(Idea) Cardinal Energy

A Buy For Income And Long-Term Gains.

Editor’s Note: Ideas from HFI Research is a separate subscription from HFI Research. Cardinal Energy is not a holding in the HFI Portfolio, so this write-up is not included.

Cardinal Energy was first written up on August 7, 2023. Please see the public post here.

By: Jon Costello

Note: Dollar values are in Canadian dollars unless otherwise specified.

Cardinal Energy (CJ:CA) isn’t one of our pound-the-table energy stock longs over the next few years like Strathcona Resources (SCR:CA) and Veren (VRN). However, we believe it can serve a constructive role in a portfolio as an income-generating name with big upside potential over the next three to five years.

We’re No Longer Hesitant to Buy

We’re considering buying Cardinal shares for our HFIR Energy Income portfolio. Our main hurdle for making a commitment in the name has been the risk that sustained low oil prices could force a dividend cut. This risk has diminished over the past several weeks for several reasons.

The primary reason is the company's recent capital raise. On January 3, Cardinal announced the closing of a $60 million bought-deal financing. The deal included 50,000 senior subordinated unsecured debentures issued for $1,000, which pay interest of 7.75% annually. Each debenture has 65 common share purchase warrants that are exercisable at $7.00 for three years after the closing date. These shares dilute existing shareholders by 2%.

The capital infusion largely staves off risk to shareholders stemming from either a dividend cut or additional equity issuance.

Another reason Cardinal’s outlook has brightened relates to oil macro. The major oil market analyst organizations, like the IEA, forecast inventory builds beginning in the first quarter, but they are not materializing. Moreover, real-time market readings imply that builds aren’t going to happen, at least not in the first quarter. Oil well freeze-offs in the U.S. are slated to further reduce first-quarter global supply by 500,000 bbl/d, improving the supply/demand balance.

Stable oil prices above Cardinal’s cash flow breakeven slightly below US$70 per barrel WTI will reduce the risk of a dividend cut even further. We expect low inventory builds at best in the subsequent quarters of 2025 and draws in 2026, barring a global recession. If our view plays out, and if consensus begins to turn more bullish, Cardinal shares are likely to be bought and appreciate significantly by the end of 2025 from their current price of $6.60.

High Returns from Dividends and Appreciation

Investors must consider Cardinal from a total return perspective, not from dividends or capital appreciation alone. The shares currently yield 11%—one of the highest yields among North American E&Ps—so dividends will contribute a substantial portion of an investor’s return generated from Cardinal shares over the next few years. For 2025 and 2026, we expect the company to keep the current dividend flat, even if its cash flow increases as it places new projects into service.

Cardinal shares are likely to appreciate in price due to increasing cash flow, which is likely to begin later this year. We expect the shares to reflect the positive cash flow inflection around mid-year after production from new projects has scaled up.

Shareholders could also benefit from a higher multiple as the market realizes that additional thermal projects will contribute further to higher cash flow over subsequent years.

Financial Outlook is Set to Improve

As new projects come online, the proportion of Cardinal’s production represented by its current base of conventional low-decline/high-ARO assets will shrink, and its proportion of thermal oil sands assets will increase.

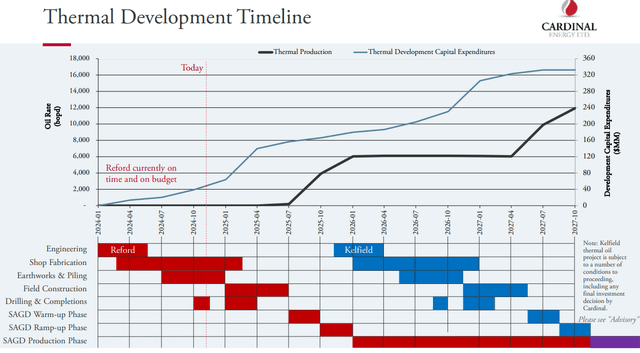

Source: Cardinal Energy Q3 2024 Investor Presentation.

