cut

We put the probability that Cardinal will cut its dividend at 50%. We have no special insight into the board of directors or management’s thinking about the issue. A cut will be likely if management believes Cardinal’s financial position and ability to develop its Reford project will be put at risk, which, in turn, depends on the company’s outlook for oil prices over the coming months.

Management hinted at its intent to maintain a strong financial position in its March 13 press release. Management stated that it “appreciates the recent market and oil price volatility brought forth by North American tariff uncertainty, and will consider necessary changes to our outlook should the implications have a meaningful effect on Cardinal’s business.” While it didn’t specifically call out the possibility of a dividend cut, it appears to be implying as much, given the language used.

Since the prospect of a dividend cut is so binary, we recommend that investors allocate half of their desired final allocation to Cardinal shares now and the other half after the dividend is cut. In other words, if an investor would feel comfortable allocating 2.5% of their portfolio to Cardinal shares, they should consider allocating half the position—or 1.25% of their portfolio—to the name now and wait for a dividend cut before allocating the other half.

If the company doesn’t cut the dividend, the shares will do well over the coming quarters, and an investor will enjoy a juicy 14.5% dividend yield on the current stock price of around $5.00. If the dividend is cut, Cardinal shares are likely to sell off, thereby increasing their long-term upside.

Factors in Favor of the Dividend Being Maintained

What Cardinal investors have going for them is that oil prices below the mid-US$60s are not sustainable. We estimate that U.S. crude oil production will decline by more than 500,000 bbl/d in 2025 if WTI were to remain in the low-US$60s. U.S. oil production will continue to decline until prices increase, with the decline growing steeper if WTI remains in the high-US$50s, where it traded today. Lower U.S. shale output will eventually cause oil prices to inflect higher during a demand recovery.

Moreover, due to the nature of the shale resource and the dwindling drilling inventories of U.S. shale producers, a ramp back above 13 million bbl/d will be slow. If WTI remains in the US$60s for another year or two, the resource will be challenged to surpass its current peak of 13.3 million bbl/d.

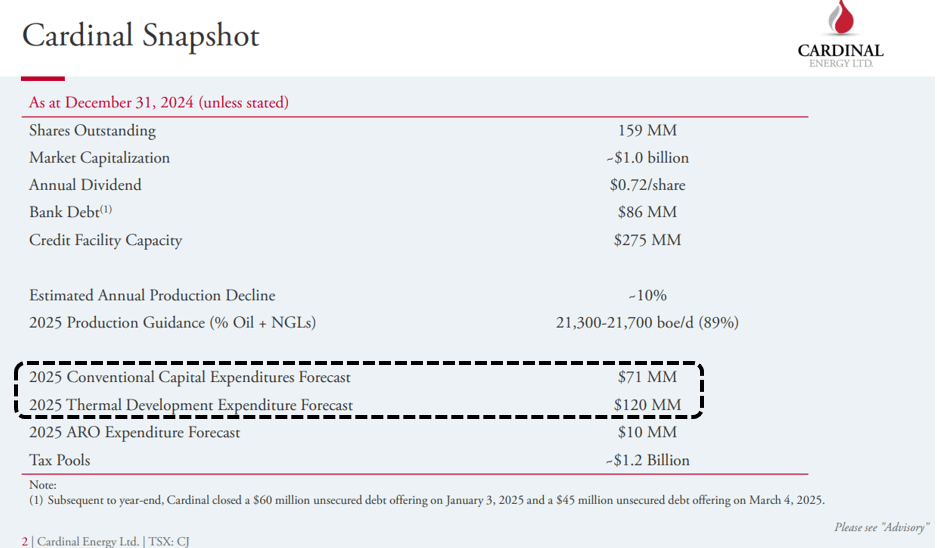

We estimate that Cardinal’s cash flow breaks even at US$62.50 per barrel WTI. At US$62.50 WTI, we estimate that Cardinal’s adjusted funds from operations will be roughly $190 million, which is also the amount needed to fund its total 2025 capex program, as shown below.

Source: Cardinal Energy March 2025 Investor Presentation. Dotted line added by author.