Cardinal’s Reford modular thermal project is set to begin its production ramp in July, adding 6,000 bbl/d of oil production. The addition will increase Cardinal’s total production from 22,500 boe/d to 28,500 boe/d by the end of the year. We expect Reford’s production ramp to be a catalyst for a higher share price.

Reford’s production will increase Cardinal’s adjusted funds flow from today’s $290 million at US$79 per barrel WTI to approximately $400 million.

Based on these post-Reford figures, Cardinal shares currently trade at a 3.0-times cash flow multiple. Assuming its current 4.4-times cash flow ratio remains intact and its share count and net debt levels remain constant, Cardinal’s shares would trade at $9.50, representing 45% upside from the current share price of $6.60. Adding a year of dividends boosts the implied return to 56%.

Cardinal’s next project after Reford, Kelfield, is expected to increase the company’s total production to 34,500 boe/d by the end of 2027. Kelfield is expected to grow Cardinal’s adjusted funds flow to $510 million by the end of 2027.

Using the same assumptions as above, Cardinal’s shares would increase to $12.50, implying 90% upside from their current price. Three years of dividends at their current rate would boost the implied total return to 120%.

While these projects are under development, we expect Cardinal’s total capex to run at around $200 million annually. We expect its annual dividend obligation to remain flat at approximately $116 million. Once Reford is fully ramped and Cardinal is generating $510 million of cash flow, the company will generate $0.51 per share of free cash flow that can be allocated at management’s discretion. This free cash flow will eliminate the company’s need to raise capital at an onerous cost to fund its thermal oil asset buildout.

We expect free cash flow to be initially allocated to paying down debt taken on to build the new assets. As Kelfield nears completion in 2027, Cardinal will have the financial flexibility to pay a sustainably higher dividend, supporting a higher stock price.

The increased cash flow from Cardinal’s new thermal projects will increase its dividend coverage. Greater dividend coverage will reduce the need for the market to price Cardinal’s shares as if its dividend is at risk, which is the case today. Combined with a higher dividend payout per share and a higher-quality production profile, we believe the valuation multiple on Cardinal shares can head to the 4.5-to-5.5-times cash flow range.

Cardinal will also retain its high torque to crude oil prices. Prices above $80 will see cash flow grow significantly higher, increasing total returns and the prospect of large special dividends. In light of the company’s history of returning excess capital to shareholders, we’re confident that it will distribute future cash flow in a shareholder-friendly manner.

Longer-term, Cardinal can initiate additional thermal oil projects after Kelfield, further increasing shareholder value through higher cash flow, greater dividends, and opportunistic share repurchases.

Risks

The knock on Cardinal is the low quality of its existing assets. Cardinal has worked through the highest quality acreage in its low-decline conventional production. It is likely to sustain production over the next three or so years, but we grow increasingly concerned that its conventional assets will decline in the years afterward. If the company’s new thermal assets perform as management expects, the cash flow they produce will more than offset the cash flow lost from the company’s conventional assets.

Other criticisms of Cardinal are that its shares trade at an elevated multiple for its small size and that its is heavily burdened by its substantial ARO obligations, which totaled nearly $100 million at the end of the third quarter. On both of these points, however, production growth and greater free cash flow will be the solution. Once the thermal asset completion is within sight, we expect these criticisms to die down.

Of course, if the thermal resource buildout fails for whatever reason, the company’s long-term prospects would be thrown into doubt and its stock would get clobbered. This is the nightmare scenario that makes progress on the thermal asset buildout important for long-term Cardinal shareholders.

Conclusion

The value proposition for Cardinal’s shares is simple: production, cash flow, and capital distributions to shareholders are all very likely to increase significantly for at least the next five years and probably beyond. Cardinal’s multiple doesn’t seem so high when considering its growth prospects, while its future cash flow generated from production growth will dwarf its ARO obligations.

Cardinal remains one of our preferred oil-weighted names in the Canadian oil patch, along with Veren (VRN) and Strathcona (SCR:CA). Investors should consider buying the shares over the coming weeks and months before investors begin to look ahead to the cash flow from completed projects.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of VRN, VRN:CA, SCR:CA either through stock ownership, options, or other derivatives.