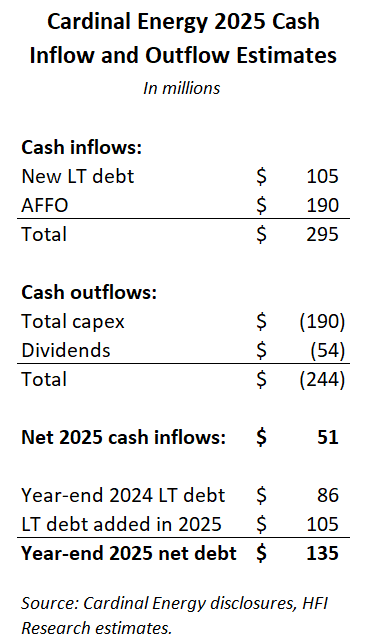

Down to US$62.50, Cardinal will be able to fund the $120 million of remaining capex for Reford, though it will not be able to cover any of its $54 million of annual dividend payments. We estimate that Cardinal will end 2025 with net debt of $135 million. Our estimates are shown in the following table.

By year-end 2025, the Reford project is likely to be complete. By the second quarter of 2026, the project is expected to contribute to Cardinal’s cash flow.

Since our oil price outlook is higher than US$62.50 per barrel, we believe there is a good chance that Cardinal will be able to fund the development of Reford while continuing to pay its dividend—despite the stock price action, which implies that a dividend cut is imminent.

Dividend to be Cut Amid Sustained Low Oil Prices

The decision of whether or not to cut will hinge on Cardinal’s adjusted funds from operations vis-à-vis management’s targeted net debt level. In the company’s fourth-quarter 2024 earnings press release, published on March 13, management stated, “Although we have access to sufficient capital resources, we will continue to be responsible in our capital allocation and endeavor to maintain a new debt to adjusted funds flow ratio below 1.0x.”

Given our 2025 estimates for Cardinal’s cash flow and year-end net debt, we expect the company to cut its dividend if WTI were to trade at or below an average of US$60 per barrel for a stretch of several weeks. At that point, the company will have to borrow to fund its operations. Its debt would rise above one-time cash flow, and its financial position would grow weaker. This could put the company’s ability to complete its Kelfield project at risk. Cutting the dividend, meanwhile, would free up $54 million annually, removing any concern about the company’s ability to complete the project. Furthermore, if oil prices remained around US$60 for a few weeks, other North American E&Ps would also be looking to cut their dividends, so Cardinal probably wouldn’t be alone.

Purely from the perspective of long-term shareholder value, a dividend cut would be a sensible policy amid a prolonged oil price downturn. We suspect that it wasn’t lost on Cardinal’s management that Birchcliff Energy’s (BIR:CA) stock price increased immediately after the company made a long-expected dividend cut.

That said, Cardinal’s situation is somewhat different than that of Birchcliff. Cardinal is smaller than Birchcliff, with an enterprise value of $932 million versus Birchcliff’s $2.2 billion. Cardinal shares have also traded at a significantly higher dividend yield than Birchcliff’s. These factors made Cardinal shares more heavily owned by retail investors, with relatively little institutional ownership. The heavier weighting of retail investors will probably cause Cardinal’s shares to sell off hard after a dividend cut is announced, at least in the immediate term. However, we’d expect the shares to recover shortly thereafter as investors begin to appreciate that the dividend ensures that the company’s long-term financial prospects remain intact.

Cardinal shareholders concerned about a dividend cut should keep in mind that they would benefit over the longer term from the company’s ability to both fund its Kelfield growth project and emerge from the current downturn with a strong balance sheet. They should also keep in mind that the longer oil prices remain low, the longer the negative impact on supply, and the longer they’ll remain elevated during a recovery in demand. Cardinal possesses considerable cash flow torque to oil prices, and its long-term upside will increase the longer oil prices remain low.

Conclusion

Whatever scenario plays out, Cardinal is bound to survive this downturn. We consider a buy below $5.00 per share to be a deep bargain relative to the company’s prospects just one year in the future.

Cardinal investors would also benefit over the coming years from the company’s policy of paying out free cash flow through dividends, which would likely continue after its oilsands projects enter service.

All these features make Carinal one of the more attractive E&P investment alternatives in the North American oil patch. We consider its shares to be a particularly attractive buy below $5.00. At that price, we will consider adding it to our own holdings.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.